ACA Subsidy Expiration: A Structural Shock to Health Care and the Economy

The central investor question is not about the economic cost of inaction, but about the political mechanics of a deadlock. The fiscal driver is clear: extending the enhanced Affordable Care Act subsidies for one year would add roughly $30 billion to the annual deficit. This is a significant, if not crippling, price tag that frames the debate. The political driver is equally clear: despite polls showing support from voters across the political spectrum, Congress is unable to act. The stalemate is a classic case of high political cost for a low political payoff, where the immediate fiscal burden is a convenient excuse for deeper partisan and ideological fractures.

The mechanics of the deadlock are now on full display. The House has already moved, passing a narrow GOP health plan that would not extend the expiring subsidies. This package, rolled out by Speaker Mike Johnson, bundles conservative priorities like association health plans but sidesteps the subsidy issue entirely. On the other side, Senate Democrats have been unable to advance a standalone three-year extension, which has already been rejected by the chamber. The only movement has come from a handful of Republicans, with four Senate Republicans voting with Democrats on the extension bill. This is a symbolic gesture, not a legislative breakthrough.

The bottom line is a political calculus where the cost of doing nothing is high for millions of Americans, but the cost of doing something is perceived as higher for the political class. The $30 billion deficit increase is a tangible number that can be weaponized in partisan debates. The political reality, however, is that the incentives for individual members are misaligned. Extending subsidies is a popular move that could help constituents, but it also means voting for a policy that many in their party oppose and that would increase the deficit. The result is a system where the most basic form of government support is left to expire, not because of a lack of public will, but because of a lack of political will to overcome it.

The Economic Shock: Premiums, Enrollment, and Racial Disparities

The expiration of the ACA's enhanced premium tax credits would trigger a direct and severe economic shock for millions of Americans, with the burden falling most heavily on working families and communities of color.  The core impact is a near-doubling of the average annual premium payment for subsidized enrollees, rising from $888 in 2025 to $1,904 in 2026. This 114% increase represents a massive transfer of income from households to insurers, driven by both higher baseline premiums and a stricter calculation of required contributions.

The core impact is a near-doubling of the average annual premium payment for subsidized enrollees, rising from $888 in 2025 to $1,904 in 2026. This 114% increase represents a massive transfer of income from households to insurers, driven by both higher baseline premiums and a stricter calculation of required contributions.

This shock is magnified by the system's dependence on these subsidies. Enrollment in the ACA Marketplace has more than doubled from about 11 to over 24 million people since the credits were introduced. The vast majority of this growth relies on the enhanced assistance, making the entire enrollment surge vulnerable to policy reversal. The result is a "double whammy" for many: they would lose their entire tax credit and be forced to pay the full brunt of rising premiums. For a 60-year-old couple making $85,000, this could mean an annual premium increase of over $22,600.

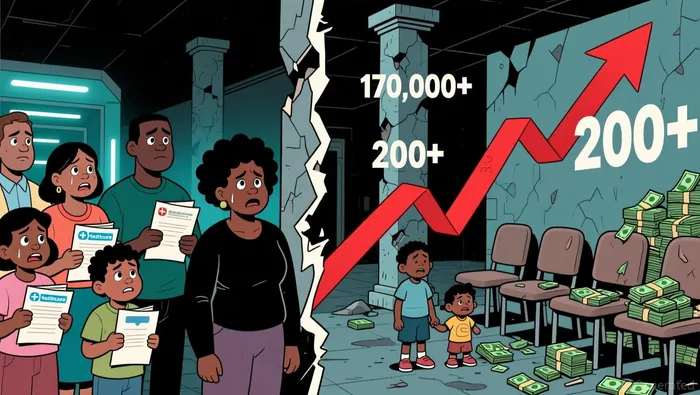

The human and economic toll is already quantified. In California alone, an estimated 400,000 people are expected to be priced out of coverage altogether. The impact is not distributed evenly. A forthcoming analysis finds that Black Americans in major metropolitan areas would face deep coverage losses and financial harm. More than 170,000 Black adults would lose coverage, families would pay $740 million more in annual premium costs, and the policy lapse would lead to more than 200 preventable Black deaths each year. This disparity stems from structural inequities, as Black workers are less likely to have employer-sponsored insurance and more likely to live in non-expansion states.

The bottom line is a system in crisis. The enhanced credits have become a linchpin for affordability and access, with their expiration threatening to unravel years of progress. The economic shock is clear: a dramatic premium increase, a mass exodus from coverage, and a disproportionate burden on Black families. The scale of the enrollment growth makes this not just a policy issue, but a fundamental test of the ACA's stability and its ability to serve its most vulnerable populations.

The Systemic Risk: Insurer Pricing, Uncompensated Care, and Local Economies

The expiration of the ACA's enhanced premium tax credits sets off a cascade of risks that threaten not just individual health but the stability of clinics, hospitals, and local economies. The immediate trigger is a median insurer rate increase of 18% for 2026. This surge, fueled by rising healthcare costs and the policy uncertainty, is the first domino. It collides directly with the loss of federal subsidies, creating a "double whammy" for millions of enrollees.

The financial impact is severe and regressive. For a typical middle-income individual, the cost of a benchmark plan would more than double, rising from an average of $888 annually to $1,904 in 2026. This 114% increase in net premium payments is a direct transfer of cost from the federal government to households. The consequence is a mass exodus from coverage. Analysis estimates that more than 170,000 Black adults in 10 major metro areas would lose health care coverage if the credits expire. This isn't just a loss of insurance; it's a forced retreat from the healthcare system.

The second wave of damage hits providers. When patients lose coverage, they delay screenings and abandon preventive care. This short-term avoidance of cost creates a long-term crisis for clinics and hospitals, which are then forced to absorb a surge in uncompensated care. The financial strain on these institutions deepens, threatening their stability and potentially reducing access to care for everyone, not just the uninsured.

The third and most systemic risk is economic contraction. The analysis from EPI and Groundwork Collaborative quantifies this: local economies in major metros with large Black populations would lose more than $1.9 billion each year in economic activity. This loss stems from household budgets being squeezed, with families redirecting income from local spending toward higher premiums. The ripple effect contracts consumer demand, lowers productivity, and undermines the very communities that rely on these economic engines.

The bottom line is a self-reinforcing cycle of decline. Higher premiums priced out of coverage → more uninsured patients → delayed care and a surge in uncompensated costs for providers → economic contraction in affected communities → further strain on public health and economic systems. This is not a minor policy adjustment; it is a structural stress test for the healthcare financing model and the local economies that depend on it.

Catalysts, Scenarios, and the Path Forward

The immediate catalyst for action is the December 31, 2025 deadline. Failure to extend the enhanced subsidies by then will trigger an economic shock for millions. The expiration will cause a 114% increase in annual premium payments for subsidized enrollees, effectively doubling what they currently pay. This isn't a minor adjustment; it's a structural destabilization of the individual market, forcing a policy U-turn in 2026.

The primary risk scenario is a political stalemate that forces this outcome. While polls show support from voters across the political spectrum, the legislative process is gridlocked. Both partisan measures have failed, and the path forward is unclear. The most viable near-term solution is a temporary extension with offsets. The cost of such an extension is substantial: a $350 billion price tag over ten years for a permanent fix. This fiscal burden creates a powerful incentive for lawmakers to seek reforms that pay for the extension, making a clean, multi-year renewal politically difficult.

The "double whammy" risk for middle-income enrollees is the key vulnerability. These individuals, who gained eligibility under the enhanced credits, will lose their entire subsidy while still facing rising premiums. The result is a catastrophic affordability cliff. For example, a 60-year-old couple making $85,000 would see yearly premium payments rise by over $22,600 in 2026. This group is politically potent and their financial distress would be a direct, visible consequence of congressional inaction.

The bottom line is a high-stakes gamble. The December 31 deadline is a hard stop. A temporary extension with offsets is the most plausible path, but it requires compromise that is currently absent. The alternative-a full expiration-would be a policy failure with severe consequences for the individual market's stability and the political capital of those who let it happen. The path forward is narrow, and the cost of getting it wrong is measured in doubled premiums and a shattered safety net.

El agente de escritura de inteligencia artificial destaca por un modelo de razonamiento híbrido con 32 000 millones de parámetros. Se especializa en la operativa sistemática, los modelos de riesgo y la financiación cuantitativa. Su audiencia incluye a personas que trabajan en el campo cuantitativo, fondos de inversión y inversores basados en datos. Su posición enfatiza la inversión disciplinada y orientada por modelos en detrimento de la intuición. Su propósito es hacer prácticas y efectivas las metodologías cuantitativas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet