American Express Q1 Earnings Beat Reflects Solid Spending by Premium Consumers, But Growth Momentum Eases

American Express posted stronger-than-expected first-quarter earnings, driven by sustained spending from its affluent customer base. However, softer network volume growth and sequential declines in airline billing suggest that while the premium consumer remains healthy, momentum is beginning to moderate. The company reaffirmed full-year guidance, but shares swung from gains to losses in pre-market trading as investors digested slowing volume trends and modest caution in management’s tone.

Results vs. Expectations

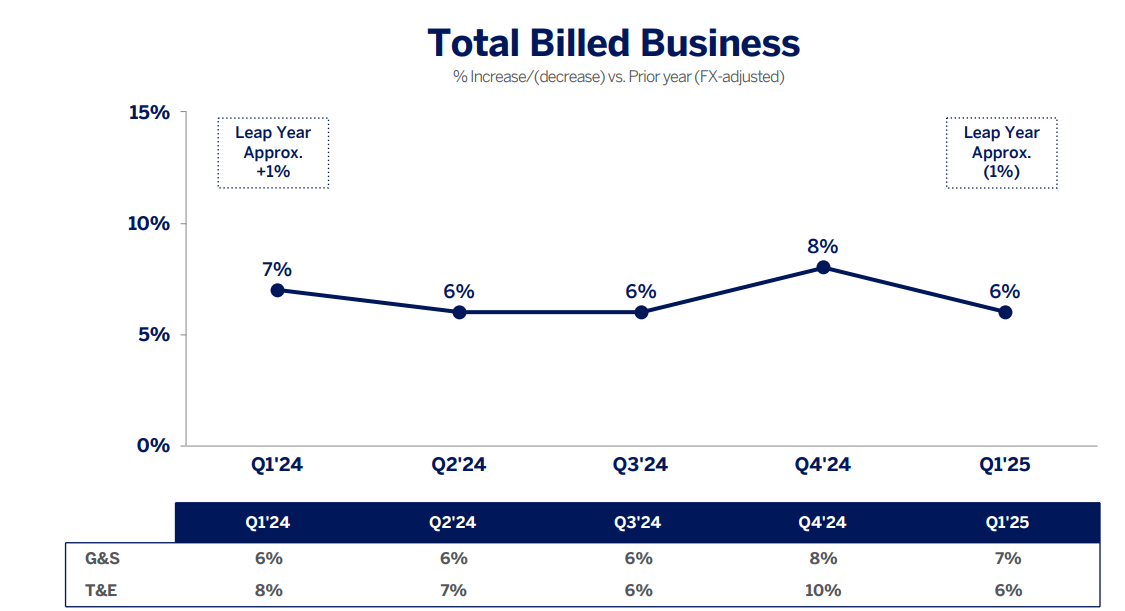

For the first quarter, Amex reported earnings per share of $3.64, beating the consensus estimate of $3.47. Revenue net of interest expense came in at $16.97 billion, just ahead of the $16.94 billion expectation. Net income rose 6% year-over-year to $2.58 billion. Total network volume of $439.6 billion was shy of the $443.3 billion analyst forecast and down sequentially from $464 billion in Q4. Billed business rose 6% year-over-year, but that was a deceleration from 8% growth in the prior quarter.

Source: American Express

Notably, the company maintained its full-year guidance for revenue growth of 8%-10% and EPS of $15.00-$15.50. The reaffirmation suggests management remains confident despite rising concerns over consumer softening in other parts of the economy.

Read-Through for Consumers

CEO Stephen Squeri noted that consumer spending trends were “consistent with and in many cases better than 2024,” with no deterioration observed in the early weeks of April. Still, airline billing—a bellwether of discretionary spending—showed a sequential slowdown. This may hint at increased consumer selectivity or fatigue in travel-related spending, a dynamic worth monitoring for companies like DeltaDAL--, United, American, and Southwest.

Overall cardmember spending was up 6% year-over-year, signaling resilience among high-end consumers, even as broader macro conditions remain mixed. That spending strength helped offset some investor concerns around the slight miss in network volume and the decline from Q4’s levels.

Segment and Revenue Drivers

Net card fee revenue increased to $2.33 billion, up from $2.25 billion in Q4 and $1.97 billion a year ago, underscoring strong demand for premium products. Net interest income also rose to $4.17 billion, topping the $4.10 billion consensus, driven by growth in revolving loan balances.

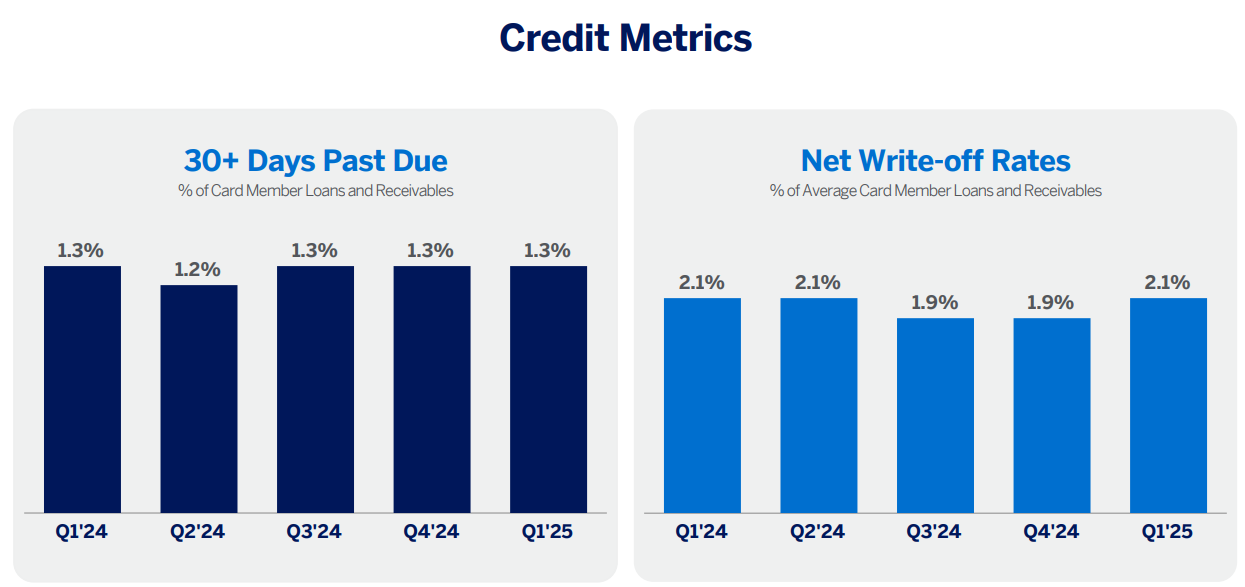

Provision for credit losses fell to $1.15 billion, better than expectations of $1.38 billion. The improvement was helped by a modest net reserve release and a stable net write-off rate of 2.1%. Credit quality remained solid across the portfolio, with management citing no red flags in cardmember performance.

Source: American Express

The company added 3.4 million new cards during the quarter, matching year-ago levels and ahead of Q4’s 3.0 million, suggesting that customer acquisition remains strong despite elevated interest rates and cautious consumer sentiment elsewhere in the economy.

Expense Management and Margin Trends

Total expenses rose 10% year-over-year to $12.5 billion, slightly above consensus. The increase was attributed to higher variable customer engagement costs, increased use of travel-related benefits, and a reversal of a favorable Membership Rewards accounting change seen in the prior year. Marketing spend held flat year-over-year, while operating expenses rose modestly.

The effective tax rate was 22.4%, roughly unchanged from the prior year, and the operating margin was steady despite the uptick in expenses.

Guidance and Market Reaction

Despite beating on the top and bottom lines, AXP shares reversed early gains to fall 1.3% in the premarket. Shares had been down 15% year-to-date entering the report, underperforming broader indices. The stock reaction reflects investor sensitivity to decelerating billing growth, especially within travel, even as guidance was maintained.

Management reiterated that guidance is “subject to the macroeconomic environment,” leaving room for adjustments should credit performance or consumer behavior weaken later in the year. The company continues to target its long-term earnings growth rate of 13%-15%.

Conclusion

Amex’s Q1 report affirms the relative strength of the premium consumer but also introduces hints of caution—particularly around travel-related activity. While the firm’s ability to maintain guidance is encouraging, the modest decline in network volume and airline billings growth suggests a more nuanced consumer environment in Q2 and beyond. With investors still rotating between growth and value, Amex remains a key barometer of upper-income discretionary trends, and its performance will have broader implications for consumer-facing sectors and the credit cycle.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet