AI Workloads Raise Storage Demand: Is Sandisk Positioned to Benefit?

Sandisk SNDK is emerging as a key beneficiary of the rapid expansion in AI workloads, which is increasing global data storage requirements. Training and inference workloads generate and process enormous volumes of data, requiring high-performance systems capable of handling frequent data access, movement and retrieval. As hyperscalers and enterprises expand AI infrastructure, demand for high-capacity and low-latency NAND flash-based solutions is rising sharply. Per Fortune Business Insights, the global AI-powered storage market is projected to witness a CAGR of 25.2% from 2026 and reach $271.32 billion by 2034.

Sandisk's technology portfolio is well aligned with these rising needs. The ongoing BiCS8 ramp is strengthening its competitive positioning as NAND content per AI deployment continues to increase, while high-performance PCIe Gen5 enterprise SSDs are gaining traction among hyperscalers building out AI infrastructure. The BiCS8 QLC Stargate product, currently advancing through qualification cycles, could further expand the company's data center presence over the coming quarters.

This technology momentum is translating into financial momentum. Data center revenues grew 76% year over year in the fiscal second quarter, reflecting strong enterprise SSD adoption, while total revenues increased 61% year over year to $3.03 billion. With demand continuing to outpace supply, SandiskSNDK-- expects third-quarter fiscal 2026 revenues between $4.4 billion and $4.8 billion, implying year-over-year growth of 171% at the midpoint.

The Zacks Consensus Estimate for Sandisk’s third-quarter fiscal 2026 revenues is pegged at $4 billion, indicating year-over-year growth of 136.14%. With the data center segment expected to become the largest NAND end market in calendar year 2026, Sandisk appears well-positioned to capture sustained long-term value from the accelerating demand for AI-driven storage infrastructure.

SNDK Faces Stiff Competition

SNDK faces stiff competition as peers also target the AI-driven storage opportunity.

Western Digital WDC remains a direct rival in NAND flash and enterprise SSDs serving hyperscale data centers. Western Digital competes with SNDKSNDK-- across similar enterprise and client flash markets. Western Digital also benefits from deep relationships with major cloud customers building AI infrastructure.

Seagate Technology STX competes primarily in hard disk drives used for large-scale capacity storage. Seagate Technology remains well-positioned in cost-efficient cloud storage deployments. However, Seagate Technology has lower exposure than SNDK to high-performance flash storage increasingly required for AI training and inference workloads.

SNDK’s Share Price Performance, Valuation & Estimates

Sandisk shares have appreciated 219.9% in the trailing three-month period, outperforming the broader Zacks Computer and Technology sector’s decline of 1.3%.

SNDK Stock Outperforms Sector

Image Source: Zacks Investment Research

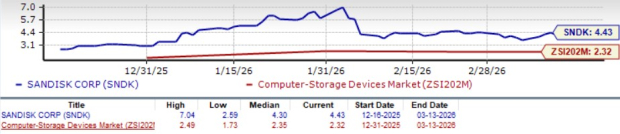

The SNDK stock is trading at a forward 12-month price/sales of 4.43X compared with the Zacks Computer-Storage Devices’ 2.32X. Sandisk has a Value Score of F.

SNDK Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $31.37 per share, up by 15.3% over the past 30 days. Sandisk reported earnings of $2.99 per share in fiscal 2025.

Sandisk Corporation Price and Consensus

Sandisk Corporation price-consensus-chart | Sandisk Corporation Quote

Sandisk currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

Sandisk Corporation (SNDK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet