Alphabet Smashes $100B Quarter: AI Boom Ignites Record Results and $90B Spending Spree

Alphabet capped its strongest quarter in company history Wednesday, smashing Wall Street expectations on both the top and bottom line while signaling unrelenting AI investment ahead. Revenue surged 16% year over year to $102.35 billion, its first-ever $100 billion quarter, and earnings per share jumped to $2.87, handily topping the $2.26 consensus. Every major segment—Search, YouTube, and Cloud—delivered double-digit growth, underscoring Alphabet’s leadership in digital advertising and artificial intelligence. Yet while the stock initially spiked as much as 9% to $297 in after-hours trading, it later eased back toward $287 as investors digested a sharply higher CapEx forecast that signaled another costly leg in the AI arms race.

The headline numbers were unequivocal beats. Revenue of $102.35 billion exceeded estimates of $100.14 billion, while net income rose 33% to $34.98 billion. Ex-TAC (traffic acquisition costs), revenue stood at $87.47 billion, also ahead of expectations. Operating income climbed to $31.23 billion, and the operating margin reached 31%, or 33.9% excluding a $3.5 billion European Commission fine. Alphabet declared a quarterly dividend of $0.21 per share—its third consecutive payout since initiating a dividend earlier this year—reinforcing its position as one of the few tech giants combining growth with shareholder returns.

Advertising, Alphabet’s profit engine, powered much of the upside. Google advertising revenue jumped 13% year over year to $74.18 billion, with Search contributing $56.57 billion and YouTube Ads delivering $10.26 billion. The latter marked a 15% jump from a year ago, buoyed by improving monetization from Shorts and sustained engagement in long-form content. YouTube’s growing share of connected TV viewership—now 12.6% of all U.S. TV watching—continues to attract premium advertisers. Alphabet noted that click-through rates and paid clicks both increased, signaling stronger ad engagement even amid higher pricing. Analysts viewed the combination of higher ad volume and pricing power as evidence that Google’s AI-driven targeting tools are resonating with marketers, keeping Alphabet well ahead of rivals in digital advertising share.

Beyond ads, YouTube Premium and GoogleGOOGL-- One subscriptions fueled a 21% rise in subscription revenue to $12.87 billion, bringing total paid subscriptions to over 300 million. That steady base of recurring revenue adds resilience to Alphabet’s broader ecosystem as the company shifts toward AI-driven services. CEO Sundar Pichai noted, “Our full-stack approach to AI is delivering strong momentum and we’re shipping at speed,” pointing to Gemini’s rapid adoption—now over 650 million monthly active users—and its ability to process “7 billion tokens per minute” through APIs.

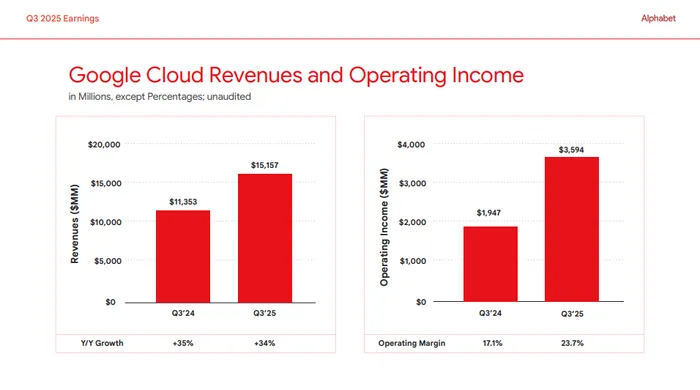

Cloud was another standout. Google Cloud revenue soared 34% year over year to $15.16 billion, beating the Street’s $14.75 billion forecast and widening the unit’s profitability. Operating income in the segment rose to $3.6 billion from $1.9 billion a year earlier, underscoring margin scalability as enterprise demand for AI infrastructure accelerates. The backlog climbed to a record $155 billion, signaling multi-year visibility for Google Cloud Platform’s AI and data services. Analysts noted the division continues to close the gap with Microsoft Azure and Amazon Web Services, especially in generative AI workloads, where Google’s custom silicon—like the new 3nm Ironwood TPUs—offers cost and performance advantages.

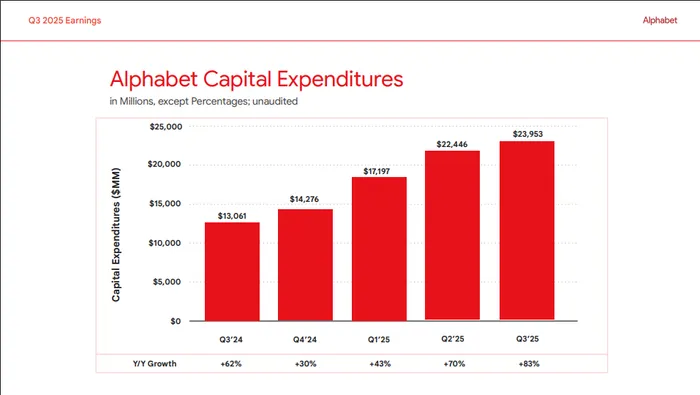

Still, the magnitude of Alphabet’s spending drew investor focus. The company raised its full-year capital expenditure outlook to $91–93 billion, up sharply from prior guidance of about $85 billion and nearly double 2024’s $52.5 billion. Management attributed the increase to data center construction and AI infrastructure scaling. CFO Ruth Porat said spending would remain “elevated into 2026” as demand for AI compute outstrips existing capacity. The figure underscores the high-stakes nature of the AI race, where hyperscalers are building massive server and power footprints to meet enterprise and consumer AI demand.

For context, Microsoft’s current CapEx run rate hovers around $31 billion per quarter, while Meta is on pace for roughly $70 billion in 2025. Alphabet’s revised $90 billion-plus range now places it firmly in the same spending league—an unmistakable signal that Google intends to defend and expand its leadership in AI infrastructure, search integration, and model deployment. Analysts generally viewed the ramp as positive for long-term positioning, though it explains some of the profit-taking following the post-earnings pop.

Operationally, Alphabet’s efficiency remains a bright spot. Excluding the regulatory fine, operating margins improved more than 200 basis points year over year, even as headcount rose to 190,167 from 181,000 a year ago. AI tools are already boosting productivity inside the company, with Pichai highlighting internal Gemini deployments across code generation, ad optimization, and data management. Other income surged to $12.8 billion, largely from unrealized investment gains, adding to the quarter’s bottom-line strength.

From a strategic lens, the report validates Alphabet’s transition from a pure ad platform to an AI ecosystem company. Search revenue continues to grow double digits despite saturation, YouTube has become the leading digital video channel globally, and Cloud is now solidly profitable. Meanwhile, the company avoided harsher antitrust remedies in the U.S. last month—what analysts called a “clearing event” that lets investors refocus on fundamentals.

In short, Alphabet’s quarter delivered exactly what Wall Street wanted: broad-based growth, expanding margins, and a confident AI investment roadmap. Yet it also revived the classic tension between growth and capital intensity. The after-hours fade—from $297 down to $287—suggests some profit-taking as investors weigh near-term cash burn against long-term dominance.

Still, the narrative remains intact. With ad momentum strong, Cloud scaling profitably, and Gemini accelerating user adoption, Alphabet’s Q3 reinforced its position as the indispensable backbone of the AI economy. As Pichai put it succinctly, “We delivered our first-ever $100 billion quarter.” Investors now have little doubt that Google’s AI machine is fully operational—and still gaining speed.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet