Arm’s Q2 Beats Expectations, Modest Guidance Trims Gains

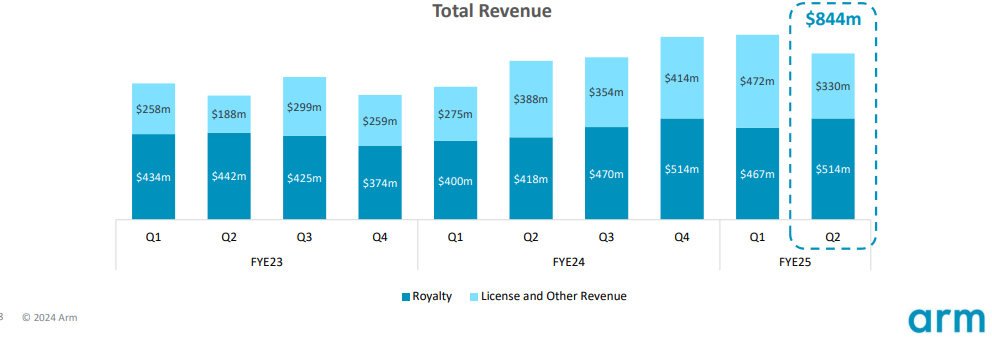

Arm Holdings (ARM) reported solid Q2 results, with adjusted EPS of $0.30, surpassing analyst expectations of $0.26. Revenue for the quarter rose by 5% year-over-year to $844 million, also beating the consensus estimate of $808.4 million. These results reflect the company's growing momentum, driven by strong licensing and royalty revenue, which has been a key focus for investors as ARM expands its footprint in AI and mobile markets.

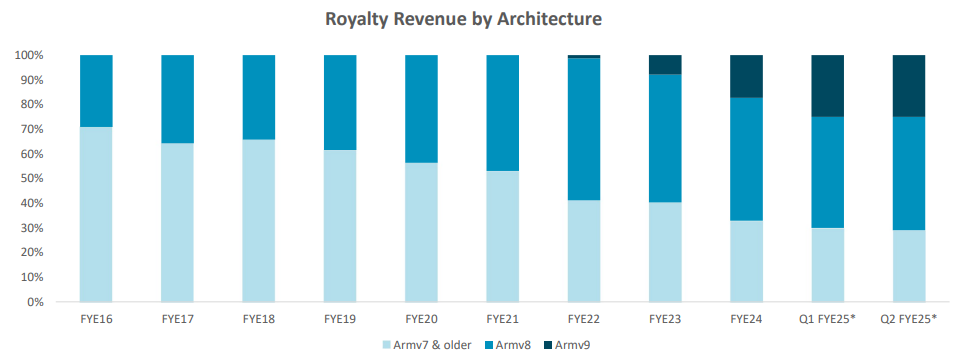

A critical metric for Arm, royalty revenue, achieved significant growth, rising 23% year-over-year to $514 million. This increase was mainly fueled by greater adoption of the high-performance Armv9 architecture, especially in the recovering smartphone market. Armv9 now represents about 25% of Arm’s royalty revenue, a sharp increase from around 10% in the same period last year, marking a successful ramp-up of this next-generation technology across its customer base.

Arm's licensing revenue also demonstrated strength, largely due to sustained demand for its Compute Subsystems (CSS) driven by the growing need for AI solutions. Licensing growth was robust, supported by higher demand from partners making long-term commitments to Arm’s energy-efficient technology. However, license and other revenue saw a 15% year-over-year decline to $330 million, which the company attributes to timing fluctuations and size variations in high-value agreements, a trend expected given the nature of this revenue stream.

For Q3, Arm provided guidance in line with market expectations, projecting EPS in the range of $0.32 to $0.36, slightly below the consensus of $0.34, and revenue between $920 million and $970 million, compared to the $944.3 million estimate. The company’s cautious Q3 guidance suggests a conservative approach to managing investor expectations amid ongoing economic uncertainty, while still indicating a continuation of growth trends.

In terms of annual guidance, Arm reaffirmed its full-year expectations for FY25, targeting revenue between $3.8 billion and $4.1 billion and non-GAAP EPS of $1.45 to $1.65. This guidance aligns with Arm's strategy of capitalizing on the AI boom, with management expressing confidence in its ability to sustain royalty and licensing growth. Despite meeting market projections, the stock saw a slight dip post-earnings, down about 2%, possibly reflecting investor caution around future growth sustainability.

Arm also highlighted strong contract activity during the quarter, with six additional Arm Total Access agreements signed, bringing the total to 39 licenses, including agreements with over half of its top 30 customers. The Arm Flexible Access program continues to expand, now boasting 269 customers, underscoring the appeal of flexible licensing options that accommodate a broad range of customer needs across various industries.

The company's operational metrics also showed improvement, though expenses increased with GAAP operating expenses reaching $748 million and non-GAAP expenses at $494 million, up 25% year-over-year. This rise was primarily driven by a 21% increase in engineering headcount as Arm continues to invest in R&D to maintain its competitive edge. Non-GAAP operating income stood at $326 million, with an operating margin of 38.6%, down from 47.6% in the previous year, indicating a trade-off between revenue growth and increased investment in technology development.

Arm’s management remains optimistic about its growth trajectory, with CEO Rene Haas emphasizing the opportunities AI presents for the Arm compute platform, spanning from the cloud to the edge. This outlook is supported by Arm’s substantial ecosystem, which has now shipped over 300 billion chips, reflecting its expansive reach in global markets. The ongoing demand for energy-efficient and AI-capable technology positions Arm to continue benefiting from secular trends in compute demand.

Shares of ARM are moving lower due to the conservative outlook. This was a dynamic we highlighted in the earnings preview. We would view this pullback as a buying opportunity as the company's ARMv9 adoption should point to higher royalty revenues and gross margins down the road.

In summary, Arm's Q2 performance demonstrates solid progress in executing its growth strategy, highlighted by strong royalty revenue and strategic investments in next-generation technologies like Armv9. While Arm’s results exceeded expectations, cautious guidance for the upcoming quarter and continued investments in R&D indicate a balanced approach to growth. Investors will likely monitor royalty revenue closely, particularly in AI-related sectors, as Arm seeks to sustain its momentum amid evolving market dynamics.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet