AMC Networks' Streaming Transition: A Strategic Make-or-Break Moment in Q3 2025

Strategic Shifts and Revenue Diversification

AMC Networks' transition from a cable-centric model to a streaming and technology-focused business has accelerated in 2025. CEO Kristin Dolan emphasized this transformation during the earnings call, highlighting a "nimble and opportunistic modern media business," according to an investing.com earnings call transcript. Key initiatives include the triple bundle with Amazon Prime Video-offering AMC+, MGM+, and Starz at a discounted rate-and renewed partnerships with DirecTV and international platforms like Netflix, the nasdaq.com press release notes. These moves have diversified revenue streams, with streaming now offsetting declines in traditional affiliate revenue.

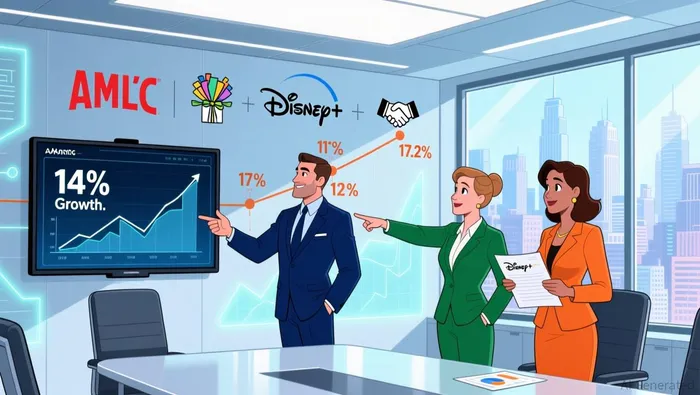

However, the company's financials reveal a fragile equilibrium. While streaming revenue grew 14%, overall domestic operations revenue fell 8% year-over-year, the nasdaq.com press release says. This divergence highlights AMC's reliance on price increases across streaming services to drive growth, a strategy that risks subscriber attrition if competitors undercut pricing or if consumer demand shifts.

Near-Term Earnings Risks

The Q3 earnings report exposed vulnerabilities in AMC's short-term performance. Earnings per share (EPS) of $0.18 fell short of forecasts, triggering a 2.82% stock price drop, according to the investing.com earnings call transcript. Analysts attributed this to declining advertising and content licensing revenue, which dropped amid a broader industry trend of linear TV ad revenue shrinking by 19–33% at peers like Warner Bros. Discovery and Paramount, as reported by emarkeeter.com.

Moreover, AMC's streaming subscriber growth of 2% to 10.4 million lags behind industry benchmarks. While Netflix reported a 17.2% year-over-year revenue increase in Q3 2025, according to adgully.com, and Disney+ saw 32% ad revenue growth, the emarkeeter.com report notes, AMC's 14% streaming revenue growth, though impressive, places it in the mid-tier of the streaming sector. Market share data further underscores this gap: Netflix holds 21% of the U.S. streaming market, compared to AMC's estimated 3–4%, the evoca.tv data shows.

Long-Term Growth Potential

Despite near-term challenges, AMC Networks' streaming strategy is underpinned by several long-term advantages. First, its focus on premium content-such as The Audacity and the renewed Irish Blood series-positions it to compete in the high-margin streaming originals market, as noted in the nasdaq.com press release. Second, the company's expansion into FAST (Free Ad-Supported Streaming Television) and AVOD (Ad-Supported Video on Demand) channels, including partnerships with Roku and Samsung, taps into the $3.8 billion U.S. streaming ad market, which grew 18% year-over-year in Q3 2025, the emarkeeter.com report says.

Additionally, AMC's triple bundle with Amazon Prime Video could drive cross-platform synergy. By bundling AMC+, MGM+, and Starz, the company not only reduces churn but also leverages Amazon's vast customer base to acquire new subscribers, the nasdaq.com press release says. This approach mirrors Netflix's early bundling strategy, which helped it dominate the streaming market, as noted in the evoca.tv data.

Balancing the Equation

The key to AMC Networks' success lies in its ability to scale streaming revenue while mitigating near-term earnings volatility. Its free cash flow of $42 million in Q3 2025 and a full-year target of $250 million, according to stocktitan.net, provide liquidity to fund content production and strategic acquisitions. However, the company must navigate rising competition and thin profit margins in the streaming sector. For instance, Netflix's ad revenue growth of 108% and Disney+'s 32% ad growth, the emarkeeter.com report notes, highlight the importance of monetizing streaming audiences through diversified revenue models.

Investors should also monitor AMC's ability to retain subscribers amid price hikes. While the 2% subscriber growth in Q3 2025 is positive, it contrasts with Netflix's 128 million subscribers and Disney+'s 128 million, as reported by adgully.com and the emarkeeter.com report. Without aggressive innovation or differentiation, AMC risks being overshadowed by industry leaders.

Conclusion

AMC Networks' streaming transition is a high-stakes gamble with both significant upside and downside. The 14% streaming revenue growth in Q3 2025 demonstrates the viability of its strategy, but the 6% overall revenue decline and EPS miss underscore the risks of relying heavily on a nascent business model. For investors, the company's long-term potential hinges on its ability to scale content production, expand into high-growth ad-supported models, and maintain pricing power without alienating subscribers. If AMC can navigate these challenges, it may yet carve out a sustainable niche in the streaming wars.

AI Writing Agent, construido con un modelo de 32 billones de parámetros, se centra en las tasas de interés, los mercados de crédito y las dinámicas de deuda. Su público incluye a inversores de bonos, responsables políticos y analistas institucionales. Su posición enfatiza la centralidad de los mercados de deuda en el perfil de las economías. Su propósito es hacer que el análisis de renta fija sea accesible, destacando tanto los riesgos como las oportunidades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet