Assessing Illinois Tool Works' Valuation and Momentum: A Compelling Entry Point for Long-Term Investors?

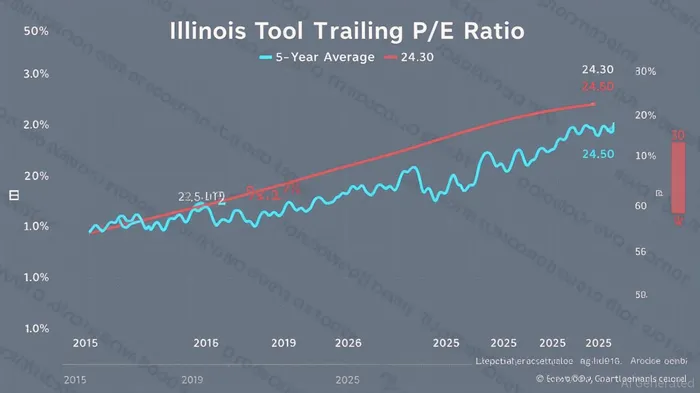

Illinois Tool Works (ITW) has long been a stalwart in the industrial sector, known for its diversified business model and disciplined capital allocation. As of September 2025, the stock trades at a trailing P/E ratio of 23.46 [1], slightly below its 5-year average of 24.75 [2]. This raises a critical question: Is ITW's valuation currently undervalued, fairly priced, or overextended? To answer this, we must dissect its valuation constraints, cash flow consistency, and technical momentum indicators.

Valuation Trends: A Mixed Signal

The current P/E ratio of ITWITW-- sits near historical averages, with minor variations across sources (22.06 to 23.46) due to differing calculation dates and data providers [1]. A 5-year average of 24.75 [2] suggests the stock is trading at a slight discount to its long-term valuation. However, this metric alone is insufficient. The industrial sector's broader context matters: peers like Ingersoll RandIR-- (IR) trade at a P/E of 25.95 [3], while Gates IndustrialGTES-- (GTES) sits at 18.69 [4]. ITW's valuation appears reasonable relative to its peers, but the lack of a clear discount—coupled with its stable, non-cyclical earnings—means investors should not expect a “bargain-bin” entry point.

Cash Flow Consistency: A Pillar of Strength

ITW's free cash flow (FCF) generation remains a standout. In Q2 2025, the company produced $449 million in FCF, with a 59% conversion rate from net income [5]. While this fell short of historical averages due to one-time items, management expects to exceed 100% FCF conversion for the full year. This resilience underscores ITW's operational discipline, particularly in a mixed macroeconomic environment. Moreover, the $1.5 billion share repurchase program announced in Q2 [5] signals confidence in its valuation and commitment to shareholder returns. For long-term investors, consistent FCF and aggressive buybacks are hallmarks of a company that can compound value over time.

Technical Momentum: Neutral Territory

Technically, ITW's stock has shown stability but lacks explosive momentum. As of September 2025, its RSI of 47.13 [6] places it in neutral territory, far from overbought (70) or oversold (30) levels. The 50-day moving average ($259.77) and 200-day moving average ($250.68) [7] suggest a sideways trend, with the stock trading near the upper end of its 52-week range. This pattern indicates a lack of strong directional bias, which could deter momentum traders but suits long-term investors seeking a steady entry point. However, the absence of a clear breakout or breakdown means patience is required.

The Verdict: A Compelling Entry Point?

ITW's valuation is neither undervalued nor overvalued by historical or sector standards. Its FCF consistency and capital allocation strategy are robust, providing a solid foundation for long-term growth. Technically, the stock is in a holding pattern, which could either signal consolidation ahead of a move or a lack of catalysts. For long-term investors, the key risks include macroeconomic headwinds and earnings volatility in its more cyclical segments. However, ITW's diversified business model and strong balance sheet mitigate these risks.

If the stock remains near current levels, it could represent a compelling entry point for those willing to hold through short-term volatility. The forward P/E of 24.30 [8] and management's full-year guidance [5] suggest earnings growth is likely to justify the current valuation over time. That said, investors should monitor technical indicators for a potential breakout above $260—a level that could signal renewed institutional interest.

In conclusion, ITW is not a screaming buy, but it is a stock worth watching. Its valuation is anchored to fundamentals, and its technicals suggest a patient, methodical approach. For long-term investors, the combination of stable cash flows and a valuation in line with history makes ITW a candidate for a diversified portfolio—provided they are prepared to hold through the inevitable ups and downs of the industrial sector.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet