Ainvest Option Flow Digest - 2026-03-26: $59.7M in Smart Money Bets — Iran Hedges, Credit Stress, and Tech LEAP Bulls All Hit the Tape

$59.7M institutional flow across 9 tickers. PDD $12.7M deep ITM put sell, TQQQ $9.5M LEAP call sell, USO $8.5M bear put spread betting oil peak is in. AMZN bulls counter with $7.9M in Dec 2027 LEAPs. Full breakdown inside.

📅 March 26, 2026 | Unusual Institutional Activity Tracked Across 9 Tickers

🧭 What Happened Today

Today's tape told a story in four distinct chapters: institutions hedging the oil war premium, credit managers bracing for high-yield pain, LEAP bulls quietly loading long-duration tech bets, and commodity players positioning for a silver and energy supercycle. Across 9 tickers, $59.7 million in unusual institutional options flow crossed the wire — ranging from a $12.7M deep ITM put roll on PDD to a $1.4M tail-risk hedge on Alphabet.

The macro backdrop made every trade meaningful: the Strait of Hormuz remains closed, the Fed is holding at 3.50–3.75% with only one projected 2026 cut, and credit spreads are quietly widening while equities hover near key gamma levels. Today's flow is not noise — it is institutional money repositioning for what happens next.

Key themes driving today's flow:

- 🛢️ Iran/Hormuz war hedge: USO bear spread ($8.5M) bets the oil spike unwinds; NEXT covered call ($4.8M) locks in LNG crisis gains

- 🏦 Credit stress hedge: HYG 4-leg put structure ($8.4M) signals high-yield bond pain ahead; Z-score 79.96 on the $78 put leg is one of the most extreme readings of the year

- 🤖 Tech LEAP bulls: AMZN ($7.9M) and TQQQ ($9.5M inverse) both express 21-month views; the bulls and bears are fighting directly in long-duration paper

- 🥈 Commodity supercycle: AG call buy ($1.5M) follows a BMO upgrade 2 days ago; silver at $67–68/oz with J.P. Morgan forecasting $81/oz for 2026

Total premium tracked: $59.7M across 9 tickers

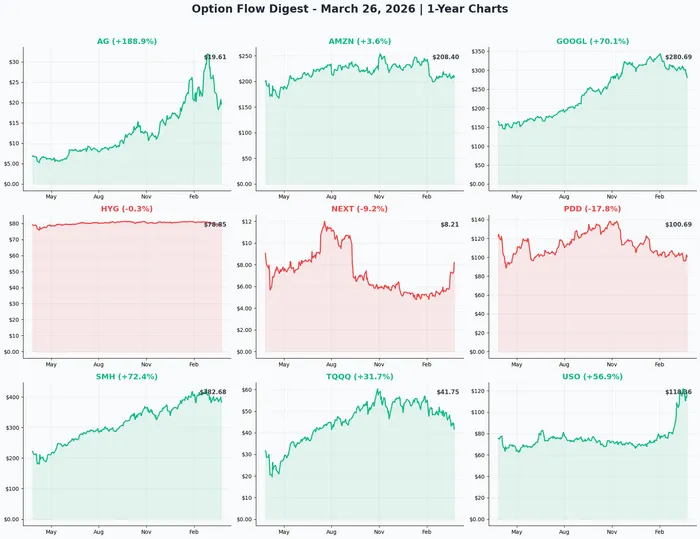

📊 Combined Chart

📋 Today's Flow at a Glance

🔍 Individual Ticker Deep Dives

1. 🐻 PDD — $12.7M Deep ITM Put Roll: Smart Money Stays Long Pinduoduo After Earnings

DECODE THE $12.7M THREE-LEG ROLL AND WHAT IT SAYS ABOUT PDD'S FLOOR →

- Flow: $12.7M — three fills selling $130 puts (April 17), all on the BID

- Unusual Score: Significant (multiple fills at deep ITM, same morning as Q4 earnings)

- YTD Performance: -15%

- The Big Question: Why would any institution sell $130 puts when PDD trades at $101 — and do it the morning after a mixed earnings print?

- What It Really Is: At $28+ of intrinsic value baked in, this is a synthetic long — the effective buy price is ~$101.55, essentially current spot. The trader is being paid to own PDD at today's price with the $130 strike as a formality. Three fills in a complex roll pattern signal deliberate position management, not a new directional bet.

- The $60B story nobody's talking about: PDD's cash fortress of RMB 422B now exceeds Alibaba for the first time in history — at ~10x forward earnings, this is one of the cheapest large-cap e-commerce stocks globally. The institution knows this.

- Catalyst: Q1 2026 earnings ~May 22 (de minimis damage first revealed); EU EUR 3/item duty effective July 1

- Risk: SAMR investigation (100+ regulators raided HQ in January) remains open with no resolution timeline; break below $100 gamma support triggers accelerated selling

2. 🐋 TQQQ — $9.5M ATM LEAP Call Sell: A Whale Collects 36.7% Premium and Bets Against the Nasdaq Bounce

UNPACK WHY SOMEONE COLLECTED $9.5M SELLING 22-MONTH NASDAQ CALLS →

- Flow: $9.5M — 6,000 contracts of January 2028 $42 calls sold in two fills, both on the BID

- Unusual Score: Z-scores of 372 and 66 — EXTREMELY UNUSUAL

- YTD Performance: -17% (vs. QQQ's -2% — volatility decay already compounding)

- The Big Question: Who buys $847M of TQQQ in a single day (March 20) and then turns around and sells $9.5M in ATM LEAP calls six days later?

- The Theta Engine: At $15.70 per contract on a $42.73 stock, the seller collects 36.7% yield over 22 months — nearly entirely time value. Theta decay alone generates ~$720,000/day across 6,000 contracts. The $42 strike is the single largest gamma resistance node in TQQQ's entire options structure.

- Most likely read: A fund that aggressively accumulated TQQQ during the Iran panic (March 20 dip) is now capping their upside and pocketing $9.5M in premium. If called away at $42, their effective exit is $57.70 — solid returns on a dip buy. If TQQQ stays below $42, they keep everything.

- Catalyst: FOMC April 28-29, Mag 7 Q1 earnings (late April), Iran war binary

- Risk: Iran ceasefire + Fed cuts = TQQQ could surge to $60+; naked sellers face serious losses above $57.70

3. 🛢️ USO — $8.5M Bear Spread: Institutional Money Calls the Top on the Iran Oil Spike

SEE THE EXACT MATH ON WHY SOMEONE PAID $4.3M NET TO BET OIL CRASHES 24% →

- Flow: $8.5M gross / $4.3M net debit — simultaneous bear put spread, 7,858 contracts each leg

- Unusual Score: $75 put volume was 6.75x the entire existing open interest in a single print

- YTD Performance: +51% (driven entirely by the Hormuz crisis)

- The Big Question: Goldman Sachs is already forecasting $67 WTI for Q4 2026 — and the EIA's own base case calls for sub-$80 WTI by Q3 if the Strait reopens. Is the war premium already borrowed time?

- The Trade Architecture: Buy $95 put ($6.4M), sell $75 put ($2.1M) = $4.3M net. If USO falls to $75 by October 16 — a level that would imply roughly a full return to pre-war pricing — the trade pays $11.4M. That is 2.65x on invested capital.

- Breakeven: USO at $89.55 (a 23.9% decline from today's $117.61 spot). Needs a substantial unwind, not just a dip.

- Catalyst: Weekly EIA inventory reports (consecutive builds already showing demand destruction), April 5 OPEC+ meeting, Hormuz diplomatic developments

- Risk: Iran escalation to Saudi/UAE targets = USO stays above $100; full $4.3M debit lost if USO above $95 at October expiry

4. 🛡️ HYG — $8.4M Credit Hedge: Institutions Are Bracing for High Yield Pain

DECODE THE 4-LEG CREDIT HEDGE WITH A Z-SCORE OF NEARLY 80 →

- Flow: $8.4M — four simultaneous legs at 12:50:42, all identical size

- Unusual Score: Z-score 79.96 on the $78 April 2 put — nearly 80 standard deviations above normal. This is one of the most extreme readings of the year on any HYG contract.

- YTD Performance: +8% total return, but current price $79.02 sits near the lower end of its range

- The Big Question: The $78 put had only 1,700 contracts of open interest before this trade. Someone just created 75,000 new contracts — 44x the existing OI — at urgency prices (above the ask on the $74 put leg). What do they know about the next three weeks?

- The Structure: Close near-term $79 puts, replace with layered protection at $78 (April 2), $75 and $74 (April 17). Net cost ~$5.3M after the $3.1M received on the close. This is a roll — not a new bet, but a restructured one with a clear view that the stress gets worse, not better.

- The Macro Context: Moody's US corporate default metric at 9.2% (post-financial crisis high); Goldman Sachs 30% recession probability; HYG OAS widened 24 bps in March alone. Credit was already under pressure before today's hedge was placed.

- Catalyst: March NFP (April 3), Q1 2026 earnings season (early April), FOMC June 16-17

- Risk: Iran ceasefire compresses inflation expectations, Fed signals dovish pivot — HYG rallies through the $79 gamma wall and puts bleed theta

5. 🐂 AMZN — $7.9M in Dec 2027 LEAP Calls: Amazon Bulls Are Loading Up for the Long Game

ANALYZE WHY SOMEONE PAID $6.7M FOR A SINGLE AMZN CALL AND ADDED A $1.2M MOONSHOT →

- Flow: $7.9M — two BTO LEAP calls: $250 strike ($6.7M, 2,000 contracts) and $350 strike ($1.2M, 1,000 contracts), both expiring December 17, 2027

- YTD Performance: -8.3% (post-capex selloff)

- The Big Question: Amazon just announced $200B in 2026 AI/cloud capex — the largest infrastructure bet in corporate history — and the stock got hammered for it. Are these LEAP buyers saying the market is wrong?

- The Dual-Strike Strategy: The $250 call is the conviction trade (18% OTM, realistic per analyst consensus). The $350 call is the moonshot kicker (65% OTM, $12.15 cost, enormous payout if AI monetization delivers). Both expire December 2027 — capturing Q1-Q4 2026 earnings, the full Trainium3/4 ramp, Alexa+ monetization maturation, and Project Kuiper expansion.

- AWS re-acceleration is the engine: AWS just reported 24% growth — fastest in 13 quarters. The Dec 2026 implied upper range is already $252.18. The $250 LEAP buyers are betting on the upper bound of what the market itself already considers plausible.

- Catalyst: Q1 2026 earnings April 23 (28 days away — the first major data point post-capex shock), FTC antitrust trial February 2027

- Risk: $200B capex burns free cash flow; tariffs impact e-commerce margins; $210 gamma resistance is an immediate ceiling that has been difficult to crack

6. 🐻 SMH — $5.3M Bearish Blitz: Smart Money Is Hedging the Semiconductor Supercycle Hard

UNPACK THE COLLAR + NEAR-TERM PUT STRUCTURE AND WHAT IT SAYS ABOUT TSMC EARNINGS →

- Flow: $5.3M — three coordinated trades: $367.50 put (April 17, $1.1M), $380 put / $410 call collar (May 15, ~$2.3M/$1.9M)

- Unusual Score: Z-scores of 15.03 and 12.43 on the collar legs — EXTREMELY UNUSUAL; 111x Vol/OI ratio on the near-term put

- YTD Performance: +12.9% (but down 6.4% in the week ending March 21 — worst weekly drop since Liberation Day tariffs)

- The Big Question: Micron just reported $23.86B (blew away the $20.07B estimate). Broadcom AI revenue up 106% YoY. NVIDIA beat and guided $78B. And yet, big money just deployed $5.3M in bearish structures. Why?

- The Timing Tells the Story: The near-term $367.50 put expires April 17 — the exact same window as TSMC's Q1 2026 earnings (~April 16). This trader is paying $1.1M for 22-day protection against a TSMC disappointment. The collar extends that hedge through May 15, capturing ON Semi earnings and the setup into NVIDIA's late May report.

- The Collar Math: Buying $380 put ($2.3M) + selling $410 call ($1.9M) = ~$400K net for a nearly self-financing hedge. This is a large long position holder protecting gains, not a naked short.

- Catalyst: TSMC Q1 earnings ~April 16, NVIDIA Q1 FY2027 ~May 27, NVIDIA Vera Rubin GPU launch Q2-Q3 2026

- Risk: Tariff resolution = instant semiconductor rally; TSMC beats and guides high = entire $1.1M near-term put expires worthless

7. 🏭 NEXT — $4.8M LEAP Covered Call: Someone Is Banking LNG Crisis Profits

DISCOVER WHY A WHALE JUST COLLECTED $4.8M CAPPING THEIR NEXT POSITION →

- Flow: $4.8M — 20,000 contracts of January 2027 $7 calls SOLD at midpoint

- Unusual Score: Z-score 37.93 — EXTREMELY UNUSUAL; Vol/OI ratio 2.83x

- YTD Performance: +39% (including +27% in a single week on the Iran-Qatar LNG supply disruption)

- The Big Question: A director bought 71,500 shares three days ago at $7.07 — and then a whale sells $4.8M in ATM LEAP calls today. Is the smart money quietly positioning for both scenarios?

- The Covered Call Math: $7 strike with stock at $7.78 = $0.78 intrinsic + $1.63 time value per contract. The $4.8M premium collected is not a bearish signal — it is a disciplined institutonal strategy to monetize a +39% gain while retaining the core position. Effective exit price if called away: $9.41.

- The LNG Context: Iranian attacks on Qatar's Ras Laffan hub disrupted ~20% of global LNG supply. Economists estimate 5+ years to repair. NEXT's Rio Grande LNG facility (Trains 1-2 at 65% complete, Train 3 at 40%) is the direct U.S. replacement play. But after a 39% YTD run, the easy first leg may already be priced in.

- Catalyst: Q1 earnings (~May/June), Train 4 $50M deferred payment (September 9), Train 1 commissioning late 2026

- Risk: Iran-US de-escalation removes the LNG supply premium fast; Morgan Stanley target $7 and TD Cowen $6 — the stock is already above Wall Street consensus

8. 🥈 AG — $1.5M December Call Buy: A Whale Just Loaded Up on Silver at the Dip

SEE WHY A Z-SCORE 8.1 CALL BUY ON AG TWO DAYS AFTER A BMO UPGRADE MATTERS →

- Flow: $1.5M — 3,326 contracts of December 18, 2026 $25 calls bought at the ASK

- Unusual Score: Z-score 8.1 — EXTREMELY UNUSUAL (4 similar trades in historical data)

- YTD Performance: AG is up +162.5% over the past year (from $6.96 to $20.31), sitting 30%+ below its recent $32.43 high after a sharp silver correction

- The Big Question: BMO Capital upgraded AG to Outperform with a C$35 price target exactly 2 days ago — and now someone drops $1.5M in December calls at the $25 strike. Coincidence or coordination?

- The Silver Macro: J.P. Morgan forecasts silver averaging $81/oz in 2026. UBS targets a mid-year spike toward $100/oz. Silver dropped 6.7% in a single session today — from ~$72.60 to ~$67.75. The call buyer is not fighting the volatility; they are buying it, with 267 days of runway across Q1 earnings (May 13), two mill expansions (H2 2026), and a potential Jerritt Canyon restart announcement.

- The Key Detail: AG's cash position hit a record $937.7M. The dividend was doubled in January 2026. FTSE All-World Index added AG in March. The valuation gap — AG at 2.2x NAV vs. historical 3x+ NAV — is exactly what BMO cited in its upgrade. This call buyer has done the homework.

- Catalyst: Q1 earnings May 13, Del Toro mine sale closing end of April, Santa Elena and Gatos mill expansions H2 2026

- Risk: $25 strike requires a 23% rally from $20.31; breakeven at expiry is $29.50; production guided 8-16% below 2025 record; Mexico concentration risk

9. 🐻 GOOGL — $1.4M Deep Put Bet: Someone Just Paid to Protect Against a 30% Crash

DECODE WHETHER THIS IS A HEDGE OR A DIRECTIONAL BET ON AN ALPHABET MELTDOWN →

- Flow: $1.4M — 9,998 contracts of June 18, 2026 $200 puts bought at the ASK

- YTD Performance: -16.5% from the February 2 all-time high of $343.45

- The Big Question: The ad tech antitrust ruling from Judge Brinkema could land any day — Capitol Forum and legal analysts put >50% odds on structural AdX divestiture. Is this $1.4M the market's way of pricing in that risk?

- The Structure: $200 strike is 30% below the $284.86 spot. At $1.42 per contract, this is cheap insurance on a potential catastrophic outcome — not a base-case trade. Vol/OI of 1.7x confirms this is a new position, not a roll.

- The Most Likely Explanation: A fund with hundreds of millions in GOOGL long exposure is paying $1.42 per contract for disaster protection ahead of the imminent antitrust ruling. If the DOJ gets structural AdX divestiture, GOOGL could be worth $5–15B less in annual revenue. At $1.42, the insurance is cheap.

- The Irony: Even in the bear case, this put needs GOOGL at $198.58 to break even at expiry. At $220, puts are worth $8–10 each — a potential 5.6–7x return. The trade pays massively in a catastrophic outcome but likely expires worthless in any normal scenario.

- Catalyst: Ad tech remedies ruling (imminent — any day now), Q1 2026 earnings April 28, Google I/O May 19-20

- Risk: Behavioral remedies only = massive GOOGL relief rally; puts expire worthless; $1.4M total loss

⏰ Expiration Timeline: What Expires When

Understanding the expiration ladder helps you track which bets are time-sensitive.

Near-Term (Next 2 Weeks): - April 2, 2026 — HYG $78 put (10 days); HYG $79 put settlement (credit roll leg) - This is the first real stress test: the $78 April 2 put was created from almost nothing (OI was 1,700; 75,000 contracts were added today). Watch the April 3 NFP as the catalyst.

April Monthly OPEX (April 17, 2026): - PDD — $130 deep ITM puts expire; $12.7M premium fully collected if below $130 (essentially guaranteed at $101 spot) - HYG — $75 and $74 puts expire; the institutional hedge's outer layers settle - SMH — $367.50 near-term put expires (TSMC earnings ~April 16 is the binary catalyst) - Mark April 17 as a significant single-day settlement across three positions in the digest.

May 15, 2026: - SMH — collar ($380 put / $410 call) expires; captures TSMC earnings + ON Semi results + NVIDIA pre-earnings sentiment

June 18, 2026: - GOOGL — $200 deep OTM puts expire; ad tech ruling + Q1 earnings + Google I/O all fall in this window

October 16, 2026: - USO — bear put spread ($95/$75) expires; the 204-day oil thesis settles

January 15, 2027 (LEAP): - NEXT — $7 covered call expires; Train 1 commissioning story resolves

December 18, 2026 (LEAP): - AG — $25 call expires; silver supercycle thesis fully tested

December 17, 2027 (LEAP): - AMZN — $250 and $350 calls expire; 21-month AI/AWS bull thesis fully tested

January 21, 2028 (LEAP): - TQQQ — $42 covered call expires; 22-month volatility decay thesis concludes

📅 Catalyst Calendar: Mark These Dates

Separate from expiration mechanics — these are the events that will move the underlying positions:

🎯 Action Plans by Investor Type

These are educational strategy frameworks, not personalized financial advice. All options trading involves substantial risk of loss.

⚡ YOLO — High Risk / 1-2% Portfolio Max

USO June $100 Puts — "Ceasefire Lottery Ticket" If you have strong conviction a Hormuz diplomatic breakthrough is coming soon, shorter-dated USO puts give faster, higher-delta exposure than the institutional October spread. Estimated cost ~$800–$1,200 per contract. Set a 30-day exit deadline — if no catalyst by late April, close the position. This is pure event-driven speculation; the position will likely expire worthless if no ceasefire catalyst materializes.

GOOGL June $220 Puts — "Antitrust Disaster Insurance" The whale bought the $200 puts; the $220 strike gives you similar exposure at a strike that is 22.7% OTM with a more achievable payout scenario. If GOOGL drops to $200 on catastrophic AdX divestiture news, your $220 puts could be worth $20+ (potentially 20–40x return on premium). Size this at no more than $500–$2,000 total. This is lottery-ticket territory — the probability of maximum profit is very low.

📈 Swing — 3-5% Portfolio / Defined Risk Only

SMH May 15 $385/$370 Bear Put Spread — "TSMC Earnings Insurance" Mirror the institutional collar thesis in a defined-risk structure. Buy the $385 put, sell the $370 put, same May 15 expiration. Cost roughly $5–7 per spread. Max profit ~$15 per spread if SMH closes below $370 by May 15. You are positioned alongside the same bear thesis and expiration as today's institutional collar. Risk: TSMC earnings beat and semiconductor sector rips higher.

AG December $25/$30 Call Spread — "Silver Supercycle with a Cap" If you want exposure to the $1.5M silver thesis without paying $4.50 for the naked $25 call, buy the $25 call and sell the $30 call (same December 18, 2026 expiry). Net cost roughly $2.50–$3.00. Max profit ~$2.00–$2.50 per spread if AG reaches $30 by December. Captures the BMO upgrade re-rating thesis while reducing the breakeven hurdle from $29.50 to approximately $27.50–$28.00.

💰 Premium Collector — Income / Moderate Risk

NEXT January 2027 $9 Covered Call — "Shadow the LNG Whale" If you own or plan to buy NEXT shares, sell the January 2027 $9 calls against your position. You are mirroring what today's institutional seller is doing, just at the $9 strike (vs. $7) to retain more upside participation before getting called away. Collect income while waiting for the Train 1 commissioning story to develop. Risk: losing upside if NEXT surges above $9 on fresh LNG supply disruption news.

HYG April 17 $77/$75 Bear Put Spread — "Follow the Credit Hedge" A small, defined-risk version of the institutional put structure. Buy the $77 put, sell the $75 put, April 17 expiration. Cost approximately $0.15–$0.25 per spread. Catches the implied lower range scenario ($77.64) without needing a crash. Best for traders who want a defined-cost hedge against Q1 earnings credit stress.

🧱 Entry Level — Conservative / Long Duration

Buy AG Shares at $18.50–$19.00 Support — "The Beginner Silver Play" Instead of the options, consider buying AG shares near the strong gamma support at $19.00 (6.03 gamma exposure). Stop at $16.50 (below the $17 structural floor). Target $24–$26 on the 12-month BMO thesis. Risk/reward is approximately 1:3. You capture the silver supercycle thesis without time decay risk, and collect AG's 2% quarterly dividend formula while you wait for the May 13 earnings catalyst.

Watch AMZN for a $200 Entry — "The Post-Capex Buyback" The $200 level is the single largest gamma support in AMZN's structure (46.4 GEX). If the stock pulls back to $200 on any macro weakness before the April 23 earnings, that is the buy-the-dip level the institutional LEAP buyers are likely relying on as their floor. AMZN at $200 is ~16x forward earnings with AWS growing at 24% — this is not a broken business.

⚠️ Risk Management Reminders

Across all positions discussed today:

- Define your risk before you enter. Every trade in today's digest has a clearly stated maximum loss. Match your position size to your actual risk budget, not your conviction level.

- The Iran war is the master variable. USO, NEXT, HYG, TQQQ, and GOOGL are all either directly or indirectly tied to the Strait of Hormuz binary. A sudden ceasefire announcement could simultaneously rally oil, compress credit spreads, lift equities, and deflate TQQQ's volatility premium — reversing multiple positions at once.

- The antitrust ruling on GOOGL could land any day. If you are long GOOGL, consider inexpensive defined-risk protection before that ruling hits. The $200 put today is cheap institutional insurance; a $265/$250 bear put spread is the smarter retail alternative.

- Deep ITM put selling (PDD) carries near-stock-equivalent risk. Selling the $130 puts when PDD is at $101 means delta is near -1. A 20% drop in PDD from here creates mark-to-market losses that can substantially exceed the $12.7M premium collected.

🏆 The Bounty Program — Ainvest x TradeStation Collaboration

Guaranteed $150 Visa Gift Card + Up to $5,000 in Stackable Bonuses

Ready to put your option flow insights into action? We've partnered with TradeStation — a 30+ year brokerage pioneer — to bring you an exclusive deal:

📌 How it works: 1. Open a new TradeStation account through Ainvest's exclusive link 2. Fund with $2,500+ opening balance 3. Make your first trade — any ticker, any size

🎁 What you get: - Guaranteed $150 Visa Gift Card — profit or loss, the value is yours - Stackable cash bonuses deposited directly to your account:

All bonuses stack on top of the guaranteed $150 gift card. 30-day verification period applies. New TradeStation customers only.

Sponsored collaboration between Ainvest and TradeStation

🔗 Full Analysis Library — March 26, 2026

All 9 deep-dive analyses are live:

⚠️ Disclaimer

This newsletter is for educational and informational purposes only and does not constitute financial advice or a solicitation to buy or sell any security. Options trading involves substantial risk of loss and is not appropriate for all investors. You can lose your entire investment — or more — when trading options. Past unusual options activity does not guarantee any future price movement in the indicated direction. All strategies discussed carry real risk of loss. Position sizing, risk management, and suitability are your responsibility. Always conduct your own research and consult a licensed financial advisor before making any investment decisions. Ainvest does not take positions in the securities mentioned in this newsletter.

Ainvest Option Flow Digest is published daily, analyzing institutional options positioning to help retail traders understand smart money flows. Subscribe for daily updates and in-depth analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO