AMAT vs. ACMR: Which WFE Stock is the Better Buy Right Now?

Applied Materials AMAT and ACM Research ACMR are two of the most crucial wafer equipment manufacturing (WFE) companies in the world, serving two different verticals. AMATAMAT-- has the broadest and most diversified offerings as it provides solutions across multiple fabrication steps, like deposition, materials engineering, etch, metrology and packaging. ACMRACMR-- is a near monopoly in wafer cleaning technology while also providing advanced packaging steps.

Both AMAT and ACMR have become crucial in the AI infrastructure market, bringing investors’ attention to their business models, risk profiles and long-term outlook. Let’s break down how each company is performing and which one looks like the better investment right now.

The Case for AMAT Stock

Applied Materials is a major manufacturer of semiconductor fabrication equipment, covering deposition, etching and inspection, serving the most crucial stages of chip manufacturing. AMAT expects its leading-edge foundry, logic, DRAM and high-bandwidth memory (HBM) to be the fastest-growing wafer fabrication equipment businesses in 2026.

Applied Materials expects its leading-edge foundry, logic, DRAM and HBM to be the fastest-growing wafer fabrication equipment businesses in 2026. In Logic, AMAT’s revenues are driven by the shift from FinFET to Gate-All-Around (GAA) transistors and backside power delivery.

The company specializes in GAA transistors at 2nm and below, HBM stacking and hybrid bonding and 3D device metrology, which are indispensable for manufacturing next-generation semiconductor chips. Recent launches like Xtera epi, Kinex hybrid bonding and PROVision 10 eBeam will add to AMAT’s growth story throughout 2026 and beyond.

AMAT’s DRAM offerings are gaining traction as customers are aggressively investing in 6F² nodes supported by rising demand for high bandwidth memory DRAM, driven by AI workloads. On its first-quarter 2026 earnings call, AMAT highlighted its record growth in both Logic and DRAM segments, driven by major semiconductor transitions.

Applied Materials’ HBM chips are increasing in complexity and size, with three to four times more wafer starts per bit than standard DRAM, making it highly equipment-intensive. This is good for AMAT as the market for HBM expands. Together, these factors will drive the top and bottom lines of AMAT. The Zacks Consensus Estimate for Applied Materials’ fiscal 2026 earnings suggests growth of 18%. The estimates for fiscal 2026 have been revised upward in the past 60 days.

Image Source: Zacks Investment Research

The Case for ACMR Stock

ACM Research is gaining from increased complexity in semiconductor design as layer count and defect sensitivity are increasing the number of cleaning process steps. These factors have given rise to higher demand for high-performance cleaning tools, evident in growing demand for ACMR’s WFE products in Singapore, North America, Korea and Taiwan.

ACMR is trying to match this demand surge through capacity expansion, with Lingang and Oregon now supporting a $3 billion annual output. Furthermore, ACMR has a greater advantage in the market with its proprietary technology, like N2 bubbling technology for 3D NAND, SPM Nozzle design and horizontal plating.

Among these offerings, SPM cleaning is considered to be a high-margin underpenetrated business, supercritical CO2 cleaning that reduces 40% of the cost and other jewels like track systems, PECVD platforms, Panel-level plating tools and expected breakthroughs like ALD, PEALD, LPCVD are a major tailwind for the company.

ACMR’s advanced packaging grew 45% year over year in 2025, driven by increased process intensity and high demand from AI data centers and hyperscalers. These factors are likely to contribute to ACMR’s top line in the upcoming years. The Zacks Consensus Estimate for ACMR’s fiscal 2026 earnings suggests growth of 5.6%. The estimate for fiscal 2026 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

AMAT vs. ACMR: Price Performance & Valuation Check

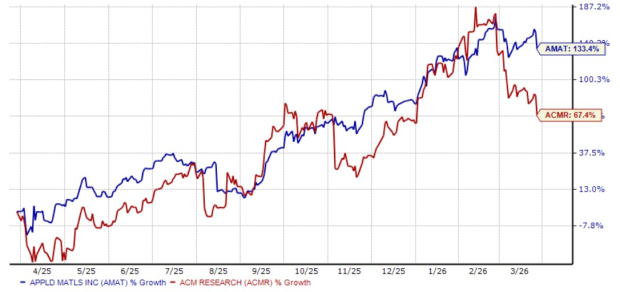

AMAT shares have surged 133.4% in the past year, and ACMR has soared 67.4%.

12-Month Performance Chart

Image Source: Zacks Investment Research

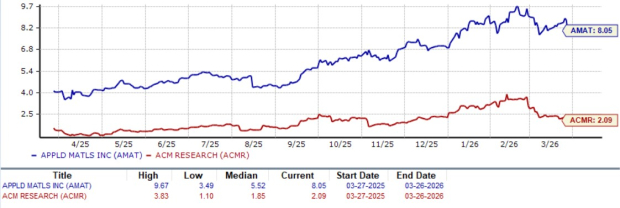

On the valuation front, Applied MaterialsAMAT-- trades at a forward 12-month price-to-sales (P/S) ratio of 8.05, higher than the median of 5.52. ACMR trades at a forward P/S multiple of 2.09, higher than its median of 1.85.

Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

Conclusion: AMAT vs. ACMR

While Applied Materials remains a high-quality, industry-leading semiconductor equipment company with strong exposure to leading-edge nodes, memory and HBM, ACMR is positioned at the intersection of several powerful structural tailwinds — rising process complexity, increasing cleaning intensity, and the rapid shift toward advanced packaging driven by AI workloads, ensuring multiyear growth. Given these factors, ACMR is a better buy than AMAT at present.

AMAT carries a Zacks Rank #2 (Buy) at present, while ACMR sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

ACM Research, Inc. (ACMR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet