Arm Plunges Below $100 After Earnings: One “Miss” Spooks Investors as $80 Back in Play

Arm’s quarter was “good” on paper, but the stock traded like it failed an exam it didn’t know it was taking. After reporting, shares knifed down to about $90 in the initial reaction, breaking below the $100 psychological level and printing the lowest levels since late April 2025, with the $80 April lows back on the radar as tech sentiment stays fragile. The bounce off the lows helps, but the price action effectively flipped $100 from “support” into “overhead supply,” meaning Arm now has to earn its way back through that level rather than simply drift there.

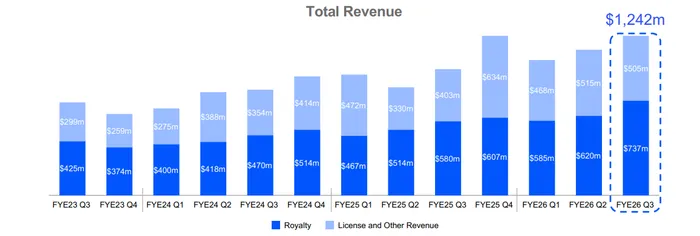

Fundamentally, Arm delivered a modest beat versus expectations and guided slightly above consensus, but that wasn’t enough in a market that is increasingly allergic to anything short of a clear upside surprise. For fiscal Q3 (December quarter), ArmARM-- posted adjusted EPS of $0.43 versus ~$0.41 expected, and revenue of about $1.24B versus expectations clustered around ~$1.22–$1.23B. Management described it as a record quarter and the fourth consecutive billion-dollar revenue quarter, with strength across smartphones, data center, and emerging “edge/physical AI” use cases. So why did investors sell first and ask questions later?

The main “tell” in the report was licensing. License and other revenue rose 25% year over year to $505M, but it came in below the ~$520M area that the Street was looking for. That shortfall is not catastrophic in isolation (licensing is inherently lumpy), but it matters because licensing is one of the cleanest signals of forward demand and pricing power for Arm’s next-gen IP. When the market is already jittery about tech spending and handset volumes, a licensing miss is interpreted less as “timing” and more as “is demand normalizing?”—especially at Arm’s premium valuation bar.

Royalties, meanwhile, were the bright spot. Royalty revenue increased 27% year over year to a record $737M, driven by higher royalty rates per chip from Armv9 and Compute Subsystems (CSS) adoption, plus strong momentum in data center. The company has been very explicit that CSS is changing the value-capture equation: more customers are signing higher-value licenses, more devices are shipping CSS-based silicon, and that richer mix lifts royalty rates even if unit growth is merely okay. Those are the right ingredients for a high-quality royalty story, and several analysts pointed to CSS and data center as the structural tailwinds that should increasingly dominate the narrative.

Guidance was technically “fine,” which was the problem. Arm guided fiscal Q4 revenue to about $1.47B (±$50M) versus consensus around $1.44B and guided adjusted EPS around $0.58 (±$0.04) versus consensus around $0.57. In a calmer tape, that’s a beat-and-raise style outcome. In this tape, “slightly better” can still be read as “not enough,” particularly when the stock is trying to hold a key technical level and investors are scanning for any sign that the next quarter’s royalty growth rate might decelerate.

That deceleration anxiety ties directly into the primary near-term headwind: smartphone supply chain constraints driven by rising memory prices and shortages. Arm acknowledged that memory issues could weigh on handset unit volumes, which is especially important because smartphones remain Arm’s largest end market and still represent a large share of the royalty base even as data center grows. Management tried to defuse the concern by arguing the impact should be concentrated at the low end of the handset market (older architectures with much lower royalties), while premium devices—where Armv9 and CSS are more prevalent and royalty rates are higher—should be more resilient. But the market’s immediate reaction wasn’t to debate elasticity models; it was to de-risk anything tethered to smartphone build uncertainty.

Arm also got hit by guilt-by-association from Qualcomm’s weak outlook. Qualcomm explicitly blamed memory constraints for its Q2 shortfall, and that quickly became the macro “explanation” investors pasted onto the entire smartphone-adjacent complex. When one major node in the chain says memory is now “defining the size of the mobile market,” investors naturally assume Arm’s handset royalties face the same ceiling risk in the near term, even if Arm’s mix is improving.

Margins and operating income were another underappreciated friction point. Arm is investing aggressively in R&D, and that is pressuring operating leverage. The company reported non-GAAP operating income of $505M and a non-GAAP operating margin of 40.7%, down from 45.0% a year ago; GAAP operating margin also stepped down to 14.9% from 17.8%. In other words, growth is strong, but profitability is not expanding in lockstep because Arm is spending into the opportunity set (CSS, next-gen architectures, and potential broader silicon ambitions). Investors can live with that when the stock is ripping and fundamentals are surprising to the upside; they’re less forgiving when the stock is already under pressure and the quarter contains a couple “not perfect” line items.

A separate, quieter headwind is bookings/visibility optics. Arm disclosed that remaining performance obligations (RPO) declined 8% year over year to about $2.15B. RPO isn’t the only truth-teller for a licensing model, but in a quarter where licensing already missed expectations, a lower RPO figure can reinforce the perception that growth may be normalizing, even if the underlying driver is simply deal timing.

On the positive side, Arm’s longer-term story remains intact, and management leaned hard into it. The company highlighted rapid progress in data center and networking, with Arm architectures increasingly embedded across hyperscalers’ custom silicon strategies, plus growing relevance as AI shifts from training-heavy workloads to inference-heavy, agentic systems that require CPU-led orchestration and power efficiency. That is the strategic reason investors pay up for Arm: it’s not just “phones,” it’s the instruction set and ecosystem increasingly sitting underneath modern compute, from edge devices to cloud infrastructure.

Finally, investors have a near-dated catalyst that could help reframe sentiment: Arm announced it will host its “Arm Everywhere” event on March 24, 2026, where markets expect more clarity around its silicon strategy and broader roadmap. With the stock now having put a fresh scar below $100, that event becomes more important—not because it guarantees upside, but because it can reduce uncertainty around how Arm intends to expand value capture beyond the current licensing/royalty model.

Bottom line: Arm beat and guided slightly above, but the market reaction was driven by a high valuation bar, a licensing revenue miss, lingering smartphone/memory worries amplified by Qualcomm, and margin pressure tied to heavy R&D investment. Near term, $100 is the line in the sand on the chart—now resistance—while fundamentals will need to keep proving that data center/CSS mix shift can offset any handset volume turbulence without sacrificing profitability.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet