Aluminum Prices Could Surge 50%: Citi’s Bullish Call

Electric vehicles, AI data centers, even humanoid robots — all need aluminum. With supply capped, could prices be on the verge of a historic breakout?

WATCH: Former OpenAI Exec: The SHOCKING Truth About AI

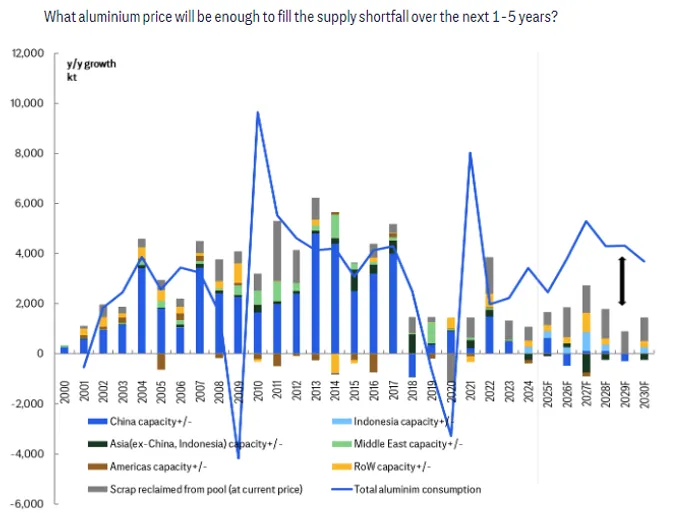

The global aluminum market is heading toward its most severe supply shortfall in more than two decades. If prices remain at current levels, a crisis of inventory depletion may become unavoidable.

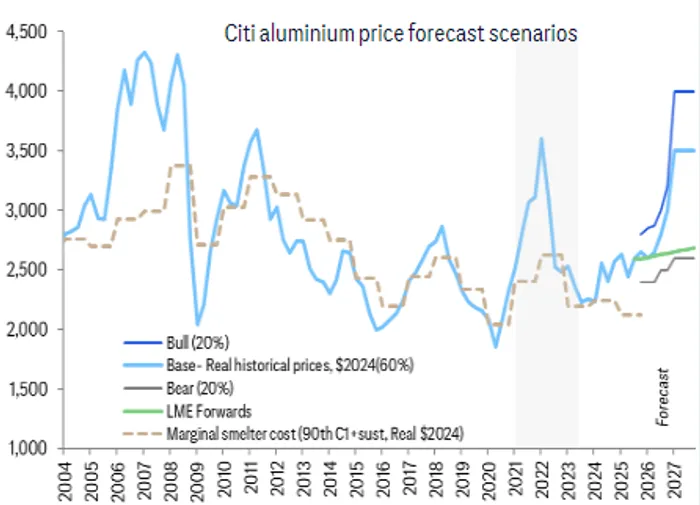

Citi analysts Wenyu Yao, Maximilian Layton, and Shreyas Madabushi wrote in a September 15 report that they are structurally bullish on aluminum. At the current price of $2,500 per ton, the market could face an unsustainable deficit over the next five years. They estimate aluminum prices need to rise above $3,000 per ton to incentivize the necessary supply growth.

In the medium to long term, CitiC-- forecasts aluminum could even test the “demand destruction” threshold of $4,000 per ton—suggesting potential upside of 50–60%.

Shrinking Supply, Surging Demand

The past two decades of low aluminum prices and oversupply were driven mainly by China’s rapid expansion of low-cost capacity. That era is now over. China’s idle capacity has been fully absorbed, and production growth has stalled.

Meanwhile, demand prospects appear exceptionally strong. According to the World Economic Forum, demand for aluminum will grow 40% by 2030. Beyond structural demand from electric vehicles, solar, wind, and grid upgrades, a wave of “future industries” is emerging as powerful growth drivers. Each humanoid robot, for example, requires 20–25 kilograms of aluminum.

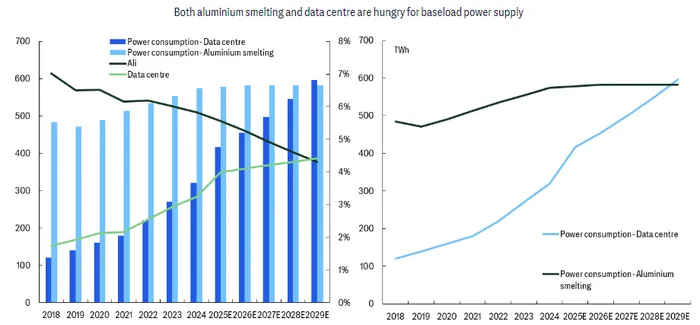

The report also highlighted that in Q1 2025, Chinese listed companies’ data center capex doubled year-on-year, and by July industrial robot production surged 60% year-on-year to an annualized pace of 900,000 units. These sectors not only consume large amounts of aluminum but also demand massive electricity, straining power supply for aluminum smelters and lowering operating rates.

Citi believes China’s huge investments in robotics and AI could replicate its earlier patterns in the energy transition and the U.S. shale boom—where massive capital inflows drove down costs and triggered explosive supply growth. This would provide long-term, robust demand for upstream materials such as aluminum, copper, lithium, and power.

Indonesia’s Supply Challenges

With China’s capacity capped, Indonesia is emerging as the next major aluminum producer. Under Citi’s base case, Indonesia’s aluminum capacity could reach 2.3 million tons by 2029. But this expansion relies heavily on coal-fired captive power plants, facing ESG, regulatory, and financing risks.

These integrated projects have payback periods of 8–11 years, even under an optimistic $2,800 per ton price assumption. A more aggressive target of 4.45 million tons would consume more than 14% of Indonesia’s total national electricity output, raising feasibility concerns.

Meanwhile, recycled aluminum cannot fully fill the gap. Historically, scrap recovery rates rise only with strong price incentives. Without sustained price pressure, Citi expects recovery rates to rise modestly from 45% today to 50% in the coming years, helped by AI sorting technology. But this will be far from sufficient to balance the market.

Aluminum scrap also responds less effectively to price signals than copper scrap, meaning the market cannot rely on recycled aluminum to quickly offset shortages.

Higher Prices Needed to Balance Market

Considering both supply and demand, Citi concludes current aluminum prices are unsustainable. To incentivize more than 10 million tons of new supply needed by 2030, prices must remain well above current levels.

Specifically, Citi projects prices must sustainably stay above $3,000 per ton to provide adequate returns for projects in Indonesia and elsewhere.

If supply growth and scrap recovery still fall short, prices will need to rise even further to suppress demand. In that case, aluminum may need to trade near $4,000 per ton—similar to the levels required to balance the market in the early 2000s.

For investors, this represents a fundamental structural shift in the aluminum market. Low inventories, inelastic supply, and strong emerging demand together create a bullish long-term setup.

How to Invest?

Several companies specialize in aluminum production or in using it to manufacture higher-value products. Key players include AlcoaAA-- (AA), Kaiser AluminumKALU-- (KALU), Century AluminumCENX-- (CENX), and Rio TintoRIO-- Group (RIO).

Alcoa is a fully integrated aluminum producer and one of the world’s largest bauxite miners. It owns stakes in seven high-quality, low-cost bauxite mines across Australia, Brazil, Guinea, and Saudi Arabia.

Kaiser Aluminum is a leading semi-fabricated aluminum producer with 13 manufacturing facilities in North America. As of mid-2025, it offered a 4% dividend yield—far above the S&P 500 average of less than 1.5%.

Century Aluminum operates three smelters in the U.S. and one in Iceland. Following U.S. aluminum import tariffs under the Trump administration, it restarted idled capacity at its Mt. Holly facility, boosting U.S. aluminum output by 10%.

Rio Tinto is a diversified mining giant headquartered in London. It operates four bauxite mines, four refineries, and 14 aluminum smelters. While aluminum accounts for 13% of its revenue, iron ore makes up over 70%. Its diversification provides resilience, as demand for iron ore and copper is expected to accelerate amid decarbonization.

For those wary of single-stock risk, ETFs provide exposure:

iShares U.S. Basic Materials ETF (IYM) offers indirect exposure through holdings such as Alcoa and Newmont MiningNEM--.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO