Alibaba's Q3 Earnings Disappoint: Time to Hold or Fold the Stock?

Alibaba Group's BABA third-quarter fiscal 2026 results painted a troubling picture for investors hoping the Chinese tech giant's transformation story would finally deliver. The company missed on both top and bottom lines, with revenues of approximately $40.7 billion falling 1.95% short of the Zacks Consensus Estimate and non-GAAP diluted earnings of $1.01 per ADS missing estimates by a startling 47.12%. In domestic currency terms, revenues grew 2% year over year while net income collapsed 66%. Free cash flow fell by RMB 27.7 billion compared with the prior-year period — a scale of deterioration that is difficult to dismiss as a temporary investment-led blip and one that demands serious scrutiny from investors.

Margins Collapse Under the Weight of Ambition

The earnings shortfall was not due to revenue weakness alone. Adjusted EBITDA tumbled 57% year over year, a staggering decline management attributed to the company's aggressive push into Quick Commerce — Alibaba's on-demand delivery service — alongside elevated spending on user experience and technology. Quick Commerce's segment-adjusted EBITA fell 78% year over year, indicating the business is consuming capital at a pace that scale efficiencies have yet to offset.

Sales and marketing expenses expanded substantially in the quarter, underscoring the fierce competitive intensity of China's e-commerce landscape. Even as the Cloud Intelligence Group offered a rare bright spot — with revenues accelerating 36% and AI-related products delivering triple-digit growth for the 10th consecutive quarter — this performance alone cannot compensate for the broader profitability deterioration across the business.

Management's forward-looking ambition compounds the concern rather than alleviating it. During the earnings call, AlibabaBABA-- outlined a five-year goal to surpass $100 billion in combined cloud and AI external revenues, while signaling capital expenditure commitments exceeding $55 billion through fiscal 2028. These projections confirm that investment headwinds are far from receding. The company expects its Model-as-a-Service business to eventually become the Cloud Intelligence Group's largest revenue product, but meaningful monetization remains a future proposition rather than a present financial reality. Investors seeking near-term earnings recovery will find little comfort in guidance that defers profitability improvement to a distant horizon while sustaining heavy near-term spending.

Adding to concerns, the Zacks Consensus Estimate for fiscal 2026 earnings is pinned at $5.72 per share, implying a 36.51% year-over-year decline, underscoring the depth of the profitability challenge Alibaba faces as it continues to fund Quick Commerce expansion and AI infrastructure investment simultaneously.

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Mounting Risks Create Concern

Alibaba's fiscal 2026 outlook remains weighed down by structural headwinds with no clear inflection point. Quick Commerce continues to dilute profitability with no firm timeline for breakeven. The disposal of Sun Art and Intime has eroded revenue comparability, and while the company indicated that like-for-like revenue would have grown 9%, headline growth of just 2% year over year underscores the persistent challenge of sustaining top-line momentum.

Management has signaled that investments in consumption-related innovation will continue, implying ongoing margin compression. China's subdued macroeconomic backdrop — with the government targeting GDP growth at its lowest levels in decades — compounds the difficulty of reigniting core e-commerce volumes. With earnings misses, leadership instability, escalating capital commitments and deteriorating profitability converging at once, the case for staying on the sidelines in 2026 becomes compelling.

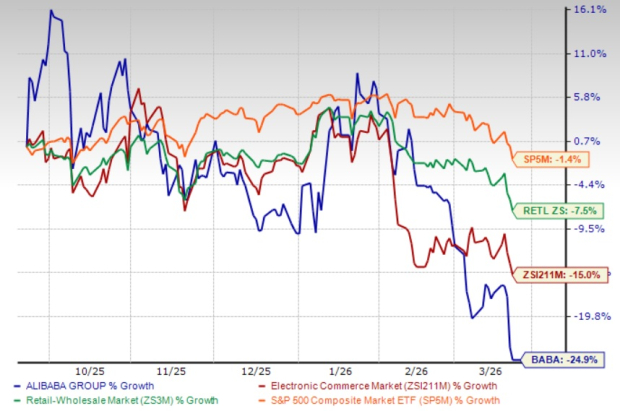

Lagging the Market and Losing Ground to Cloud Giants

BABA shares have lost 24.9% in the past six-month period, underperforming the Zacks Retail-Wholesale sector’s decline of 7.5% — a gap that reflects not merely broader market turbulence but investor-specific skepticism about Alibaba's near-term earnings trajectory. Rather than benefiting from the AI tailwind, BABABABA-- has been weighed down by its earnings misses, leadership instability and the market's growing impatience with a turnaround story that has yet to deliver convincing profitability improvement.

BABA’s 6-Month Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, BABA stock is currently trading at a trailing 12-month EV/EBITDA ratio of 15.98X compared with the Zacks Internet – Commerce industry’s 10.39X, suggesting the stock is not cheap despite its fundamental deterioration. BABA has a Value Score of C.

BABA’s Valuation

Image Source: Zacks Investment Research

On the competitive front, Alibaba's cloud aspirations face formidable opposition from Amazon AMZN, Microsoft MSFT and Alphabet GOOGL-owned Google — three of the world's most resourced hyperscalers. According to new data from Synergy Research Group, Amazon, Microsoft and Alphabet held fourth-quarter worldwide cloud market shares of 28%, 21% and 14%, respectively. Against these three adversaries, Alibaba must simultaneously defend its home turf — where domestic rivals Huawei Cloud and Tencent Cloud are mounting credible challenges — and press for international cloud expansion in markets where Amazon, Microsoft and Google already hold entrenched positions.

Conclusion

With BABA shares underperforming, valuation stretched relative to industry peers, earnings estimates in a sharp downward trajectory, and cloud competition intensifying from some of the world's best-capitalized technology firms, the risk-reward calculus for investors in 2026 tilts decidedly unfavorably. Until profitability stabilizes, investors are better served staying on the sidelines. Alibaba currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet