AECOM Retains Construction Business: Strategic Win or Risk?

AECOM’s ACM decision to retain its construction management business marks a notable shift from its earlier strategy of streamlining operations toward a more asset-light, higher-margin professional services model. The move reflects management’s growing confidence in the segment’s ability to deliver consistent profitability, supported by improved execution, tighter risk controls and a more selective approach to project bidding.

While the company previously explored a sale, management concluded that the business is an industry leader with a strong cash flow profile that is best utilized through closer alignment with AECOM’s design and advisory segments. This integration is already proving a strategic win in the sports and high-profile events sector, where the combined technical and programmatic expertise secured roles for both the LA '28 and Brisbane 2032 Olympic Games. Financially, the unit remains a stable contributor, with its results and a strong backlog now fully integrated into AECOM's increased fiscal 2026 guidance.

However, retaining the business is not without risks. Construction management typically carries different margin dynamics and execution complexities compared to AECOM’s higher-margin advisory and design segments. Successfully integrating operations while maintaining profitability and discipline will be critical to ensuring the unit enhances, rather than dilutes, overall returns.

Ultimately, the decision reflects a strategic bet that tighter integration and scale advantages will outweigh potential risks. If executed well, retaining the CM business could strengthen AECOM’s position as a full-service infrastructure leader and support its long-term margin expansion and growth objectives.

AECOM’s Competitive Landscape

AECOM's performance reflects broader industry momentum, with peers such as Jacobs Solutions Inc. J and Fluor Corporation FLR also benefiting from a favorable mix of high-value infrastructure and federal projects, improved project execution and a shift toward higher-margin work.

Jacobs remains a key peer, benefiting from strong demand in water, environmental remediation and advanced manufacturing, supported by IIJA-driven infrastructure spending. Similar to AECOMACM--, which recently reported strong net service revenue and adjusted EBITDA growth, Jacobs is capitalizing on rising demand for sustainable infrastructure. Both companies are also expanding their higher-margin advisory and program management capabilities.

Fluor is also strengthening project visibility through a diversified backlog across engineering, procurement and construction markets. At the end of 2025, the company reported a backlog of $25.5 billion, reflecting stable demand across sectors such as LNG, mining and metals, advanced technologies, life sciences, nuclear fuels and national security programs. While Fluor’s model offers greater exposure to large project execution, it also carries relatively higher cyclicality compared with AECOM’s consulting-driven framework.

ACM Stock’s Price Performance & Valuation Trend

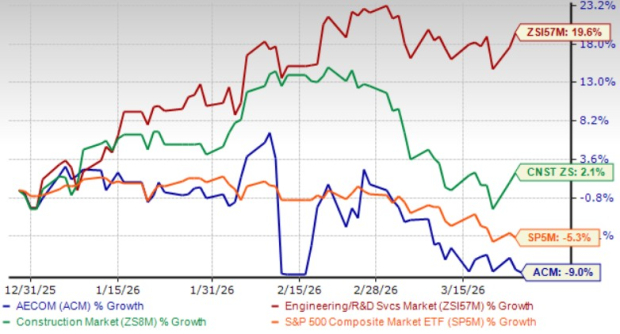

Shares of this Texas-based provider of professional, technical and management solutions have trended downward 9% in the past three months, underperforming the Zacks Engineering - R and D Services industry, the broader Construction sector and the S&P 500 index.

Image Source: Zacks Investment Research

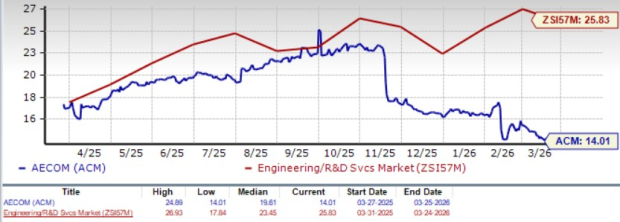

ACM stock is currently trading at a discount compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 14.01, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of ACM

ACM’s earnings estimates for fiscal 2026 and 2027 have trended upward in the past 60 days. The revised estimates for fiscal 2026 and 2027 imply year-over-year growth of 13.5% and 12%, respectively.

Image Source: Zacks Investment Research

AECOM currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fluor Corporation (FLR): Free Stock Analysis Report

AECOM (ACM): Free Stock Analysis Report

Jacobs Solutions Inc. (J): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet