Ainvest Option Flow Digest - November 10, 2025

$333.5M Whale Trades: Nuclear Power, Gold, AI & Defense - Smart Money's 2026 Blueprint

Welcome to today's unusual options flow analysis. On November 10, 2025, we tracked $333.5 MILLION in institutional-scale options activity across 10 high-conviction positions. This isn't retail speculation—these are sophisticated players positioning for major catalysts spanning from December 2025 through January 2027.

Today's Total Flow: $333.5M across 10 tickers Largest Single Trade: GLD $96M Bull Call Spread Average Premium: $33.35M per ticker Timeframe Range: Weekly (Dec) to LEAPS (Jan 2027)

🎯 What's Happening: The One-Liner Breakdown

Mega-Cap Plays ($251M Combined)

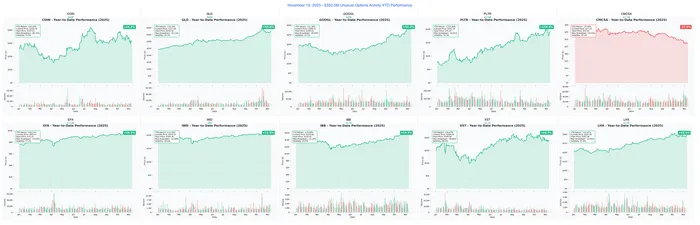

COIN $95M Diagonal Spread - Bullish crypto bet with January 2027 LEAPS as BitcoinBTC-- ETF flows surge and Coinbase One subscriptions hit records. Strategy expects consolidation near $300 before breakout above $350 by 2026.

GLD $96M Bull Call Spread - December 19th expiration targeting $240-$250 as Fed rate cuts accelerate (3 more cuts expected 2025), geopolitical tensions simmer, and dollar weakness creates 10% tailwind for gold.

GOOGL $60M Dual Call Strategy - Two simultaneous massive trades (7,000 deep ITM + 17,000 ATM calls) betting on Q4 earnings beat, Gemini AI momentum, and Search antitrust resolution by February 2025.

International & Value Rotation ($56.9M Combined)

EFA $12.8M Complex Roll - Buying back puts (closing bullish position) while selling $100 calls as institutional money derisk after 28% YTD rally driven by dollar weakness. ECB cuts to 1.5% by September 2025 expected.

IWD $8M Put Spread - February 2026 insurance against 10% downturn ahead of June 2025 Russell reconstitution ($70-100B trading volume) as 40% recession probability looms and healthcare crisis deepens.

CMCSA $21.1M Butterfly Spread - Range-bound bet between $26-$28 through December 26 expiration as Versant cable spinoff completes Q4 2025. Strategy profits if stock stays flat during corporate action.

Sector-Specific Opportunities ($119.6M Combined)

PLTR $27.9M Calendar Spread - Sold 23,000 December $200 calls for $20M, bought 27,000 November $200 calls for $7.9M (net $12.1M credit) expecting consolidation near $200 through Nov 21, then breakout by Dec 19 as S&P 500 inclusion drives flows.

IBB $6.1M Calendar Roll - Closed November $135 calls for $4.3M profit, opened 6,100 February 2026 $165 calls for $2.04M positioning for J.P. Morgan Healthcare Conference (Jan 13-16) that generated $8.2B M&A deals in 2024.

VST $5.1M Dual Call Strategy - Two trades layering calls at $185 (Jan 2026) and $225 (June 2026) betting S&P 500's best performer (+280% YTD) continues as AI data center nuclear power agreements materialize at 2.4 GW Comanche Peak plant.

LHX $1.5M LEAPS Calls - January 2027 $300 strike capturing 14-month upside from $1.88B fresh contracts, Next Gen Jammer production, Golden Dome missile defense awards, and Trump administration defense priorities.

💡 Market Intelligence: What Smart Money Sees

Theme #1: Nuclear Renaissance & AI Power Demand 🔋

The VST $5.1M dual call position isn't just about one stock—it's a bet on the entire AI infrastructure thesis. With McKinsey projecting AI data centers will consume 13% of global electricity by 2030 (42% CAGR), VST's second-largest U.S. nuclear fleet (6,505 MW) becomes critical infrastructure. The $185 January 2026 calls target near-term data center agreements, while the $225 June 2026 moonshot bets on multi-billion dollar PPAs signing.

What matters: Vistra is actively negotiating nuclear co-location at Comanche Peak (2.4 GW) and Beaver Valley (1.8 GW) with "two large companies" per CEO. After FERC's Amazon-Talen rejection, VST's approach focuses on behind-the-meter solutions. If agreements sign, nuclear becomes premium-priced baseload (vs. intermittent renewables), justifying $225+ targets.

Risk: Already up 280% YTD from ~$49 to $186. Valuation stretched with 4.68 debt-to-equity ratio. Any data center deal delays or Winter Storm Uri repeat could gap stock down 20-30%.

Theme #2: Precious Metals Macro Hedge 🏆

The GLD $96M bull call spread is the largest single trade today, and the December 19th timing is deliberate. Someone paid $96M betting gold rallies 6-9% in just 39 days. Why?

- Fed dovish pivot: Three more rate cuts expected in 2025 (following December 2024's 25bps to 4.25-4.50%)

- Dollar weakness: 10.7% H1 2025 decline (worst in 50 years) adds ~10% tailwind to gold

- Geopolitical risk: Middle East tensions, China-Taiwan, Ukraine continue driving safe-haven flows

- Central bank buying: China, India, Turkey accumulated 1,136 tonnes in 2023 alone

Trade structure: December $240-$250 bull call spread. Max profit if GLDGLD-- between $245-$250. Current price $234.85. Needs 2.2-6.4% move—achievable if Fed signals more cuts or geopolitics flare.

Risk: Gamma resistance massive at $240 (127.3B exposure). If dollar reverses on U.S. economic strength, gold vulnerable to 5-10% pullback.

Theme #3: Big Tech AI Monetization Acceleration 🤖

The GOOGL $60M dual call strategy combines two massive trades at 10:49 AM—7,000 deep ITM December $130 calls ($15M) + 17,000 ATM December $195 calls ($45M). This isn't hedging. This is aggressive accumulation before catalysts.

Why December expiration?

- Q4 2024 earnings (late January/early February 2025)

- Gemini AI momentum (consumer + enterprise adoption accelerating)

- Search antitrust case resolution expected early 2025

- Cloud revenue growing 35% YoY ($11.4B Q3 2024)

The PLTR $27.9M calendar spread takes the opposite approach—short December, long November—betting on near-term consolidation followed by post-earnings breakout. Net $12.1M credit collected! Trader profits if PLTR stays near $200 through November 21, keeping sold calls worthless, while bought calls decay slower.

Key insight: Both trades expect Q4 earnings beats but use different structures. GOOGLGOOGL-- buyer wants immediate upside; PLTR seller wants range-bound action first.

Theme #4: Healthcare M&A Inflection 💊

The IBB $6.1M calendar roll is a textbook example of professional trade management. Trader closed profitable November $135 calls ($4.3M), then redeployed into 6,100 February 2026 $165 calls ($2.04M net cost). Net $6.04M committed—but they already extracted $4.3M profit!

J.P. Morgan Healthcare Conference (January 13-16, 2025) is the catalyst. The 2024 conference generated $8.2B in M&A deals (vs $2.65B in 2023). With 64% of investors expecting IPO uptick, falling interest rates, and $350-400B patent cliff forcing Big Pharma to acquire pipelines, biotech M&A wave building.

Top holdings catalysts:

- Amgen MariTide obesity data (imminent late 2024)

- Gilead lenacapavir HIV PrEP filing (99.9% efficacy in trials)

- Vertex Suzetrigine pain drug launch (approved Jan 30, 2025)

- Alnylam AMVUTTRA cardiomyopathy approval (March 23 PDUFA)

Risk: Patent cliff is real ($350-400B revenue at risk through 2030). GLP-1 obesity market consolidating around Novo/Lilly. 39% of small biotechs have <1 year cash runway.

Theme #5: Defensive Hedging Into Year-End 🛡️

The IWD $8M put spread (buying $185 puts, selling $175 puts for February 2026) and EFA $12.8M complex roll (buying back puts, selling $100 calls) show institutional caution.

Why hedge now?

- 40% recession probability over next 12 months (up from 23% in January)

- UnitedHealth slashed 2025 earnings by 47% ($30/share to $16/share)

- Trade war escalation: 100% additional tariff on Chinese goods (total duty 155%)

- Fed now expects only 2 cuts in 2025 (down from 4 expected)

IWD structure: Protects $1.54B portfolio against 10% decline ($204 → $185) for just $2.8M net cost (0.18% insurance). Max profit if Russell 1000 Value drops to $175 (14.87% decline).

EFA structure: Closing profitable bullish put sales, capping upside at $100 with call sales. After 28.2% YTD rally, taking chips off table.

📅 Catalyst Calendar: When These Bets Pay Off

🔥 WEEKLY (Nov 11-15)

Near-term volatility expected:

- VST implied move: ±$8.39 (±4.51%) by Nov 14

- LHX implied move: ±$6.08 (±2.09%) by Nov 14

- No major earnings, but options expiration dynamics create gamma hedging flows

📆 MONTHLY (Nov 16-21) - Critical OPEX!

Nov 21 Monthly Expiration:

- PLTR November $200 calls expire - Calendar spread profits if stays near $200

- Multiple tickers have significant open interest at monthly strikes

- Quarterly earnings season underway (tech, retail, industrials)

🎄 QUARTERLY (Dec 19 - Triple Witch)

December 19th Quarterly Expiration (39 days):

- GLD $96M bull call spread expires - Needs $240-$250 move

- GOOGL $60M dual calls expire - Q4 earnings catalyst

- CMCSA $21.1M butterfly expires - Versant spinoff completion

- Triple witch = increased volatility from equity options, index options, index futures all expiring

- Holiday trading patterns historically bullish for equities

Near-term catalysts before Dec 19:

- Amgen MariTide obesity data (late Nov/early Dec)

- Fed December FOMC meeting (Dec 17-18) - rate decision

- Q4 earnings preview season begins

- Year-end portfolio rebalancing flows

🚀 Q1 2025 (January-March)

January 2025:

- J.P. Morgan Healthcare Conference (Jan 13-16) - IBB $6.1M trade targets this

- Q4 2024 earnings season kicks off

- GOOGL Search antitrust resolution expected

- Gilead lenacapavir HIV PrEP FDA filing decision

- Trump administration budget priorities clarify

February 2025:

- PLTR Q4 Earnings (Feb 3) - S&P 500 inclusion effects, AIP adoption

- EFA, IWD, IBB options expire Feb 20 - Major gamma event

- MSCI Index Rebalancing (Feb 11) affects EFA

- ECB rate decisions (Jan 30, March 13) - path to 1.5% by Q3

March 2025:

- Alnylam AMVUTTRA cardiomyopathy PDUFA (March 23)

- Q1 2025 earnings guidance begins

- Russell reconstitution preparations start (April 30 "Rank Day")

📊 LEAPS (2026-2027)

June 2025:

- Russell 1000 Value Reconstitution (June 27) - IWD put spread protects this

- VST $225 calls expire June 18, 2026 - Long-dated moonshot bet

- Earnings season Q1 2025 complete

2026-2027:

- COIN January 2027 LEAPS - Multi-year crypto bull thesis

- LHX January 2027 $300 calls - Defense sector multi-year catalysts

Key dates summary:

- This Week: VST/LHX weekly vol

- Nov 21: PLTR calendar spread decision point

- Dec 19: GLD, GOOGL, CMCSA quarterly expiration

- Jan 13-16: JPM Healthcare Conference (IBB catalyst)

- Feb 3: PLTR earnings

- Feb 20: EFA, IWD, IBB monthly expiration

- June 27, 2025: Russell reconstitution

- Jan 2027: COIN, LHX LEAPS expiration

🎓 Trading Ideas by Investor Type

💥 For the YOLO Trader (High Risk/High Reward)

Best Trade: Follow the PLTR $27.9M Calendar Spread structure (but scaled down!)

Your Play:

- Sell 10x PLTR Dec 19 $200 calls (collect ~$7,000)

- Buy 10x PLTR Nov 21 $200 calls (pay ~$3,000)

- Net credit: ~$4,000 (you get paid to enter!)

How you win:

- If PLTR stays $195-$205 through Nov 21: Sold calls expire worthless, you keep $7K

- If PLTR stays near $200 through Dec 19: Full profit realized (~$4K credit kept)

- If PLTR breaks out after Nov 21: Bought calls gain value, sold calls still OTM

How you lose:

- If PLTR rockets above $210 immediately: Sold calls get assigned, bought calls don't keep up

- If PLTR crashes below $190: Both calls expire worthless but you still keep net credit

Why this works for YOLO: You're collecting premium (immediate cash!), betting on near-term range before breakout, and the trade PAYS YOU to enter. Max risk defined at spread width minus credit.

Position sizing: 2-5% of portfolio max. If you have $50K, allocate $1,000-2,500.

Exit plan: Take profits at 50-75% max gain. Don't get greedy waiting for expiration.

📈 For the Swing Trader (3-6 Week Holds)

Best Trade: GLD $96M Bull Call Spread replicated at smaller scale

Your Play:

- Buy GLD Dec 19 $237 calls

- Sell GLD Dec 19 $245 calls

- Net debit: ~$3-4 per spread ($300-400 per 1 contract spread)

Why this timeframe works:

- 39 days to expiration = perfect swing trade duration

- Fed December meeting (Dec 17-18) is binary catalyst

- Holiday seasonal patterns historically bullish for gold

- Geopolitical risks (Middle East, China-Taiwan) provide volatility

Entry timing:

- Best entry: On any dip to $230-232 support (gamma floor at $230 with 61.4B exposure)

- Acceptable: Current levels if dollar continues weakening

- Avoid: Chasing above $238 (reduces profit potential)

Target profits:

- Take 50% off at $240 break (50% of max gain)

- Take remaining 50% at $243-245 (75-100% of max gain)

- Set stop loss at $232 break below support

Risk management:

- Position size: 5-10% of portfolio

- Max loss: $300-400 per spread (defined and limited)

- Breakeven: ~$240-241

- Gamma support at $230 (61.4B) and $225 (69.2B) limits downside

Why this beats stock: Defined risk, no overnight gap risk beyond spread width, leveraged upside if gold rallies.

💰 For the Premium Collector (Income Focus)

Best Trade: IWD $8M Put Spread - Sell insurance at strong gamma support

Your Play:

- Sell IWD Feb 20, 2026 $200 puts (collect premium)

- Buy IWD Feb 20, 2026 $195 puts (limit risk)

- Net credit: ~$150-200 per spread

Why this generates income:

- Strong gamma support at $200 (0.088B) means dealers defend this level

- Current price $204.43 = 2.71% buffer before short puts tested

- 102 days = collect theta (time decay) while IWD consolidates

- Even if IWD pulls back to $200, still profitable

Your income breakdown:

- Collect $150-200 upfront (deposited immediately!)

- Max profit: Keep full premium if IWD stays above $200

- Max risk: $350-450 (spread width $5 - credit received)

- Annualized return: 40-57% on capital at risk if successful

Management:

- Take profits at 50% of max gain ($75-100 per spread) if achieved in 30-60 days

- Roll down strikes if IWD rallies above $210 (adjust to $205/$200 spread)

- Close early if IWD breaks below $197 support (cut losses)

Why this works for income collectors:

- Positive theta (time decay works FOR you)

- Defined max risk ($350-450 per spread)

- High probability setup (market implies 65-70% chance of staying above $200)

- Can repeat monthly, collecting premium consistently

Position sizing: 10-15% of portfolio. If you have $100K, allocate $10-15K = 20-30 spreads.

Advanced move: Layer multiple expirations (Dec, Jan, Feb) to smooth income and reduce timing risk.

🎓 For Entry-Level / New Options Traders

Best Trade: Own the ETFs directly, learn by watching

Your Play (Safest):

- Buy 10-50 shares GLD at $234.85 = $2,348-$11,742

- Buy 10-50 shares IBB at $158.63 = $1,586-$7,931

- Hold through December/January catalysts

- Set 5% stop losses to protect capital

Why ETFs for beginners:

- No options complexity, time decay, or strike selection

- No expiration risk - you control when to sell

- Diversification: GLD tracks gold, IBB tracks 219 biotech companies

- Dividend income: IBB pays 0.17% yield

- Learn by watching how unusual options activity drives price

What to watch:

- If GLD rallies to $240-245 by Dec 19, the $96M call spread is printing money

- If IBB breaks $165 by Feb 20, the $6.1M calendar roll is successful

- Track gamma levels: $230 support for GLD, $155 support for IBB

- Notice how price respects these gamma walls (dealers hedge by buying/selling)

When to sell:

- GLD: Take profits at $242-245 (near resistance)

- IBB: Take profits at $168-172 (near implied move upper range)

- Cut losses if stop loss hit (5% below entry)

Next step after mastering this: Once comfortable with ETF price action and gamma dynamics, try ONE simple option:

- Buy 1x GLD Dec $235 call (costs ~$5-7 per share = $500-700 total)

- Max loss: $500-700 (know this upfront!)

- Max gain: Unlimited if GLD rallies

- Practice position sizing, entry timing, profit taking

- Experience theta decay firsthand

- Learn by doing with small size

Books to read while holding:

- "Options as a Strategic Investment" by Lawrence McMillan

- "The Options Playbook" by Brian Overby

- Watch the unusual options flow unfold in real-time

Key principle for beginners: Start small, learn by doing, protect capital. Options are leverage - they magnify both gains AND losses. Master the basics before deploying size.

⚠️ Risk Management: Don't Blindly Follow Whale Trades!

Critical Warnings

1. Unusual ≠ Profitable

Just because smart money deployed $333.5M doesn't mean these trades will work. Z-scores measure statistical unusualness (size relative to normal activity), NOT probability of success. Many institutional trades are hedges, portfolio adjustments, or tax-loss harvesting—not directional bets.

Example: The IWD $8M put spread is insurance, not a bearish bet. If markets stay calm and IWD doesn't drop 10%, the trader loses $2.8M (but their $1.54B portfolio gained elsewhere).

Takeaway: Understand the INTENT behind each trade before copying. Is it speculation or protection?

2. Time Horizon Matters Enormously

LEAPS trades (COIN Jan 2027, LHX Jan 2027) have 14+ months to work out. They can withstand 20-30% pullbacks and still profit if the long-term thesis plays out.

Monthly trades (GLD Dec 19, GOOGL Dec 19, PLTR Nov 21) have 11-39 days. They expire worthless if wrong by just a few percentage points or days.

Don't mix timeframes! If you buy GLD Dec calls because you like gold long-term, you're mismatched. Short-dated options require precision timing AND directional accuracy.

Takeaway: Match your timeframe to the trade. Swing traders use monthlies; LEAPS require 12-18 month conviction.

3. Position Sizing is EVERYTHING

Institutional traders risking $1.5M on LHX LEAPS likely have $500M-1B portfolios (0.15-0.3% risk). For them, total loss is rounding error.

For retail traders: If you have $50K portfolio and risk $1,500 (3%) on one LEAPS call, you're taking the SAME relative risk. But you can't afford 10-20 losers in a row like institutions can.

Position sizing rules:

- LEAPS (high risk, multi-year): Max 1-2% per trade

- Monthlies (moderate risk): Max 3-5% per trade

- Spreads (defined risk): Max 5-10% per trade

- Stock/ETF (low risk): Up to 15-20% per position

Example: $100K portfolio

- LEAPS call: $1-2K max

- Monthly spread: $3-5K max

- ETF position: $15-20K max

Takeaway: Lose small, win big. Survival > home runs.

4. Hidden Risks in Each Trade

GLD $96M: Dollar reversal risk. If U.S. economy stays strong and Fed pauses cuts, dollar rallies, gold drops 5-10% fast.

GOOGL $60M: Antitrust risk. If judge orders breakup (Chrome, Android spin-offs), stock gaps down 15-25%.

PLTR $27.9M: Execution risk. Sold December calls (short volatility). If earnings beat huge and stock gaps to $220, the sold calls explode in value, capping gains.

VST $5.1M: Operational risk. Another Winter Storm Uri (2021 caused $1.6B negative cash flow) gaps stock down 20-30% overnight.

IWD $8M: Recession risk materializing. 40% probability means 60% probability it DOESN'T happen. Paying $2.8M for insurance that may not be needed.

IBB $6.1M: Patent cliff and cash burn. $350-400B in drug revenues losing exclusivity through 2030. 39% of small biotechs have <1 year cash.

Takeaway: Every trade has a "what if it goes wrong" scenario. Identify it BEFORE entering.

5. Emotional Discipline Beats Analysis

The PLTR calendar spread trader collected $12.1M net credit. But if PLTR gaps to $215 on earnings, the emotional pain of capped gains could cause panic selling of the long November calls at exactly the wrong time.

Common emotional mistakes:

- Chasing: Buying after 280% rally (VST) because of FOMO

- Panic: Selling at support (GLD $230) right before bounce

- Greed: Holding for 100% gain instead of taking 50% profit

- Revenge trading: Doubling down after loss to "get even"

Solution:

- Write down entry, stop loss, profit targets BEFORE entering

- Use alerts, not constant monitoring (reduces emotional reactions)

- Accept that 40-60% win rate is realistic (not every trade works!)

- Track your actual P&L vs. benchmark (S&P 500) quarterly

Takeaway: The best plan executed poorly beats the perfect plan abandoned mid-trade.

6. Patience > Perfection

Smart money has been loading up since August (LHX up 50%, VST up 280%). You're seeing the trades NOW, but they've been building positions for months.

Don't force trades. If you missed VST's run from $49 to $186, don't chase at $186. Wait for:

- Pullback to $175-180 gamma support (6-9% correction)

- Or confirmation of data center deals (new catalyst)

The market will give you opportunities. There are unusual options trades EVERY SINGLE DAY. Missing one trade doesn't matter if you preserve capital for the next setup.

Takeaway: Patience is a position. Cash is a position. Waiting for YOUR entry > jumping into someone else's trade at their entry + 20%.

📚 Final Thoughts: Using This Newsletter

This newsletter decodes unusual options activity to help you understand what sophisticated investors are thinking—NOT to blindly copy their trades.

How to use this information:

Remember: The goal isn't to win every trade. The goal is to survive long enough to compound the winners and cut the losers quickly. Professional traders accept 40-60% win rates—they just ensure winners are 2-3x larger than losers.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. Unusual options activity reflects statistical measures, not predictions of profitability. Always do your own research and consult a licensed financial advisor before trading.

Ainvest Option Flow Digest is published daily, analyzing institutional options positioning to help retail traders understand smart money flows. Subscribe for daily updates and in-depth analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.