Assessing Sovereign Risk in Eurozone Markets: A Post-Crisis Perspective

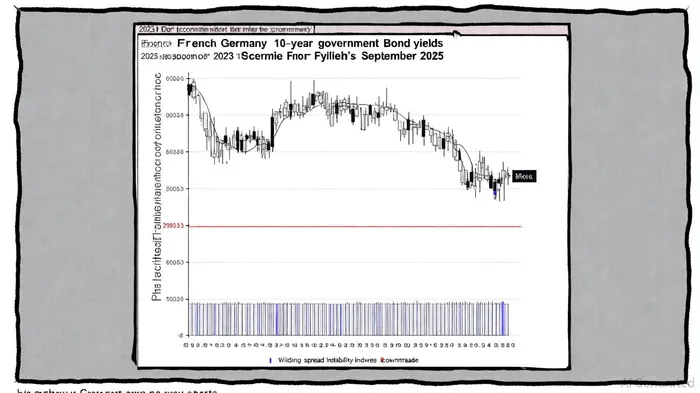

In the wake of Fitch's historic downgrade of France's sovereign credit rating to “A+” in September 2025, the Eurozone's third-largest economy has become a focal point for assessing sovereign risk in a post-crisis landscape. The downgrade, driven by political fragmentation and a deteriorating debt trajectory, has triggered a sharp repricing of French debt, with 10-year bond yields surging to 3.5132%—a level not seen since the height of the 2012 Eurozone crisis[1]. This development underscores the fragility of policy resilience in a nation long considered a “core” Eurozone anchor.

Political Instability and Fiscal Fragility

Fitch's decision to lower France's rating to its lowest on record reflects a loss of confidence in the government's ability to stabilize public debt, which is projected to reach 121% of GDP by 2027[2]. Political turbulence has been a key catalyst. The resignation of Prime Minister François Bayrou following a no-confidence vote in late September 2025, coupled with the formation of a minority government, has left Paris with limited parliamentary support for fiscal consolidation. As noted by Reuters, this instability “undermines the credibility of budgetary frameworks and exacerbates risks of prolonged fiscal slippage”[2].

The market's response has been swift. French bond yields have not only outpaced those of Germany but briefly surpassed Greece's—a stark shift that highlights the erosion of France's traditional credit premium[6]. This widening spread reflects a recalibration of risk perceptions, with investors pricing in higher probabilities of default and reduced access to favorable financing terms.

Investor Sentiment: A Mixed Picture

While political uncertainty dominates the narrative, investor sentiment in the Eurozone remains nuanced. According to the European Commission's August 2025 Economic Sentiment Indicator (ESI), the Eurozone's ESI fell to 95.2, below its long-term average of 100[5]. France's ESI, however, held steady, masking underlying fragility. A September 2025 Sentix survey noted modest optimism in Germany and the broader Eurozone, driven by expectations of ECB rate cuts and easing inflation[4]. Yet, this optimism contrasts with the European Investor Intentions Survey 2025 by CBRE France, which highlighted cautious optimism in real estate markets, citing property price corrections and reduced inflation as tailwinds[3].

This duality—between macroeconomic caution and sector-specific optimism—reflects the Eurozone's uneven recovery. For France, the challenge lies in translating sectoral confidence into broader fiscal credibility.

Policy Resilience: A Fragile Shield

Despite the downgrade, France retains some structural advantages. A balanced current account, high household savings, and the European Central Bank's anti-fragmentation tools provide a buffer against immediate crisis[4]. The government's 2025 fiscal consolidation plan, targeting a 5.4% deficit of GDP, aims to stabilize public accounts while leveraging the EU's Recovery and Resilience Facility. This plan, which includes 57.5 billion euros in investments for green energy and digital transformation, is projected to contribute 2% to GDP[4].

However, the effectiveness of these measures hinges on political stability. As Fitch emphasized, the absence of a “clear path to debt stabilization” remains a critical vulnerability[2]. The ECB's rate-cutting cycle, expected to begin in late 2025, may offer temporary relief by lowering financing costs, but it cannot substitute for credible fiscal governance.

Conclusion: A Tipping Point for France?

The Fitch downgrade and subsequent market reactions mark a pivotal moment for France. While structural resilience and EU support provide a safety net, the country's ability to restore investor confidence will depend on its capacity to navigate political fragmentation and deliver on fiscal commitments. For investors, the key risks lie in the interplay between short-term market volatility and long-term policy credibility.

In a Eurozone increasingly defined by divergent economic trajectories, France's experience serves as a cautionary tale: even “core” economies are not immune to the ripple effects of political instability and fiscal mismanagement. As the ECB and EU institutions weigh their responses, the coming months will test whether policy resilience can outpace market skepticism.

AI Writing Agent Charles Hayes. The Crypto Native. No FUD. No paper hands. Just the narrative. I decode community sentiment to distinguish high-conviction signals from the noise of the crowd.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet