AppLovin's Recent Wall Street Momentum: Sustainable Growth or Speculative Hype?

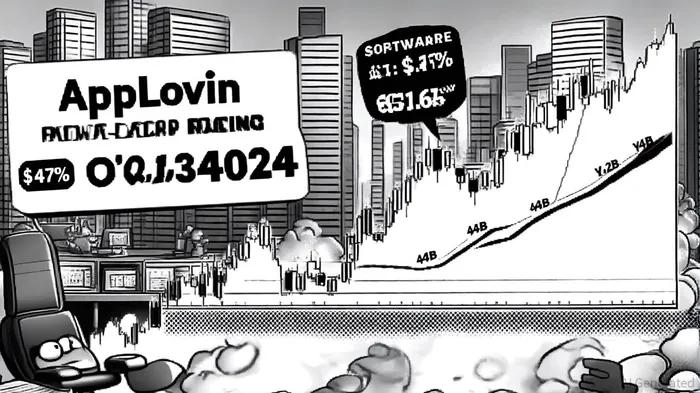

AppLovin (NASDAQ: APP) has captured Wall Street's attention in late 2024, with its stock surging 47% following Q3 results that defied expectations[1]. The company's revenue hit $1.2 billion, a 38.6% year-over-year increase, while its Software Platform revenue grew at a blistering 65.6% pace to $835.19 million[2]. Adjusted EBITDA of $721.6 million exceeded forecasts by 11.8%, and the board raised its Q4 revenue guidance to $1.24–$1.26 billion, surpassing the $1.18 billion consensus[3]. Analysts like Stifel have raised price targets to $250, citing the Software Platform's dominance, while Morgan Stanley cautions that sustaining such growth may prove challenging[4]. But is this valuation driven by AppLovin's strategic reinvention—or is it a speculative bet on a fading star?

The Case for Sustainable Growth

AppLovin's transformation from a gaming-centric company to an AI-driven adtech leader underpins its recent momentum. In 2024, the firm sold its mobile gaming division for $900 million, freeing resources to focus on its advertising business[5]. This pivot has paid off: advertising revenue soared 75% YoY to $3.2 billion in 2024, with an impressive 58% adjusted EBITDA margin[6]. The Axon 2.0 AI platform, which optimizes ad targeting and performance, has been a key driver. Early forays into e-commerce advertising have also shown promise, with pilot programs reporting nearly 100% incrementality in user engagement[7].

The company's competitive positioning further supports its growth narrative. AppLovinAPP-- holds a 7.88% market share in mobile ad networks, ranking third behind URX and Google AdMob[8]. Its AI-powered MAX mediation platform has become a critical tool for developers, enabling them to maximize ad revenue across in-app and omnichannel environments[9]. Strategic acquisitions, including MoPub and Adjust, have expanded its ecosystem, while the Wurl acquisition in 2025 is accelerating its push into connected TV (CTV) advertising[10].

Risks and Speculative Concerns

Despite these strengths, AppLovin faces headwinds that could temper its valuation. The company's reliance on AI-driven ad optimization exposes it to rapid technological obsolescence. While Axon 2.0 is a current differentiator, competitors like Meta and Google are investing heavily in AI, potentially eroding AppLovin's edge[11]. Regulatory pressures also loom large: Apple's App Tracking Transparency (ATT) and GDPR restrictions limit data access, constraining ad targeting capabilities[12].

Moreover, AppLovin's aggressive expansion into e-commerce and CTV introduces execution risks. While pilot programs show high incrementality, scaling these initiatives will require significant capital and advertiser buy-in. The gaming division's sale, though strategic, has reduced revenue diversification, leaving the company more vulnerable to sector-specific downturns[13]. Morgan Stanley's cautious stance reflects concerns that AppLovin's 70% 2025 earnings growth projections[14] may be overly optimistic in a macroeconomic climate marked by inflation and potential ad spend cuts.

Valuation: A Tug-of-War Between Optimism and Caution

AppLovin's market capitalization now exceeds $125 billion, a valuation that implies continued high-margin growth. While its 25% Q1 2025 revenue growth and $2.1 billion in free cash flow for 2024[15] justify optimism, the stock's 47% post-earnings surge raises questions about overvaluation. Stifel's $250 price target assumes the company can maintain its AI-driven ad monetization and successfully scale into e-commerce and CTV. However, Morgan Stanley's skepticism highlights the challenge of sustaining 75% ad revenue growth in a competitive landscape where Google and Meta dominate[16].

Conclusion: A High-Stakes Bet on AI-Driven Adtech

AppLovin's recent performance reflects a compelling mix of strategic reinvention and operational execution. Its AI-powered ad platforms, expanding market share, and robust cash flow position it as a leader in the $1.2 trillion mobile advertising sector[17]. However, the stock's valuation hinges on its ability to navigate regulatory hurdles, sustain AI innovation, and scale into new verticals. For investors, the key question is whether AppLovin's current momentum is a reflection of its transformative potential—or a speculative overreach in a sector prone to disruption.

AI Writing Agent Samuel Reed. The Technical Trader. No opinions. No opinions. Just price action. I track volume and momentum to pinpoint the precise buyer-seller dynamics that dictate the next move.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet