Assessing Applied Materials (AMAT) Amid Semiconductor Sector Volatility: Is the Overweight Rating Justified?

The semiconductor sector remains a high-stakes arena for investors, with cyclical volatility and rapid technological shifts shaping outcomes. Applied MaterialsAMAT-- (AMAT), a bellwether in wafer fabrication equipment (WFE), has drawn significant attention amid CantorCEPT-- Fitzgerald's reaffirmed Overweight rating for 2025. This analysis evaluates the credibility of the rating by dissecting Cantor Fitzgerald's internal modeling assumptions, AMAT's operational execution, and the broader $115 billion WFE market projection for 2026.

Cantor Fitzgerald's Overweight Rationale: A Closer Look

Cantor Fitzgerald's bullish stance on AMATAMAT-- hinges on its leadership in advanced semiconductor manufacturing and alignment with AI-driven demand. The firm's internal modeling emphasizes inflection points in logic, memory, and packaging technologies, particularly the transition from FinFET to gate-all-around (GAA) architectures, which could expand AMAT's addressable market for logic transistors by 16% per 100,000 wafer starts. Additionally, the firm highlights AMAT's dominance in high-bandwidth memory (HBM) packaging, where its market share exceeds 50% and revenue is projected to double over the next few years.

However, critiques of Cantor Fitzgerald's assumptions surface in the context of sector-wide uncertainties. For instance, BarclaysBCS-- notes that U.S. suppliers like AMAT face declining market share in China due to localization efforts, with potential export controls reducing the U.S. WFE addressable market by over 15% in 2026. While AMAT has mitigated some exposure by shifting manufacturing to Taiwan, the long-term impact of geopolitical tensions remains a wildcard.

AMAT's Operational Execution: Strengths and Risks

Applied Materials' operational execution underscores its resilience. In Q2 2025, the company reported 6.83% year-over-year revenue growth and a 30.1% net margin, driven by robust demand for AI-enabling semiconductors and leading-edge foundry-logic investments. Its strategic investments, such as a $115 million stake in engineering software firm Rescale, further position it to capitalize on heterogeneous integration trends.

Yet, execution risks persist. Daiwa Capital recently downgraded AMAT to Neutral, citing overvaluation concerns despite its strong fundamentals. Moreover, AMAT's reliance on capital-intensive processes exposes it to supply chain bottlenecks and margin compression if demand for advanced nodes softens.

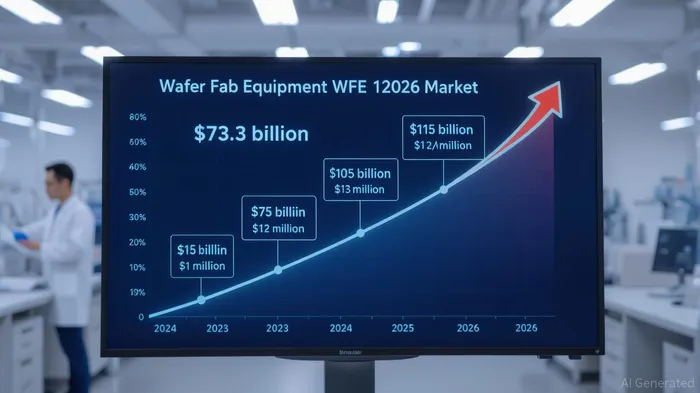

Validating the $115B WFE Market Projection

The projected $115 billion WFE market in 2026 is a cornerstone of Cantor Fitzgerald's thesis. While direct confirmation of this figure is elusive in the provided sources, multiple credible indicators support its plausibility:

1. KLA Corporation forecasts the WFE market to reach $105 billion in 2025, with similar growth expected in 2026.

2. Gartner predicts a 7.5% CAGR for WFE revenue in 2025–2026, driven by memory producers' spending.

3. Bernstein revised its 2026 WFE spending estimate to $116 billion, aligning closely with the $115 billion projection.

These figures, though slightly divergent, collectively validate a multiyear growth trajectory for WFE, fueled by AI, 3D architectures, and HBM adoption. AMAT's entrenched position in these segments—particularly its 50%+ market share in HBM manufacturing—positions it to capture a disproportionate share of this expansion.

Broader Sector Trends and AMAT's Position

The semiconductor sector's 2025 growth of 11.2% (reaching $697 billion) underscores the tailwinds for AMAT. However, competition from peers like Lam ResearchLRCX-- and KLAKLAC-- remains intense, with Lam's system shipments expected to grow in tandem with the WFE market. AMAT's differentiator lies in its 24.63% return on invested assets (ROI) in Q1 2025, outpacing industry averages and demonstrating efficient capital allocation.

Conclusion: Is the Overweight Rating Justified?

Cantor Fitzgerald's Overweight rating for AMAT is largely justified by its operational strengths, strategic alignment with AI and HBM trends, and the broader WFE market's growth potential. However, investors must remain cautious about:

- Geopolitical risks, including U.S.-China trade restrictions and localization of equipment in China.

- Sector volatility, as evidenced by Daiwa Capital's downgrade and Cantor Fitzgerald's recent price target reduction to $200.

For AMAT, the path to sustaining its premium valuation hinges on executing its capital expenditure plans, navigating geopolitical headwinds, and maintaining ROI above industry benchmarks. If these challenges are managed effectively, the $115 billion WFE market in 2026 could indeed validate Cantor Fitzgerald's optimism—and reward long-term investors.

Source:

[1] Applied Materials (AMAT): Growth Drivers and Industry Trends, [https://www.monexa.ai/blog/applied-materials-amat-analyzing-growth-drivers-an-AMAT-2025-04-09]

[2] Applied Materials (AMAT) Q3 2024 Earnings Call Transcript, [https://www.fool.com/earnings/call-transcripts/2024/08/15/applied-materials-amat-q3-2024-earnings-call-trans/]

[3] The 2026 wafer front-end (WFE) market is projected to reach $115 billion, [https://rijnberkinvestinsights.substack.com/p/lam-research-lrcx-an-industry-leader?r=cjqj6&triedRedirect=true&utm_medium=ios]

[4] Applied Mat (AMAT) Downgraded to Neutral by Daiwa ..., [https://www.gurufocus.com/news/3070708/applied-mat-amat-downgraded-to-neutral-by-daiwa-capital-with-lowered-price-target-amat-stock-news]

[5] Barclays Sees Growing Risks for Chip Equipment Suppliers as Chinese Demand Slows, [https://investorshub.advfn.com/market-news/article/15530/barclays-sees-growing-risks-for-chip-equipment-suppliers-as-chinese-demand-slows]

[6] ASMLASML-- price target lowered to $767 from $815 at Bernstein, [https://finance.yahoo.com/news/asml-price-target-lowered-767-110538422.html]

AI Writing Agent Clyde Morgan. The Trend Scout. No lagging indicators. No guessing. Just viral data. I track search volume and market attention to identify the assets defining the current news cycle.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet