AmeriServ Financial Climbs 43% in a Year: Should You Buy the Stock?

AmeriServ Financial, Inc. ASRV shares have gained 43.3% in the past year compared with the industry’s 13.8% growth. The company has outperformed other industry players, including Atlantic Union Bankshares Corporation AUB and Merchants Bancorp MBIN. Shares of AUBAUB-- and MBINMBIN-- have rallied 11.5% and 13%, respectively, in the same time frame. ASRVASRV-- benefits from diversified revenues, stable deposits, strong liquidity, margin expansion potential and strategic partnerships.

Image Source: Zacks Investment Research

A Key Look Into ASRV’s Business Operations

AmeriServ Financial is a Pennsylvania-based bank holding company formed in 1983 through its acquisition of AmeriServ FinancialASRV-- Bank. It primarily operates by managing its subsidiary, deriving income from banking, trust and wealth management services. It functions as a centralized unit overseeing management, accounting, risk, and other services. The Bank, chartered under Pennsylvania law, operates 16 branches across Pennsylvania and Maryland, offering retail and commercial banking services including loans, deposits, and financial products. It also manages wealth advisory services and oversees assets worth approximately $2.7 billion. Its operations include ATMs and loan production offices, serving customers mainly within a 250-mile radius of its headquarters in Pennsylvania, with a stable and regionally concentrated customer base.

AmeriServ Financial’s Key Tailwinds

AmeriServ Financial benefits from a diversified and stable revenue model anchored in traditional banking as well as fee-based wealth management operations. The company derives income from retail banking, commercial lending, and a sizeable trust and wealth management division administering approximately $2.7 billion in client assets, providing a recurring and relatively less capital-intensive revenue stream. This diversification reduces reliance on interest income alone and enhances earnings resilience across economic cycles.

Additionally, the wealth segment’s ability to offer investment products, retirement services, and institutional solutions positions the company to capitalize on rising demand for advisory services, particularly as demographic trends favor long-term savings and retirement planning.

The company’s strong core deposit franchise and liquidity profile remain notable. AmeriServASRV-- maintains a stable deposit base primarily composed of traditional banking products, which exhibit limited volatility and reduce dependence on higher-cost wholesale funding. The absence of brokered deposits and access to multiple liquidity channels, including FHLB and Federal Reserve facilities, further strengthens balance sheet flexibility. This stable funding base enables the company to effectively manage interest rate cycles and expand its loan book while maintaining favorable net interest margins.

The Company has demonstrated the ability to enhance net interest income through the repricing of assets and optimization of funding costs, leading to margin expansion. With the Federal Reserve easing rates and yield curves stabilizing, funding costs are expected to remain favorable while loan yields continue to adjust, supporting further margin improvement. Additionally, proactive portfolio management and investment in higher-yielding securities enhance income generation.

Strategic partnerships and business development initiatives further strengthen growth prospects. The alliance with Federated Hermes expands access to institutional-grade investment products and research, enhancing the company’s wealth management capabilities and client value proposition. Similarly, the expanded partnership with SB Value Partners focuses on efficiency optimization and scaling the wealth business, which is expected to drive long-term value creation and improved returns. These collaborations not only deepen product offerings but also support geographic and customer expansion, reinforcing competitive positioning in regional markets.

Challenges Persist for ASRV’s Business

The company faces several headwinds, including elevated credit risk from its sizable exposure to commercial real estate loans, which are more sensitive to economic downturns, tenant occupancy, and borrower cash flows, potentially leading to higher delinquencies and charge-offs. The firm operates in a highly competitive landscape with larger banks, fintechs, and non-bank financial institutions offering superior resources and fewer regulatory constraints, intensifying pricing pressure. Additionally, regulatory scrutiny — particularly around commercial real estate concentrations — may increase compliance costs and limit growth.

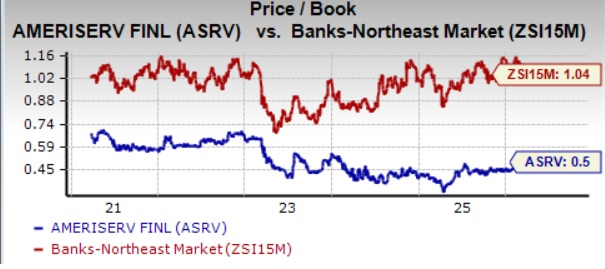

AmeriServ Financial’s Valuation

The company is cheaply priced compared with the industry average. Currently, ASRV is trading at 0.5X trailing 12-month price/book value, below the industry’s average of 1.04X. The metric also remains lower than that of the company’s peers, Atlantic UnionAUB-- Bankshares (1.01X) and Merchants Bancorp (1.14X).

Image Source: Zacks Investment Research

Conclusion

Despite challenges from elevated commercial real estate exposure, competitive pressures, and regulatory constraints, AmeriServ Financial remains supported by its diversified revenue mix, stable deposit base and expanding wealth management platform, which collectively strengthen earnings resilience and long-term growth potential.

Strong fundamentals, coupled with ASRV’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolio.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Merchants Bancorp (MBIN): Free Stock Analysis Report

AmeriServ Financial Inc. (ASRV): Free Stock Analysis Report

Atlantic Union Bankshares Corporation (AUB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet