Apple Earnings Preview Will iPhone 17 Spark the Next Upgrade Cycle?

Apple will report its fiscal Q4 2025 results (corresponding to the natural Q3 of 2025) after the U.S. market closes on October 30.

Since the start of the AI era, AppleAAPL-- has lagged behind peers, with its stock performance ranking last among the “Magnificent Seven.”

However, the strong sales of the iPhone 17 series have helped Apple make a stunning comeback.

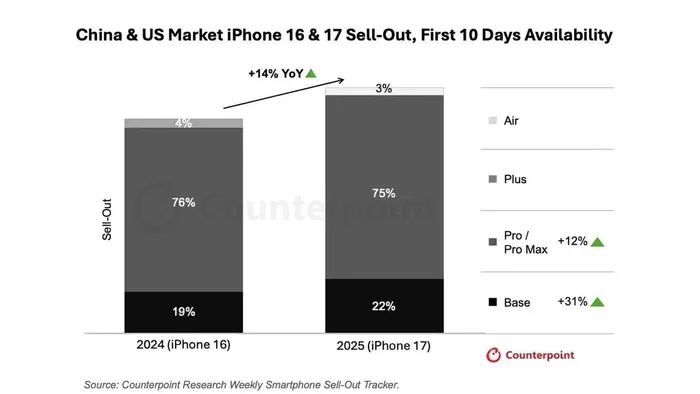

According to Counterpoint Research, iPhone 17 sales during the first 10 days after launch were up 14% compared with the iPhone 16 series. The long-awaited replacement cycle appears to be underway.

iPhone 18 Rumors Point to Continued Momentum

Even as the iPhone 17 is selling strongly, leaks about the iPhone 18 have already surfaced.

The iPhone 18 series is expected to feature the A20 chip built on a 2-nanometer process, offering 15% better performance and 30% lower power consumption versus its predecessor.

The iPhone 18 Pro may introduce a variable aperture main camera, allowing users to control light intake based on shooting conditions.

Apple may also launch its first foldable iPhone, potentially extending the current upgrade boom for another two years.

Services: Apple’s Hidden Profit Engine

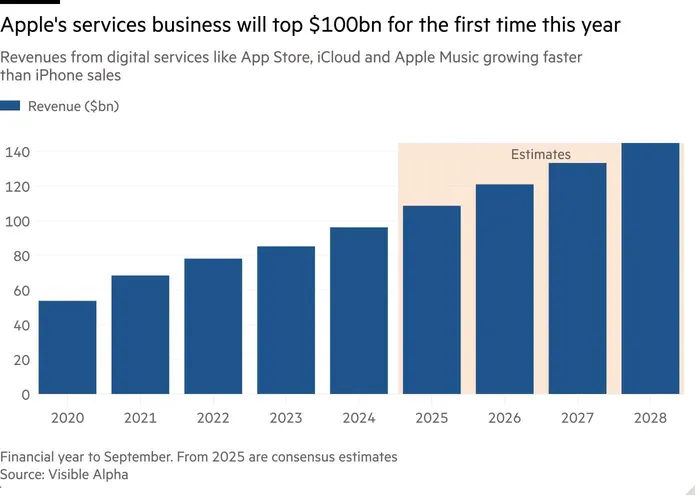

Apple’s second growth pillar lies in its services business, which includes iCloud, Apple Music, and the App Store. This segment now accounts for one-third of total revenue, and its gross margin of 75% far exceeds that of the iPhone (around 40%).

As a result, the rising share of high-margin services has lifted Apple’s overall gross margin from 38% in 2020 to 47% today.

Evercore ISI analysts believe Apple’s double-digit growth trend in services will continue, especially now that several legal disputes have been settled.

According to a Financial Times report citing Visible Alpha, Apple’s services revenue is projected to reach $108.6 billion this quarter, up 13% year over year. By 2030, services could account for over 30% of total revenue, potentially generating $175 billion per quarter.

Future Catalysts and Valuation Risks

Apple is also working to bring Apple Intelligence to China and expand into live sports streaming, both potential catalysts for long-term services growth.

However, valuation remains a concern.

Apple’s forward P/E ratio exceeds 39x, well above its 10-year average of 23x and the Nasdaq 100 average, making it the second most expensive stock among the Magnificent Seven — behind only Tesla.

If Apple fails to deliver impressive growth numbers, investors may reprice its lofty valuation quickly.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet