U.S. 8-Week Treasury Bill Auction Yields at 4.300%: A Shift in Short-Term Rates and Market Dynamics

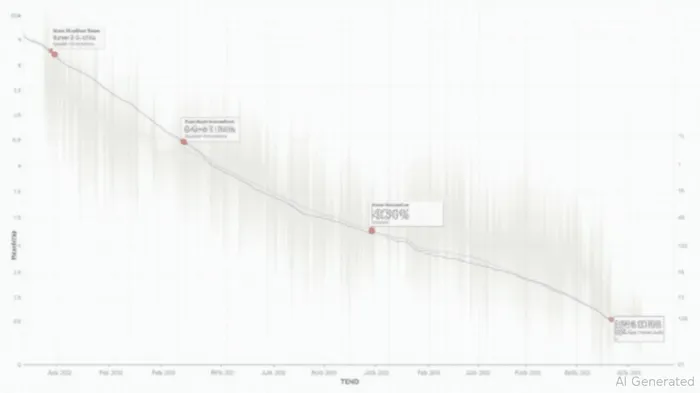

The U.S. Treasury's 8-Week Bill Auction on June 19, 2025, delivered a yield of 4.300%, marking a notable decline from the recent peak of 5.70% in February 2024. With no prior forecast for this auction, the result underscores evolving market sentiment toward short-term rates amid shifting Federal Reserve policy expectations and geopolitical uncertainty.

Opening Paragraph

The 8-Week T-Bill, a key benchmark for short-term borrowing costs, has become a focal point for investors gauging the Federal Reserve's stance on interest rates. Its yield dropped to 4.30%—a level not seen since early 2023—as markets priced in potential rate cuts following the Fed's June decision to hold rates steady. This auction's outcome highlights a critical inflection point for monetary policy and market liquidity.

Introduction

Treasury bill auctions are pivotal for understanding investor confidence and central bank influence. The 8-Week Bill, introduced in 2018 to provide a shorter-duration benchmark, reflects demand for safe-haven assets and expectations of future rate movements. The June 2025 auction's yield of 4.30% falls below the 4.56% recorded in November 2024 and aligns with projections of a gradual decline toward 4.58% by early 2026.

Data Overview

The 8-Week Bill's yield has fluctuated between 4.56% (November 2024) and its all-time high of 5.70% (February 2024), driven by Fed rate hikes and inflation fears. The June 2025 result of 4.30% signals a reversal of this trend, with yields now reflecting market optimism about easing cycles. Key data points include:

- Methodology: Yields are calculated using the monotone convex spline (MC) method, ensuring accuracy based on secondary market quotes.

- Recent Stability: The 3-Month T-Bill rate has hovered near 5.25% since mid-2024, slightly above its long-term average of 4.19%.

Analysis

The 4.30% yield reflects three key dynamics:

1. Fed Policy Signals: The June 2025 Fed meeting indicated a pause in rate hikes and hinted at potential cuts later in the year. This reduced pressure on short-term rates.

2. Geopolitical Risks: Middle East tensions have bolstered demand for Treasuries as a safe haven, depressing yields.

3. Market Equilibrium: Identical yields and dollar prices in recent auctions suggest a balanced supply-demand landscape, with investors calibrating positions ahead of potential Fed moves.

Policy Implications

The Fed faces a delicate balancing act: managing inflation while avoiding a recession. A yield of 4.30% for the 8-Week Bill aligns with the central bank's dovish pivot, but further declines could signal overconfidence in economic softness. Policymakers will monitor data on consumer spending and employment closely.

Market Reactions

- Bond Markets: Short-term Treasuries rallied, with the 2-Year yield dropping by -4 basis points in Q2 2025.

- Equities: Tech and consumer discretionary sectors gained, benefiting from lower borrowing costs.

- Sectors at Risk: Capital Markets and Consumer Durables, historically sensitive to rate changes, face mixed headwinds from both lower yields and slowing demand.

Conclusion

The 4.30% yield on the 8-Week T-Bill marks a significant shift in short-term rate expectations, driven by Fed policy, geopolitical risks, and market dynamics. Investors should remain cautious, as upcoming inflation reports and Fed communications will dictate the trajectory of yields. For now, the data suggests a gradual normalization path, favoring defensive allocations and sectors insulated from rate volatility.

Backtest Analysis: Historical Context for 8-Week Bill Yields

A backtest of the 8-Week Bill's yield performance since its 2018 introduction reveals a strong correlation with Fed rate decisions. During periods of tightening (e.g., 2022–2023), yields rose sharply, while easing cycles (e.g., 2021) saw declines. The current dip to 4.30% aligns with the post-2024 policy reversal, offering a template for future rate movements. Investors are advised to pair Treasury exposure with inflation-hedged assets like TIPS or gold to mitigate risk.

This analysis underscores the evolving landscape of short-term rates and the need for dynamic portfolio adjustments in a post-peak rate environment.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet