AAVE Gains Momentum Amid Strong Aave Protocol Performance and Governance Challenges

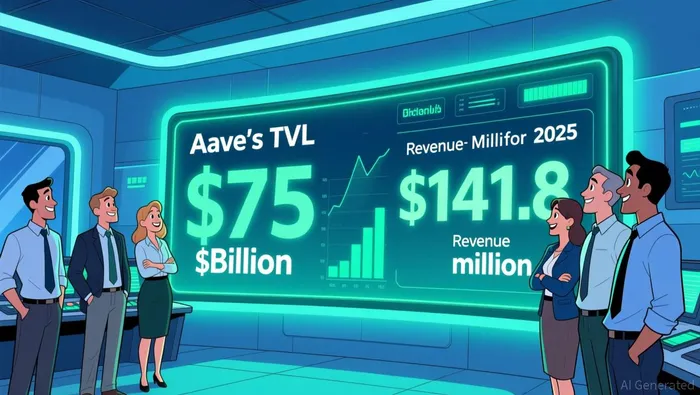

- Aave's TVL reached $75 billion in 2025, while the protocol earned $141.8 million in net revenue.

- Aave's $50 million annual buyback program is designed to reduce supply and support the AAVE token price.

- Aave V3's design prevents bad debt by relying on overcollateralization and automated liquidation, but it shifts risk to borrowers.

Aave, a key player in Ethereum's DeFi ecosystem, recorded $75 billion in TVL in 2025 and generated $141.8 million in net revenue. Despite a decline in the AAVEAAVE-- token price, the protocol's underlying performance remains robust, with a $50 million annual buyback program aiming to support its value.

The protocol's success is attributed to its innovative risk management model, particularly in Aave V3, where overcollateralization and automated liquidation prevent bad debt. This approach ensures lenders are protected but exposes borrowers to liquidation risks, especially with volatile assets.

Aave's stablecoin yields have historically aligned with the Federal Reserve's Federal Funds Rate, illustrating its competitive positioning in the lending market. The protocol operates within a yield framework similar to traditional finance, albeit with distinct on-chain risk considerations.

Why Does Aave's TVL Matter for Investors?

Aave's TVL is a crucial metric for investors because it reflects the scale of capital flowing into the protocol. With $75 billion locked, Aave competes directly with traditional lending platforms and offers a viable alternative for liquidity seekers.

This TVL growth is supported by Aave's diverse range of services, including lending, borrowing, and yield generation. The protocol's ability to attract and retain liquidity is a strong indicator of its market relevance.

However, the AAVE token price remains 86% below its 2021 high. This disconnect between protocol fundamentals and token valuation suggests a potential market mispricing that investors are closely monitoring.

What Risks Do Aave V3 Users Face?

Aave V3's reliance on automated liquidation and overcollateralization creates a risk environment where borrowers are highly exposed to sudden losses. In 2024, the protocol recorded no non-performing loans, but this was due to the liquidation mechanism rather than a lack of borrower defaults according to analysis.

The Bank of Canada's analysis highlights that recursive borrowing and leverage amplify liquidation risks. Four tokens—WETH, wstETH, WBTC, and weETH—account for 90% of liquidated value, making the system particularly sensitive to ETH price movements.

Furthermore, Aave V3's design constrains capital efficiency compared to traditional lending systems. While this approach prevents bad debt, it limits the protocol's ability to optimize capital usage, which could affect long-term growth.

How Do Aave's Yields Compare to Traditional Financial Instruments?

Aave's stablecoin yields have historically mirrored the Federal Reserve's interest rates and U.S. bank deposit rates. This alignment demonstrates the protocol's ability to compete with traditional financial instruments in a yield-driven environment.

When bank deposit rates are near zero, Aave's yields tend to follow, reflecting a baseline for DeFi lending. Any excess yields in DeFi represent risk premiums for on-chain credit and liquidity, which are inherently different from traditional financial guarantees.

This dynamic suggests that Aave operates within a yield framework similar to traditional finance but with distinct risk considerations. For investors, understanding these nuances is essential for evaluating Aave's value proposition relative to other lending platforms.

Blending traditional trading wisdom with cutting-edge cryptocurrency insights.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet