Alphabet Q1 Earnings Review: Strong Beat on EPS, Resilient Ad Revenue, and Cloud Momentum Offset Macro Uncertainty

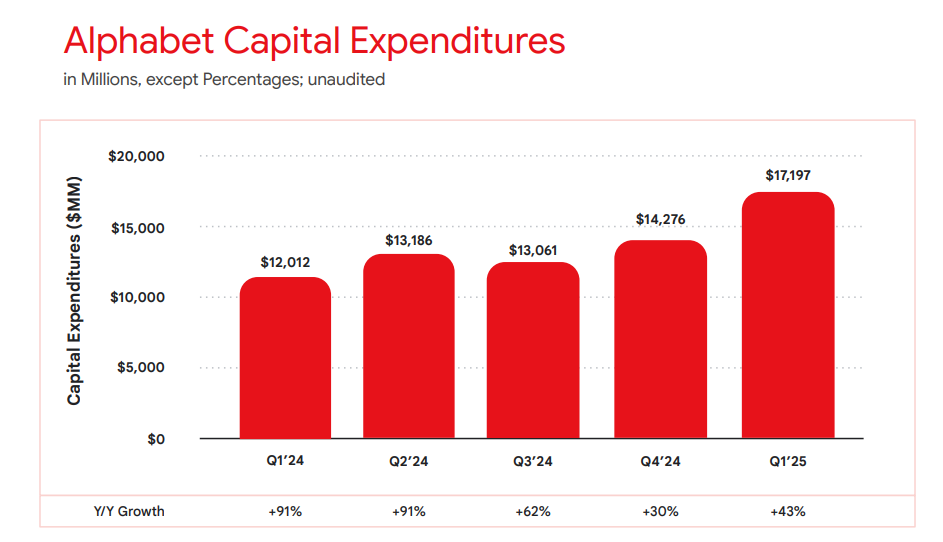

Alphabet kicked off earnings season for the mega-cap tech cohort with a confident strideLRN--, delivering better-than-expected results across key performance metrics and boosting shareholder returns. In the face of macroeconomic uncertainty and regulatory scrutiny, the GoogleGOOG-- parent posted adjusted earnings per share (EPS) of $2.81—well ahead of the $2.01 consensus and up nearly 49% year over year. Revenue for the quarter landed at $90.23 billion, topping expectations of $89.1 billion and growing 12% annually. Capital Expenditures did shoot up 43% to $17 billion in the quarter. Investors will want to see if GOOGL reiterates its $75 billion CapEx target for 2025 on the call. Shares climbed over 4% in after-hours trading as the company’s ad business and cloud momentum provided reassurance to investors.

Advertising Resilience: Better Than Feared

Despite fears of digital advertising fatigue amid the renewed trade tensions and weaker e-commerce activity, Alphabet’s ad revenue came in at $66.89 billion, up 8.5% year over year and above the $66.39 billion consensus. Google Search revenue hit $50.7 billion, just beating expectations but down sequentially from Q4, suggesting investors will comb through the earnings call commentary for signs of softening demand and increased competition from ChatGpt and other AI programs. Notably, while YouTube ads revenue of $8.93 billion was up 10% annually, it slightly missed estimates of $8.94 billion—highlighting a possible plateau in platform monetization after previous strong quarters.

The company did not shy away from acknowledging external challenges. Recent commentary from analysts such as Barclays’ Ross Sandler warned of softer transaction volumes in digital retail, and Alphabet’s ad growth slowdown from Q4’s 10.6% clip to 8.5% in Q1 reflects that reality. However, surpassing Street expectations shows that ad budgets have not collapsed—yet. This will be a popular topic during Q&A.

Cloud Growth Continues, but Pace Moderates

Google Cloud revenue rose 28% year over year to $12.26 billion, just a hair below the $12.32 billion consensus. While the segment's growth decelerated from the prior quarter’s 30.1% pace, investors were encouraged by the operating income from Cloud, which reached $2.18 billion—more than double the $900 million in the prior-year period and well ahead of estimates.

Alphabet emphasized strength across its core Google Cloud Platform (GCP) offerings, including AI infrastructure and generative AI solutions. The rollout of Gemini 2.5, its new AI model, was credited with driving interest and enterprise engagement. Though not quite a blowout, the solid cloud margin progress marks a critical step toward sustained profitability in the fiercely competitive enterprise cloud space.

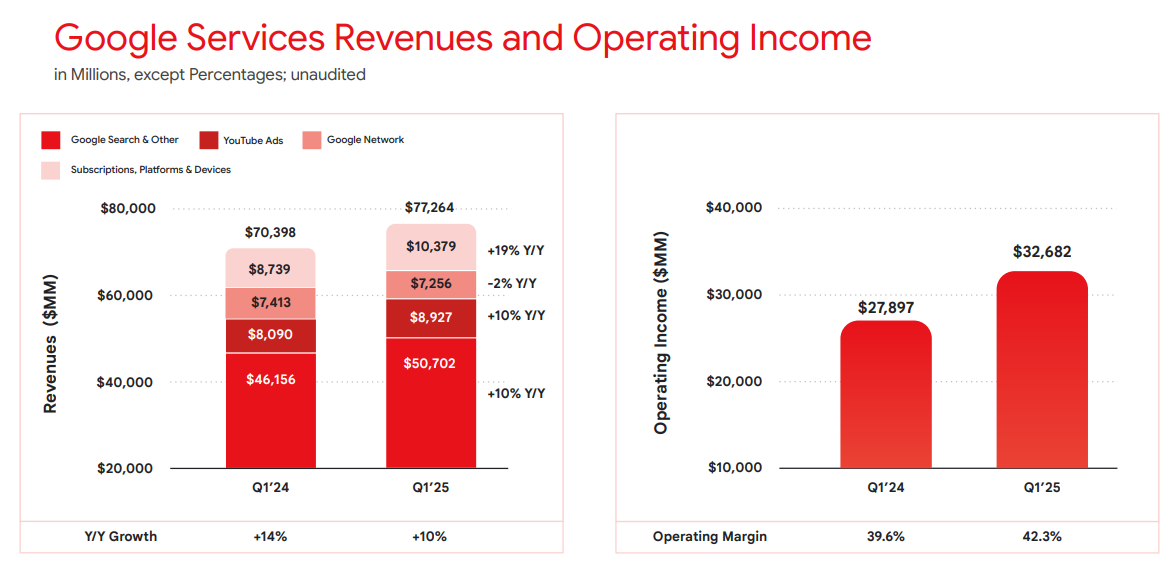

Services and Subscriptions: Growing User Base, Platform Depth

Total Google Services revenue increased nearly 10% to $77.26 billion, led by Search, YouTube, and a notable $10.38 billion in subscriptions, platforms, and devices revenue—a figure that beat estimates by nearly half a billion. The company now boasts over 270 million paid subscribers across services such as YouTube Premium and Google One, signaling that its consumer monetization efforts continue to pay off.

The segment's operating income was robust at $32.68 billion, reflecting a 17% increase year over year. With margin improvement and user growth tied to AI-enhanced services, AlphabetGOOG-- continues to leverage its ecosystem to scale engagement without inflating operating costs.

Other Bets and Ongoing Challenges

Alphabet’s "Other Bets" segment remains in deep red territory, posting a $1.23 billion operating loss, which widened from the prior year and missed expectations. Revenue fell 9.1% to $450 million, reflecting ongoing struggles to commercialize its moonshot projects. While this segment has never been a needle-mover on earnings day, investors remain cautious about the company’s ability to eventually turn these ventures into viable businesses.

The company also faces legal pressure. Alphabet recently suffered dual antitrust rulings, including a high-profile case involving alleged monopoly practices in the online ad space. These developments could weigh on long-term sentiment, particularly if divestiture or structural changes are imposed.

Capital Return and Shareholder Yield Expansion

Alphabet announced a major $70 billion stock repurchase authorization, in line with recent Big Tech trends to emphasize capital returns. The company also hiked its quarterly dividend by 5% to $0.21 per share, reinforcing confidence in long-term cash flow durability.

The capital return programs underscore Alphabet’s ability to sustain growth investments while rewarding shareholders—especially amid regulatory turbulence and political noise surrounding tech policy and tariffs.

Conclusion: AI Anchored Growth, Watch Ad Trends in Q2

Alphabet’s Q1 results were a firm reminder of its financial resilience and operational leverage, with strong beats on EPS and revenue, expanding margins, and accelerating cloud profits. While sequential ad deceleration and YouTube’s slight miss temper the narrative, they haven’t yet derailed investor confidence.

Looking ahead, second-quarter commentary on ad demand and macro risks will be critical. Any indications of weakening digital ad spend due to global trade pressures or economic slowdown could weigh on growth expectations. For now, however, Alphabet remains a bellwether of stability in the mega-cap tech space, with AI-led initiatives increasingly pulling the company’s long-term strategy into sharper focus.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet