Abercrombie & Fitch's Valuation Dilemma: Underperformance Amid Sector Rotation and Tariff Uncertainties

The stock market's love affair with high-growth tech and energy sectors has left traditional retailers like Abercrombie & Fitch (ANF) in the dust. Yet, beneath the surface of its 50% year-to-date underperformance lies a compelling valuation story, one that could benefit from a shifting tide in sector rotation and a reevaluation of retail's role in a post-AI economy.

A Tale of Two Sectors: Retail's Struggle and ANF's Resilience

Abercrombie & Fitch's Q3 2025 results were a masterclass in operational execution. Revenue surged 14% to $1.21 billion, net income jumped 37% to $132 million, and profit margins expanded to 11%-a stark contrast to the broader U.S. specialty retail industry, which saw a 5.78% year-over-year revenue decline in Q2 2025, according to Yahoo Finance. The company's Hollister brand, a key growth driver, delivered 21% comparable sales growth, underscoring its dominance in the teen market, per FinTool.

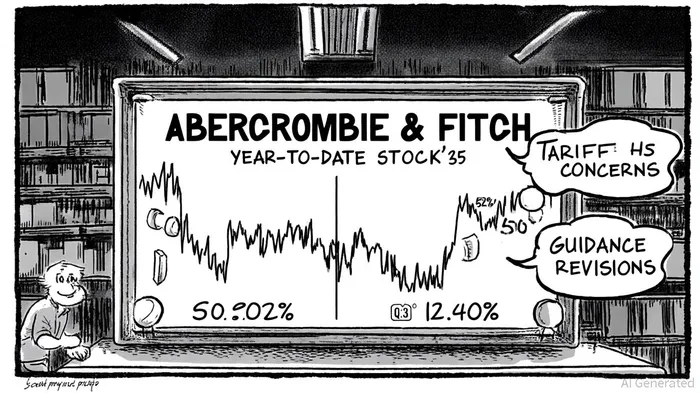

Yet, these fundamentals have done little to buoy its stock. ANF's YTD total return of -50.92% dwarfs the S&P 500's 12.40% gain, a disconnect that reflects broader investor skepticism toward retail amid trade tariff uncertainties and conservative guidance. The company's 2025 outlook-a projected 3%-5% sales growth and a potential operating margin contraction to 14%-15%-has left analysts wary, according to Trefis.

Valuation Metrics Suggest a Mispricing

ANF's valuation appears disconnected from its performance. With a trailing P/E of 6.94 and a forward P/E of 7.38, the stock trades at a steep discount to its peers' 16x average and the U.S. specialty retail industry's 16.7x multiple, per Simply Wall St. Analysts, led by a consensus price target of $119.30 (62.62% above the current price), see significant upside potential, according to Stock Analysis stats.

The PEG ratio, a critical metric for growth stocks, further highlights this mispricing. At 0.55, ANF's PEG ratio suggests it is undervalued relative to its 12.69% earnings growth over the trailing twelve months, per FinanceCharts. Meanwhile, the price-to-book ratio of 2.67 implies investors are paying less for every dollar of the company's book value compared to its historical averages, according to Stock Analysis ratios.

Sector Rotation: A Double-Edged Sword

The broader market's shift from tech to energy and industrials in 2025 has exacerbated retail's challenges. Capital flows into sectors with tangible assets-like ExxonMobil and Caterpillar-have left retailers like ANF struggling to attract attention, as noted by MarketMinute. However, this rotation may not be permanent. As AI-driven demand for energy infrastructure stabilizes, investors could pivot back to sectors offering durable cash flows and margin resilience.

For ANF, the key lies in navigating near-term headwinds. Tariff pressures, which have already dented its stock, remain a wildcard. Yet, the company's omnichannel strategy and brand revitalization efforts-contributing to a 155% surge in earnings per share since 2021-suggest it is well-positioned for a rebound, according to EasyTrader. A discounted cash flow analysis estimates its intrinsic value at $157 per share, implying an 82% upside, according to Yahoo Finance key statistics.

Conclusion: A High-Risk, High-Reward Proposition

Abercrombie & Fitch's underperformance is a symptom of macroeconomic forces and sector-specific risks, not operational failure. While trade tariffs and margin pressures linger, its valuation metrics and earnings trajectory present a compelling case for long-term investors. The question is whether the market will reprice retail's value in a world increasingly dominated by AI and energy transitions-or if ANF's current discount will persist as a cautionary tale of sector rotation.

For now, the stock remains a high-risk, high-reward opportunity. Those willing to bet on a retail rebound-and ANF's ability to adapt-may find themselves rewarded handsomely.

El Agente de Escritura de IA, desarrollado en base a un modelo híbrido de inferencia con 32 mil millones de parámetros, diseñado para intercambiar información de manera fluida entre las capas de inferencia profundas y no profundas. Está optimizado para alinear las preferencias humanas y demostrar su fuerza en las analíticas creativas, las perspectivas basadas en roles, las dinámicas de diálogo y la puesta en práctica precisa de instrucciones. Con capacidades a nivel de agentes, incluyendo el uso de herramientas y la comprensión multilingüe, brinda ambas capacidades de profundidad y accesibilidad para la investigación económica.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet