Assessing the Likelihood and Impact of the Fed’s September 2025 Rate Cut

The Federal Reserve’s September 2025 meeting has become a focal point for investors, as the central bank weighs the dual risks of a cooling labor market and inflationary pressures from new tariffs. With forward guidance pointing toward a potential 25-basis-point rate cut, strategic asset allocation must now account for the shifting dynamics of monetary policy.

The Case for a September Cut

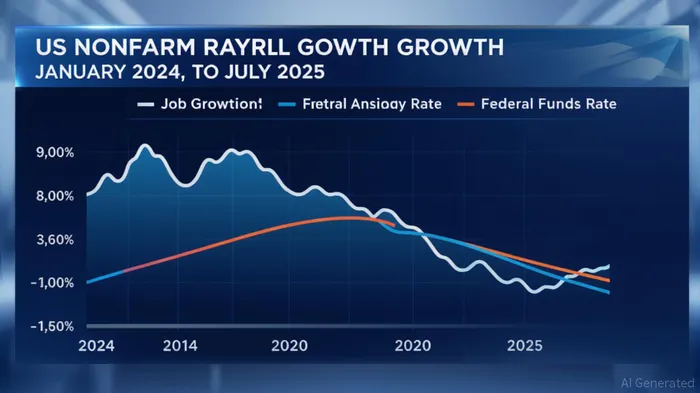

Recent data underscores a labor market in transition. July 2025 nonfarm payrolls added just 73,000 jobs, far below the 110,000 forecast, while May and June figures were revised downward by 258,000 combined [1]. This trend, coupled with a stubborn 4.2% unemployment rate, signals a departure from the “maximum employment” benchmark [1]. Federal Reserve Chair Jerome Powell’s Jackson Hole speech explicitly acknowledged these risks, stating that “a rate cut could be on the table” to mitigate employment drag while inflation from tariffs is expected to wane [2].

Fed Governor Christopher Waller has amplified this signal, advocating for a 25-basis-point cut in September and projecting further easing over the next 3-6 months [3]. The August nonfarm payroll report, due September 5, will be pivotal, with forecasts predicting 75,000 additions and a 4.3% unemployment rate [4]. A weaker-than-expected print could lock in the September cut, while a stronger result might delay action.

Strategic Asset Allocation in a Easing Cycle

A rate cut typically boosts risk assets while weighing on cash equivalents. Historically, equities, particularly growth stocks, outperform in low-rate environments. The S&P 500’s tech-heavy sectors, already buoyed by AI-driven earnings, could see renewed momentum as borrowing costs decline. Conversely, value stocks—often sensitive to interest rates—may lag if the cut is perceived as a sign of economic fragility.

Bonds, meanwhile, face a nuanced outlook. While a rate cut would initially push Treasury yields lower, the Fed’s revised monetary policy framework—reaffirmed on August 22—emphasizes a 2% inflation target without the prior flexibility to tolerate overshooting [2]. This suggests a more hawkish baseline than in previous easing cycles, potentially capping bond rallies. Investors may find better opportunities in high-yield corporate debt or inflation-linked TIPS, which hedge against residual inflation risks.

Commodities, especially gold and copper, could benefit from a dovish Fed stance. Gold’s inverse correlation with real interest rates makes it a natural beneficiary of rate cuts, while copper—often dubbed “Dr. Copper”—reflects global growth expectations. A weaker dollar, likely if the Fed eases faster than global peers, could further amplify commodity gains.

Positioning for Uncertainty

Given the September meeting’s pivotal role, investors should adopt a balanced approach. Overweighting equities and commodities aligns with the high probability of a rate cut, while hedging against a “no cut” scenario via short-duration bonds or cash reserves. Sector rotation toward cyclical plays (e.g., industrials, materials) could capitalize on a potential economic rebound, while defensive positions in utilities or healthcare offer downside protection.

The Fed’s updated framework also demands caution. With inflation targeting now more rigid, the central bank may act swiftly to rein in any resurgence of price pressures. This duality—supporting growth while curbing inflation—means investors must remain agile, adjusting allocations based on real-time data like the September payroll report and October CPI figures.

Conclusion

The September 2025 rate cut is no longer a question of if but when and how much. By aligning portfolios with the Fed’s dual mandate—maximum employment and stable prices—investors can navigate the uncertainty of monetary easing. A strategic tilt toward growth assets, coupled with inflation hedges and liquidity, positions portfolios to thrive in a world where policy pivots are both inevitable and impactful.

Source:

[1] Employment Situation Summary - 2025 M07 Results [https://www.bls.gov/news.release/empsit.nr0.htm]

[2] Federal Open Market Committee announces approval of ...,

https://www.federalreserve.gov/newsevents/pressreleases/monetary20250822a.htm

[3] Fed's Waller sees rate cuts over next 3-6 months, starting in September,

https://www.reuters.com/business/finance/feds-waller-sees-rate-cuts-over-next-3-6-months-starting-september-2025-08-28/

[4] August jobs report due out as Fed uncertainty looms [https://finance.yahoo.com/news/august-jobs-report-due-out-as-fed-uncertainty-looms-what-to-watch-this-week-125350194.html]

Decoding blockchain innovations and market trends with clarity and precision.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet