Aflac's Global Resilience: A Dividend Powerhouse in Turbulent Times

When it comes to dividend stocks that weather storms, AflacAFL-- (AFL) stands out like a beacon in a fog. As a Dividend Aristocrat with 43 consecutive years of dividend increases, this insurance giant isn't just about consistency-it's about unshakable reliability. Let's break down why Aflac's global business model and dividend policy make it a standout play, even when the macroeconomic skies turn gray.

The Dividend Engine: A 43-Year Streak with Room to Grow

Aflac's dividend story is the gold standard. In 2025, its payout ratio is projected at a conservative 33%, leaving ample room for growth even during downturns, according to an Aflac press release. Over the past decade, dividends have surged at a 10.9% annualized rate, accelerating to 15.7% in the last five years, the release noted. At $2.32 annualized per share, the current yield of 2.09% to 2.20% isn't just competitive-it's a signal of confidence, according to a GuruFocus article.

But here's the kicker: Aflac's dividend safety isn't just about numbers. It's rooted in a business model that generates consistent cash flows. Supplemental insurance-Aflac's bread and butter-is a non-discretionary need. When the economy tanks, people still need coverage for hospital stays, accidents, and retirement planning. That's why, even during the 2008 crash, Aflac maintained its dividend, hiking it 16% in 2009 after a 20% EPS drop in 2008, according to a Pestel Analysis piece.

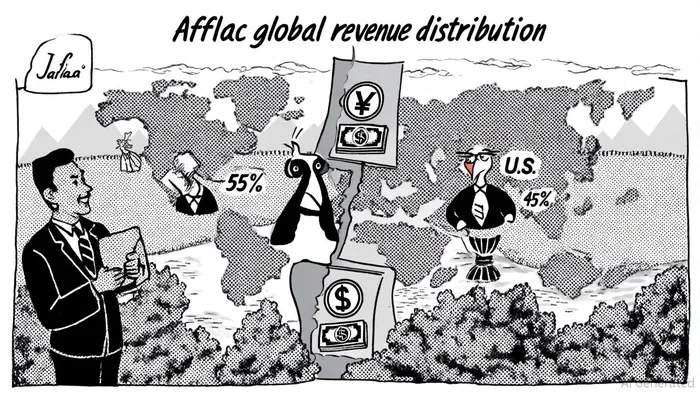

Global Diversification: Japan and the U.S. as a Hedge

Aflac's secret sauce? A two-market engine: Japan and the U.S. In 2024, Japan accounted for 55% of adjusted revenues, driven by products like Tsumitasu, which targets retirement and post-retirement care-a booming sector in an aging society, as noted in the Pestel Analysis piece. The U.S. segment, meanwhile, saw a 5.5% decline in pretax earnings for 2024 but offset this with product innovation, such as an enhanced accident insurance policy covering mental health, also described in that Pestel Analysis piece.

This duality is critical. When the U.S. stumbled during the pandemic, Japan's lower claims activity (due to lockdowns reducing accidents) boosted adjusted earnings, a trend highlighted in the GuruFocus coverage. Conversely, a weaker yen in 2025 hit Japan's revenue but was partially offset by U.S. dollar strength. Aflac's management isn't just playing defense-they're actively hedging. For example, Q1 2025 saw $900 million in share repurchases and a 16% dividend hike, signaling confidence in capital deployment, as the company reported.

Weathering the Storms: Lessons from 2008 and 2020

Let's talk about the real test: how Aflac fared during past crises. In 2008, its EPS fell 20%, but disciplined cost management and a low-capital-expenditure model allowed a 49.6% rebound in 2009, as detailed by the Pestel Analysis piece. During the 2020–2021 pandemic, U.S. premiums dipped 0.9% for the year, but Japan's adjusted earnings surged due to lower claims, according to the GuruFocus coverage. This isn't luck-it's a testament to Aflac's ability to balance regional risks.

Now, in 2025, macroeconomic headwinds like currency swings and investment losses are testing its mettle. Q1 GAAP net earnings plummeted 98.5% year-over-year due to $963 million in investment losses, as reported by GuruFocus. Yet, adjusted earnings held steady at $1.66 per share, and the dividend march continued. This resilience isn't accidental-it's engineered.

The 2025 Outlook: Challenges and Catalysts

Aflac's 2025 results reflect a mixed bag. Fourth-quarter 2024 net earnings hit $1.9 billion, up from $268 million in 2023, driven by $1 billion in investment gains, the company's press release showed. However, Q1 2025 saw a revenue miss, with GAAP earnings at $0.05 per share versus $1.66 adjusted, per the GuruFocus summary. The key here? Don't let short-term volatility cloud the long-term vision.

Aflac's adjusted book value of $52.87 per share at the end of Q1 2025 underscores its financial fortitude, per the company's release. Management is also doubling down on Japan's third-sector insurance market-a $1.2 trillion opportunity-and expanding mental health coverage in the U.S., aligning with growing consumer needs, as noted in the Pestel Analysis piece.

Final Verdict: A Dividend Stock for the Long Haul

Aflac isn't just surviving macroeconomic chaos-it's thriving. Its global diversification, conservative payout ratio, and history of navigating downturns make it a rare breed: a high-yield stock with blue-chip stability. For investors seeking dividends that don't vanish when the going gets tough, Aflac's 43-year streak isn't just a record-it's a promise.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet