Amex Crushes Earnings — But Credit Jitters Keep This Wall Street Favorite Trapped in a $300–$350 Holding Pattern

American Express posted another strong quarter , solidifying its position as the premium bellwether of consumer credit while offering just enough reassurance to calm nerves over rising credit concerns in the broader financial sector. The company reported third-quarter earnings per share of $4.14, up 19% from last year and comfortably ahead of the $4.00 consensus estimate. Revenue climbed 11% year over year to a record $18.4 billion, topping forecasts of $18.0 billion. The results reaffirmed that Amex continues to execute its playbook—leveraging a loyal, affluent customer base and expanding high-fee products—though the surrounding environment suggests limited multiple expansion as investors remain skittish about credit markets.

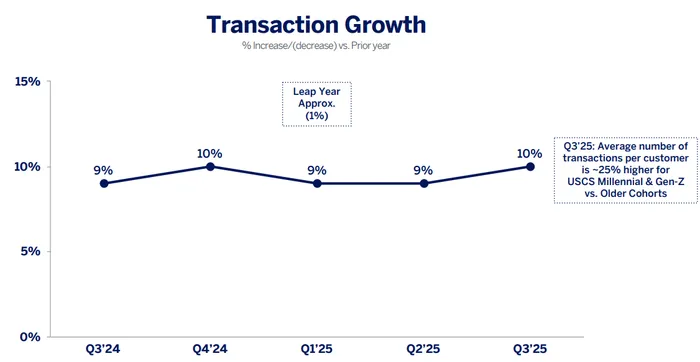

The quarter’s performance reflected the resilience of the company’s core franchise. Card member spending accelerated to 9% year over year, with strong demand for premium cards and elevated usage across travel and lifestyle categories. In particular, the company’s refreshed U.S. Consumer and Business Platinum Cards, launched in September, drew an exceptional response. CEO Stephen Squeri said that “new U.S. Platinum account acquisitions doubled compared to pre-refresh levels,” adding that early engagement has exceeded expectations. AmexAXP-- continues to dominate the high-income segment, where discretionary travel and entertainment spending remains durable, a key advantage amid growing economic crosscurrents. Spending growth in the upper brackets of the consumer economy has offset softer volumes among lower-tier cohorts, reinforcing Amex’s unique positioning relative to mass-market card issuers.

Compared to expectations, Amex delivered across the board. EPS of $4.14 beat by 14 cents, revenue topped forecasts by roughly $400 million, and both metrics marked acceleration from the second quarter’s pace. Net interest income rose on the back of higher revolving loan balances, while card fee revenue continued to climb as premium products captured more share. The company’s brand refresh cycle, which includes not just card benefits but also new digital tools like the Amex Travel App and its new Amex Ads platform, continues to deepen customer engagement and expand the addressable revenue base.

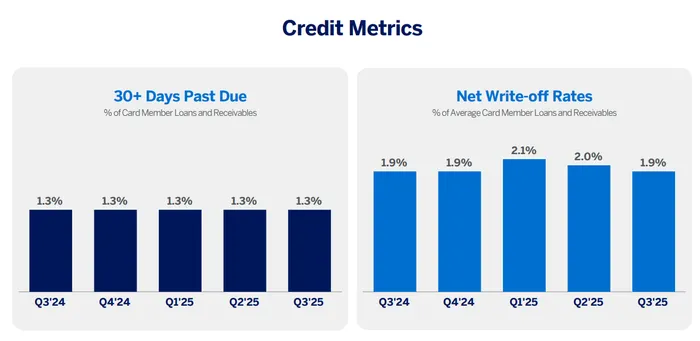

Crucially, credit quality held firm—an increasingly rare feat in the current environment. Provisions for credit losses fell slightly to $1.3 billion from $1.4 billion last year, thanks to smaller reserve builds and a stable net write-off rate of 1.9%, flat year over year. Delinquencies were contained, and management described credit metrics as “best-in-class.” While peers have begun to show creeping deterioration in late payments and rising losses in some subprime segments, Amex’s prime-heavy portfolio remains a stabilizer. Still, the company’s management did not ignore the backdrop of broader credit anxiety, noting that it continues to monitor spending and repayment trends closely as loan growth picks up. The slight uptick in net charge-offs quarter over quarter reflects a normalization trend more than distress—a dynamic the market appears comfortable with for now.

On the cost side, expenses increased 10% year over year to $13.3 billion, largely due to higher “customer engagement costs” tied to greater spending and travel benefit usage, as well as higher operating expenses. The effective tax rate also rose to 24.1% from 21.8%, reflecting global tax law changes. The expense profile remains a watch point as elevated benefit usage and technology investments offset some of the operating leverage from revenue growth. That said, Amex’s margin structure remains one of the healthiest in the card space, supported by strong fee income and disciplined underwriting.

The company raised its full-year 2025 guidance slightly. It now expects revenue growth of 9% to 10%, compared with the prior range of 8% to 10%, and earnings per share of $15.20 to $15.50, up from $15.00 to $15.50 previously. The revision signals quiet confidence that premium spending trends and membership fee momentum can carry through year-end despite macro headwinds. Squeri reiterated that Amex remains committed to its long-term financial algorithm: “We are confident in our growth prospects as we continue to execute our proven product refresh strategy and enhance our powerful Membership Model.”

From a capital markets perspective, Amex remains shareholder-friendly. The company returned over $2 billion to shareholders year to date through dividends and buybacks, underpinned by consistent free cash flow generation and a strong capital position. Its Tier 1 capital ratio and liquidity coverage remain well above regulatory thresholds, giving the firm room to maneuver should the credit environment tighten further.

Still, while fundamentals remain sound, the stock’s technical picture reflects investor caution. Shares of AXPAXP-- have oscillated between $300 and $350 since May, consolidating within a well-defined range as financials broadly face valuation resistance amid renewed credit-sector volatility. The stock currently trades near the midpoint of that band, and given the rising drumbeat of credit stress headlines—from regional banks to shadow finance—it’s unlikely investors will chase Amex aggressively higher in the near term. The company’s clean credit profile may insulate it, but macro contagion risk can still drive sector-wide derating. For now, the path of least resistance for the stock likely remains sideways to slightly lower if credit fears persist.

In sum, American ExpressAXP-- delivered what markets needed: a beat, a modest guidance raise, and no credit surprises. Spending trends remain robust, affluent customers are still swiping, and the card refresh cycle is paying off. Yet the broader market context—particularly the renewed scrutiny of credit quality and tightening financial conditions—suggests investors will stay selective within financials. Until the narrative around credit risk and funding stability calms, AXP looks poised to keep coiling in its established $300–$350 range—solidly engineered, but not yet ready for breakout speed.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet