AI Stocks at a Crossroads: Dotcom Echoes or Sustainable Growth?

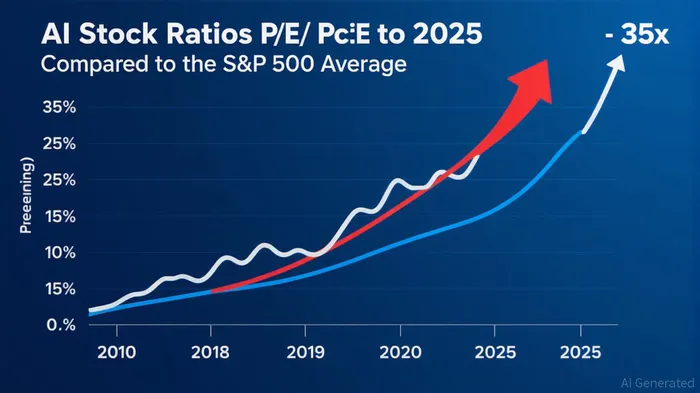

The AI stock rally has reached fever pitch, with valuations now flirting with levels last seen during the dotcom bubble. Leading names like BroadcomAVGO-- (AVGO) and PalantirPLTR-- trade at 33x and 69x forward earnings, respectively, while the sector’s collective P/E ratio exceeds 35x—levels that UBSUBS-- warns leave “little room for disappointment” in cash flow generation [1]. This speculative fervor is reminiscent of 2000, when investors poured money into internet companies with no revenue, only to face a brutal correction. But is history repeating itself, or is this time different?

Short-Term Hype: The Dotcom Parallels

The parallels to the dotcom era are striking. Just as AmazonAMZN-- and eBayEBAY-- dominated headlines in the late 1990s, today’s “Magnificent Seven” tech stocks now account for over one-third of the S&P 500—up from 15% at the dotcom peak [3]. Retail investors are driving much of the buying pressure, with call options surging and institutional investors quietly offloading shares [5]. This liquidity imbalance could lead to sharp corrections if earnings fall short of expectations.

The MIT study revealing that 95% of generative AI pilots fail to deliver immediate revenue growth is a sobering reminder of the gap between hype and reality [1]. Meanwhile, competition is heating up: NVIDIA’s recent sell-off following China’s DeepSeek launch underscores the fragility of dominance in this sector [6].

Long-Term Fundamentals: A Stronger Foundation?

Yet, unlike the dotcom era, today’s AI boom is underpinned by tangible infrastructure and measurable adoption. Microsoft’s Azure cloud segment grew 39% year-over-year in Q2 2025, driven by AI-driven Copilot services and capacity constraints [1]. TSMCTSM--, the chipmaker powering this revolution, raised its full-year revenue guidance to 30% growth, with gross margins near 60% [1]. These fundamentals suggest a sector capable of sustaining its momentum—if execution aligns with expectations.

Moreover, consumer adoption is real: OpenAI’s ChatGPT alone saw 5 billion visits in July 2025 [3]. This contrasts sharply with the dotcom era, where many companies lacked clear revenue models. The AI industry is projected to grow at a 35.9% CAGR, with MicrosoftMSFT-- and MetaMETA-- investing hundreds of billions into data centers [3].

The Risks: Can the Hype Hold?

The answer hinges on execution. While Microsoft and Alphabet’s cloud divisions show strong operating leverage, companies like Palantir and Super Micro ComputerSMCI-- face valuation headwinds [2]. Hyperscaler dependence is another risk: Broadcom’s 40% revenue from cloud clients could backfire if demand slows [4]. Regulatory scrutiny and supply constraints also loom large, with U.S. tech firms committing $350 billion to AI-related capital expenditures in 2025—surpassing the combined capex of all listed energy and utilities companies in the U.S. and Europe [1].

Conclusion: A Calculated Bet

For investors, the key is to separate the wheat from the chaff. While the sector’s long-term potential is undeniable, short-term volatility is inevitable. Focus on companies with proven scalability, like TSMC and Microsoft, and avoid speculative plays with unproven business models. As always, diversification and a long-term horizon will be critical in navigating this high-stakes game.

Source:

[1] AI stocks' valuations nearing dotcom levels; AMDAMD-- upgraded, [https://www.investing.com/news/stock-market-news/5-big-analyst-ai-moves-ai-stocks-valuations-nearing-dotcom-levels-amd-upgraded-4217515]

[2] AI Bubble Signals from History [https://www.ie.edu/insights/articles/ai-bubble-signals-from-history/]

[3] AI Bubble Risks: Lessons from the Dot-Com Crash and AI ... [https://www.digest.tz/ai-bubble-dotcom-lessons/]

[4] This Artificial Intelligence Stock Has Beaten the Market in 9 of the Past 10 Years. And It's On Track to Do It Again in 2025., [https://finance.yahoo.com/news/artificial-intelligence-stock-beaten-market-225100780.html]

[5] Tech Stocks at a Crossroads: Has AI Hype Peaked, or Is There More Room to Run, [https://bookmap.com/blog/tech-stocks-at-a-crossroads-has-ai-hype-peaked-or-is-there-more-room-to-run]

[6] AI Stocks Face 'Show Me' Moment: Why NvidiaNVDA-- Failed To ..., [https://www.investors.com/news/technology/artificial-intelligence-stocks/]

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet