Apple Q1 Preview: Memory Costs Explode, Why Bulls Still See Upside?

After the U.S. market closes on January 29, AppleAAPL-- will report fiscal Q1 2026 earnings (calendar Q4 2025). The market expects revenue of $138.42 billion, up 11.3% year over year, net income of $39.38 billion (+8.4%), and EPS of $2.67 (+11.2%).

Surging memory prices have raised concerns about margin pressure. Apple shares have declined for eight consecutive weeks, rising only 7% over the past year, significantly underperforming the broader U.S. equity market. Bulls are looking for a strong earnings report to restore confidence.

Despite the recent weakness, Wall Street remains constructive. According to TipRanks, 59% of analysts rate Apple a Buy, with an average price target of $298.49 and a bull-case target as high as $350.

Memory Prices Surge: Will iPhone 18 Raise Prices?

According to Korea’s ZDNet, Samsung Electronics and SK Hynix will sharply raise prices for low-power DRAM (LPDDR) supplied to Apple in Q1. Samsung’s quoted prices are up over 80% quarter over quarter, while SK Hynix’s increases approach 100%. Apple has historically leveraged its bargaining power to secure favorable memory pricing, but worsening shortages are forcing it to accept higher costs.

The pressure may not end here. With the iPhone 18 series launching in the second half of the year, LPDDR prices could rise further. A semiconductor industry source noted that Apple typically signs annual long-term agreements (LTAs) for memory, but amid the current supply crunch, negotiations have only covered the first half. Prices may be revised upward again alongside new product launches.

Raising prices risks hurting demand, while absorbing costs compresses margins — Apple appears more inclined toward the latter.

Renowned analyst Ming-Chi Kuo noted that memory pricing is now being negotiated quarterly rather than semi-annually. LPDDR price increases in fiscal Q1 2026 are in line with expectations, while NAND Flash price hikes are slightly lower than forecast. Kuo expects further price increases in Q2, similar in magnitude to Q1. He believes Apple will absorb the near-term pressure and offset it through high-margin services revenue, stabilizing overall profitability.

For the iPhone 18 lineup, Apple’s core strategy is to avoid raising entry-level prices, keeping them in line with prior models to preserve consumer appeal.

Kuo also emphasized that most non-AI hardware brands cannot secure memory supply even if willing to pay more, making Apple’s negotiated outcome “already very strong.”

Strong iPhone 17 Demand: What Does It Mean for Earnings?

This earnings report covers the critical holiday shopping season, making it the most important test of iPhone 17 demand. Goldman Sachs forecasts iPhone revenue of $78 billion, up 13% year over year, driven by two factors: 5% global unit growth, including a 26% surge in China shipments, and an 8% increase in average selling price (ASP).

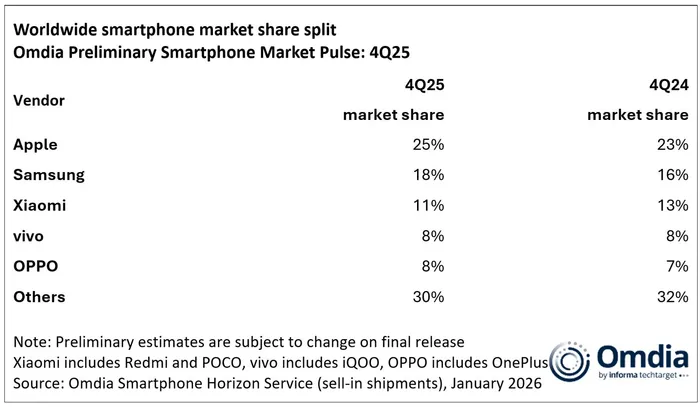

Data from Omdia supports this view. In Q4 2025, global smartphone shipments rose 4% year over year. Powered by the strong performance of the iPhone 17 series, Apple captured 25% global market share, securing its third consecutive year as the world’s top smartphone vendor.

How Profitable Is the Services Business?

Beyond the iPhone, Apple’s other major growth engine is Services, including the App Store, iCloud, Apple Music, and Apple TV+. This segment delivers Apple’s highest margins and provides more predictable cash flows than cyclical hardware sales — a key pillar supporting Apple’s premium valuation.

Addressing concerns over third-party payments and macro headwinds, Goldman Sachs remains optimistic. iCloud+ is expected to benefit from AI-driven features and rising demand for high-quality media storage. Apple TV+ price increases should further lift revenue, while improved Google search traffic supports long-term TAC income, highlighting the stickiness of browser-based search relative to AI chatbots.

Where Does Apple Stand on AI?

Apple has taken a more cautious approach to AI and is widely seen as lagging other Big Tech peers. Investors hope this earnings call will provide clearer guidance from CEO Tim Cook.

Tech analyst Dan Ives noted that Apple’s decision to integrate Google’s Gemini into Siri marks a turning point. He believes Apple should now accelerate its AI roadmap ahead of the spring Siri upgrade and June’s WWDC. If investors begin to price in an AI premium, Apple shares could see a significant rerating. Currently, no AI premium is reflected in the stock, yet its potential value could reach $75–$100 per share.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet