Seven & i's Erosion of Earnings Momentum: A Case of Operational and Strategic Fragility in Japan's Retail Sector

Seven & i's Erosion of Earnings Momentum: A Case of Operational and Strategic Fragility in Japan's Retail Sector

The erosion of earnings momentum at Seven & i Holdings, the Japanese retail giant behind the 7-Eleven brand, has become a cautionary tale of operational inefficiencies and strategic missteps in a fiercely competitive market. While the company reported a 11.4% year-over-year increase in operating profit for the first half of FY2025, reaching ¥208.3 billion, this figure masked a deeper malaise: a 6.9% decline in operating revenue to ¥5,616.6 billion and a subsequent 24% drop in profits by Q3 2025, according to Investing.com slides. These numbers, as highlighted by Bloomberg and Reuters, underscore a troubling pattern of volatility that raises questions about the sustainability of Seven & i's business model.

Operational Inefficiencies: A House of Cards?

Seven & i's operational challenges are rooted in its sprawling, fragmented structure. The company's attempt to diversify beyond convenience stores-into supermarkets, department stores, and financial services-has proven to be a double-edged sword. While convenience stores account for 62% of its revenue, underperforming segments like department stores and supermarkets have dragged down overall profitability, according to a DCFmodeling SWOT analysis. For instance, that analysis noted the department store segment reported a ¥13 billion loss in 2022, a problem Seven & i has tried to address by spinning off these units into York Holdings. Yet, this restructuring has not stemmed the bleeding.

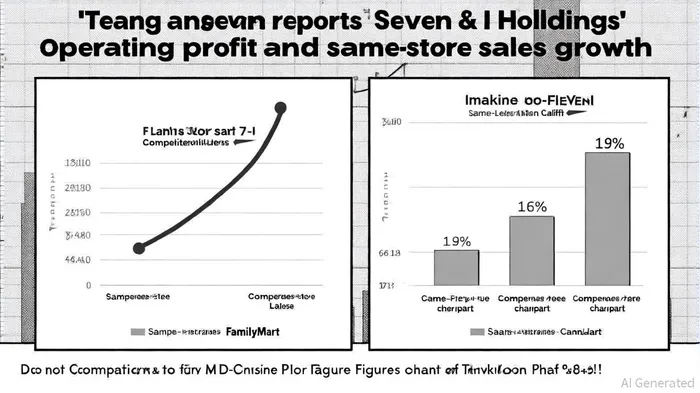

In contrast, rivals like Lawson and FamilyMart have maintained laser-like focus on convenience stores, leveraging agile supply chains and localized strategies to outperform Seven & i. A Business Gurus analysis found Lawson and FamilyMart posted faster same-store sales growth in 2025, a metric that Seven & i has struggled to match. This gap is not trivial; it reflects a fundamental inability to adapt to shifting consumer behavior, particularly among price-sensitive demographics.

Strategic Weaknesses: A Lack of Clarity

Seven & i's strategic direction has been further clouded by corporate governance issues and a failed $47 billion takeover bid from Alimentation Couche-Tard. The collapse of this bid exposed structural weaknesses in Japan's corporate governance framework, according to a Morningstar report. This uncertainty has compounded operational challenges, with management now prioritizing short-term fixes-like store closures and asset sales-over long-term innovation.

The company's reliance on convenience stores, while a strength in theory, has also become a liability. For example, Seven & i's U.S. operations, which contribute over 75% of its consolidated revenue, have seen same-store sales decline every month in 2025, as Bloomberg reported. This underperformance is exacerbated by rising energy costs, inflation, and a saturated market. Meanwhile, initiatives like the 7NOW delivery service and SEVEN CAFÉ Bakery expansion, while promising, are still in their early stages and have yet to translate into meaningful profit growth (see Investing.com slides).

A Fragile Path Forward

Seven & i's recent guidance-forecasting a 147.3% increase in net income for FY2025-hinges on the completion of structural reforms and a ¥600 billion share buyback program (noted in the Morningstar report). However, this optimism is tempered by the reality of a 23% earnings decline in the fiscal year ending February 2025, as Bloomberg documented. The company's plans to list York Holdings and streamline operations may provide liquidity, but they also risk alienating franchisees, who have already expressed frustration over management's lack of responsiveness, according to the Business Gurus analysis.

Moreover, Seven & i's global ambitions, such as its acquisition of the 7‑Eleven chain in Australia, have yet to yield significant returns. While the company anticipates Australia's full-year contribution to drive EBITDA growth, one-time acquisition costs have temporarily depressed operating income, as noted in the Morningstar report. This pattern-of short-term pain for long-term gain-has left investors skeptical, particularly in a market where competitors are executing with greater precision.

Conclusion: A Race Against Time

For Seven & i, the clock is ticking. The company's operational inefficiencies and strategic ambiguities have created a fragile foundation, one that may not withstand further macroeconomic headwinds. While its focus on convenience stores and digital innovation offers a glimmer of hope, the broader challenges-ranging from corporate governance flaws to a saturated domestic market-remain unresolved. Investors would be wise to monitor Seven & i's progress closely, but the current trajectory suggests that the road to recovery will be long and fraught with obstacles.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet