AMD Q2 Earnings: Strong Revenue and AI Momentum Overshadowed by China Headwinds

WATCH: Uranium, and Real Assets Could Be the Only Safe Havens as Easy Money Ends

Advanced Micro Devices (AMD) reported mixed second-quarter results that, while showcasing solid top-line growth and AI traction, ultimately led to a sell-off as investors focused on regulatory headwinds and margin pressures. Shares fell roughly 6% post-report, testing support near the 20-day moving average as markets reacted to weaker-than-expected profitability metrics, export control fallout, and a lack of immediate upside from AI-related momentum.

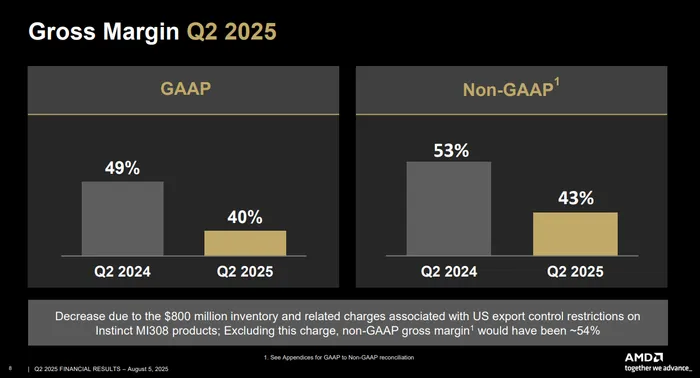

The headline numbers were a mixed bag. Revenue came in at $7.69 billion, beating consensus of $7.42 billion and marking a 32% year-over-year increase. But adjusted EPS of $0.48 narrowly missed the $0.49 consensus, with the shortfall driven largely by margin compression tied to a steep $800 million inventory charge related to U.S. government restrictions on AI GPU exports to China. That charge also weighed on reported operating income, which came in at a loss of $134 million on a GAAP basis. Stripping out those charges, AMD’s adjusted gross margin landed at 43%, slightly down from prior quarters, while GAAP gross margin slumped to 40%.

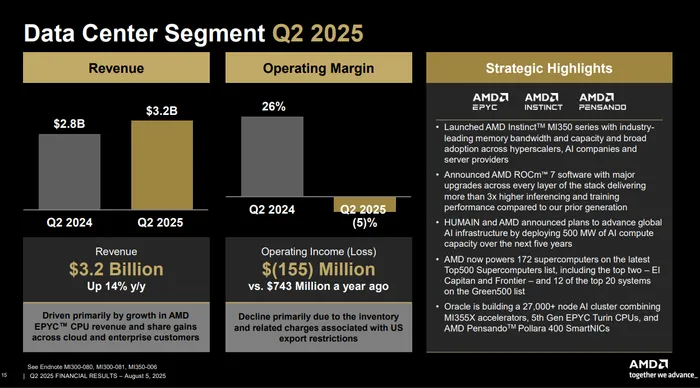

Data center performance, long a linchpin of AMD’s bull thesis, was a source of confusion. At a glance, revenue from the segment rose 14% year-over-year to $3.2 billion, driven by robust EPYC server CPU demand. However, that figure was down 12% sequentially due to weak MI308 GPU shipments—directly tied to export controls. AMD’s management acknowledged the difficulty in forecasting GPU shipments to China due to pending U.S. licensing approvals, prompting analysts to question the reliability of AI growth forecasts in the near term.

Still, not all was gloomy. CEO Lisa Su noted that EPYC server CPU sales hit record levels, and demand remained broad-based across both cloud and enterprise clients. More than 100 new AMD-powered cloud instances launched during the quarter. Su also confirmed that production of the MI350 AI accelerator began ahead of schedule and is ramping rapidly, with strong demand from hyperscalers and sovereign AI initiatives. The company is on track to ship $7 billion worth of MI3xx GPUs this year, excluding any China-related revenue—a notable revision upward from previous $6.5 billion forecasts.

Looking ahead, AMDAMD-- guided Q3 revenue to $8.7 billion (plus or minus $300 million), comfortably ahead of consensus estimates of $8.298 billion. Gross margin is expected to rebound to 54%, reflecting a healthier mix as high-margin products ramp and inventory charges fade. The company noted that the Q3 guide excludes any contribution from China-bound MI308 shipments, a sign that regulatory uncertainty will remain a risk factor.

The Client and Gaming segments were bright spots. Revenue jumped to $3.6 billion, up 69% year-over-year, as Ryzen desktop and mobile processor demand surged. ASPs were strong, and Su highlighted meaningful share gains across desktop, mobile, and commercial end-markets. The Embedded segment, by contrast, saw a modest 4% year-over-year decline to $824 million, though management pointed to early signs of cyclical recovery.

Export controls remain a notable overhang. The $800 million inventory write-down underscores the risk posed by regulatory volatility, and the exclusion of China revenue from guidance reflects management's caution. AMD is waiting for licensing approvals, with no clear timeline. As Su put it, “This is a better position than we were 90 days ago,” but visibility remains limited. The inability to monetize China-bound GPUs could hamper near-term upside in the Data Center segment, despite strong non-China demand.

Beyond the quarter, AMD continues to emphasize strategic investments in open AI ecosystems. The ROCm 7 platform—seen as an alternative to Nvidia’s CUDA—continues to gain traction with hyperscalers like MicrosoftMSFT-- and MetaMETA--. The MI350 GPU, paired with AMD’s Infinity architecture, delivers 3x the inferencing and training performance of prior generations, while the upcoming MI400 remains on track for a 2026 launch.

Despite the regulatory headwinds, analysts remain constructive on AMD’s long-term positioning. The company is gaining share in server CPUs, its MI series is beginning to scale, and recent moves—like the $3 billion sale of its ZT Systems manufacturing business—signal a disciplined shift toward high-margin core operations. Partnerships with TSMCTSM-- remain a key advantage as AMD continues to secure capacity and innovate on advanced packaging.

Still, sentiment has clearly cooled. At 44x forward earnings, valuation leaves little room for error, and investors are scrutinizing every line item for signs of AI monetization catching up with expectations. The reaction to this quarter—strong revenue, weak EPS, and heavy China risk discounting—underscores how high the bar has become.

In summary, AMD delivered a fundamentally solid Q2 marked by revenue strength, a robust product roadmap, and growing AI relevance. But the drag from export controls and questions around short-term profitability created enough doubt to trigger a selloff. With MI350 production accelerating and MI400 in the pipeline, AMD remains one of the most important challengers to Nvidia’s dominance. But with geopolitical friction rising and valuation rich, the company is now entering a phase where execution—and regulatory clarity—will be as important as innovation.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet