AI Memory Boom: Bernstein’s 2Q26 Upside Surprise

Memory stocks are volatile, yet Bernstein has compelling reasons to stay bullish.

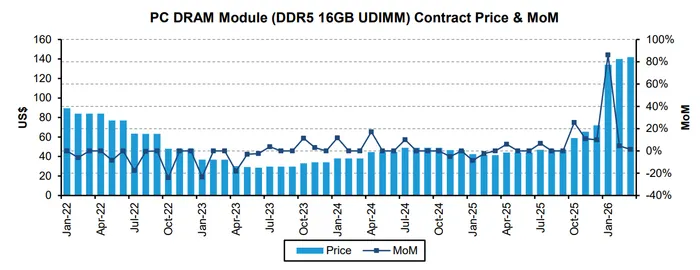

Bernstein’s latest report delivers a clear, data-driven bullish signal for the memory sector. Despite modest late-March spot-price softening in select PC DRAM segments, contract prices continued their upward march through March, setting the stage for another outsized sequential increase in 2QCY26.

Conventional DRAM contracts are projected to rise an additional 40–50% QoQ, while NAND wafer and mobile NAND contracts are expected to jump 70–75% QoQ — ahead of both prior Bernstein forecasts and the broader consensus.

This acceleration occurs against a backdrop of unrelenting AI/server demand, persistent supply tightness, and hyperscalers’ aggressive pursuit of long-term agreements (LTAs) to secure capacity through 2027 and beyond.

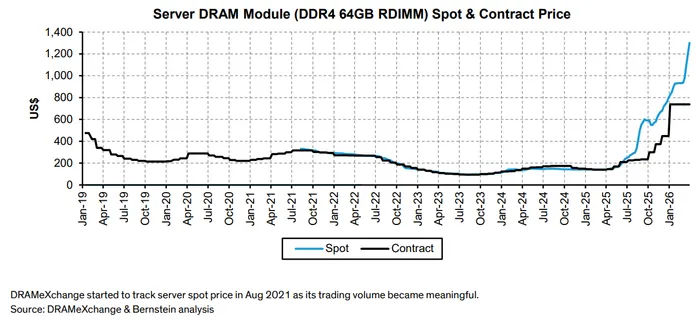

The numbers are stark. Bernstein’s weighted-average DRAM contract prices for 1QCY26 are tracking +105% QoQ versus 4QCY25, with PC DRAM at +109%, server at +103%, and specialty/consumer even stronger.

NAND posted an even more robust +136% QoQ in 1QCY26. Spot prices, while exhibiting some distributor profit-taking in PC DDR5 late in March, remain materially above contract levels and continue to signal pricing power. Server DRAM spot prices, in particular, accelerated sharply (DDR4 +~40% MoM), underscoring the bifurcation between AI-centric demand and legacy end-markets.

TrendForce’s contemporaneous March data aligns almost precisely, forecasting conventional DRAM contracts +58–63% QoQ and NAND +70–75% QoQ in 2QCY26 — revisions that validate Bernstein’s earlier March 18 note on pricing “more than expected.”

Macro and Demand Backdrop Reinforces the Thesis

This price trajectory sits squarely within the structural AI infrastructure supercycle. Hyperscalers and cloud service providers (CSPs) continue to absorb the majority of high-bandwidth memory (HBM) and premium server DRAM output, diverting cleanroom capacity away from conventional DRAM and NAND.

Bloomberg Intelligence and Seeking Alpha commentary highlight that data-center bit growth is on track for +50% in 2026, with AI servers projected to consume ~70% of high-end DRAM wafer starts — a dramatic reallocation that leaves legacy markets (PC, smartphone, consumer) structurally undersupplied.

Recent earnings beats from MicronMU-- (record Q2 FY26 results, HBM sold out through calendar 2026) and Samsung’s guidance for record profits further corroborate the tightness. LTAs — often incorporating volume commitments, prepayments, and price floors — are now the dominant negotiation theme, particularly with U.S. CSPs, but extending to Chinese enterprise buyers as well. This shift materially de-risks near-term revenue visibility for suppliers while extending the upcycle’s duration.

Broader macro conditions remain supportive: Fed easing, resilient U.S. growth, and sustained hyperscaler capex (projected $650–700 bn industry-wide in 2026) provide both liquidity and end-demand tailwinds.

Bernstein maintains Outperform ratings with the following price targets (as of April 2, 2026 closing prices):

Samsung Electronics (005930.KS): KRW 225,000 (from KRW 175,600) — diversified exposure across DRAM, NAND, and foundry, with strong HBM ramp.

SK hynix (000660.KS): KRW 1,150,000 (from KRW 823,000) — HBM leadership and server DRAM strength.

Micron (MU): US$510 (from US$367.85) — HBM sold-out status and aggressive capacity additions position it as a prime beneficiary.

SanDisk (SNDK): US$1,000 (from US$692.73) — NAND leverage and enterprise SSD momentum.

Risk Factors – Explicit and Latent

The report is candid on the cycle’s finite horizon. Pricing power will moderate after 2QCY26 as room for further hikes shrinks; suppliers are already pivoting to LTAs for CY2027+ profitability.

Demand destruction is materializing: PC shipments are now expected to decline 8% (Bernstein sees teens% downside, concentrated in 2H26), smartphones 7–15%, with Chinese/low-end brands hit hardest. Capacity additions ramp in 2H CY27 and CY28 will drive normalization, with prices and margins returning to cyclical troughs by CY28.

Latent risks include faster-than-expected Chinese NAND supply (YMTC), geopolitical friction, and any sharper slowdown in hyperscaler capex. Valuation multiples, while still attractive on forward earnings, embed significant optimism; investor sentiment remains a swing factor.

Conclusion

Bernstein’s March tracker is not merely confirmatory — it is incrementally bullish. The 2QCY26 contract-price upside surprise, underpinned by AI/server demand that shows no signs of abating, extends the memory supercycle’s duration and intensity through at least 1H CY27.

For investors, the setup favors disciplined exposure to the highest-quality names (Samsung, SK hynix, Micron, SanDisk) via the Outperform-rated names, while maintaining caution on valuation and the eventual mean-reversion that memory cycles inevitably deliver.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO