7-Year Auto Loans Reshape Automotive Sector Valuations and Risk Profiles in 2025

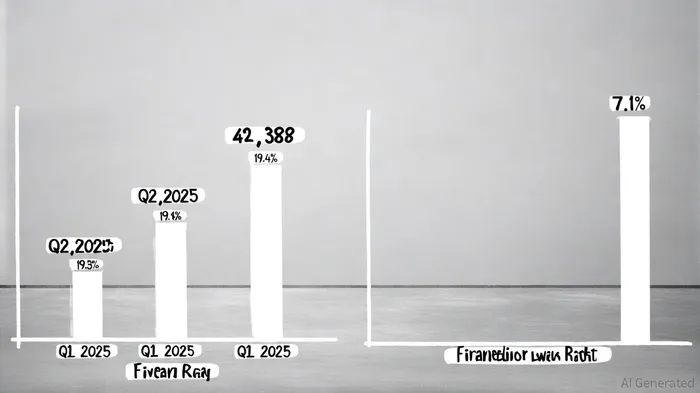

The automotive sector is undergoing a seismic shift as 7-year auto loans surge in popularity, driven by soaring vehicle prices and elevated interest rates. By Q2 2025, these extended loan terms accounted for 22.4% of new-car financing, up from 19.8% in Q1 2025[1]. This trend, while offering short-term relief to borrowers, is reshaping industry valuations, lender profitability, and risk profiles in ways that demand closer scrutiny for investors.

Borrower Behavior and Financial Implications

The average new-car buyer now finances $42,388 at an interest rate of 7.1%, resulting in monthly payments of $741 and total interest costs exceeding $10,000 over seven years[2]. While these terms make monthly obligations more manageable, they amplify the risk of borrowers becoming “underwater,” where the loan balance exceeds the vehicle's depreciated value. For example, a $40,000 loan at 7% interest over seven years incurs $10,711 in interest—nearly double the $5,977 paid on a four-year loan[1]. This dynamic is exacerbated by declining down payments, which have shrunk to an average of $6,433, further stretching borrowers' financial exposure[2].

Sector-Wide Valuation Pressures

The automotive finance sector faces a dual challenge: higher interest income from extended loan terms and increased risk of defaults. Auto loan balances now total $1.7 trillion, with 82% of buyers paying above MSRP during the pandemic peak, locking them into high-interest loans[3]. Lenders are grappling with repossession losses, as auction values for repossessed vehicles have plummeted, and operational costs like storage fees erode recovery margins[3]. Meanwhile, delinquency rates hit 7.9% in Q1 2025—the highest since 2009—with subprime borrowers accounting for 6.56% of defaults[4].

For automakers, the rise in 7-year loans has created a paradox. While longer terms boost sales by improving affordability, they also delay revenue recognition and increase residual value risk. Captive lenders, which dominate new-vehicle financing, are tightening underwriting standards to mitigate exposure, particularly for used vehicles, which face steeper depreciation curves[5].

Investor Implications: Risk and Opportunity

The stock performance of automotive lenders and OEMs is increasingly tied to their ability to navigate these challenges. Captive lenders like Ford Credit and GMGM-- Financial are leveraging AI-driven tools to monitor borrower hardship and adjust credit policies dynamically[4]. However, non-captive lenders, which serve subprime borrowers and finance used vehicles, face steeper headwinds. Their delinquency rates remain significantly above pre-pandemic levels, raising concerns about portfolio quality[1].

Digital transformation is a key differentiator. Lenders adopting digitized underwriting and alternative data (e.g., utility payment histories) are better positioned to expand credit access while managing risk[5]. Conversely, firms reliant on traditional models risk margin compression as delinquency rates climb. For investors, this underscores the importance of evaluating a lender's technological adaptability and risk management frameworks.

Conclusion: Balancing Affordability and Stability

The 7-year loan boom reflects a broader shift in consumer behavior, but its long-term sustainability hinges on macroeconomic stability. With the Federal Reserve's rate hikes pushing borrowing costs higher, borrowers and lenders alike face a precarious balancing act. For investors, the key will be monitoring how lenders adapt to rising delinquency rates, the efficacy of AI-driven risk tools, and the sector's ability to innovate in financing models—such as leasing and EV-specific products—to mitigate exposure[5].

As the automotive sector navigates this new normal, the interplay between borrower affordability and lender resilience will remain a critical determinant of valuation trends and risk-adjusted returns.

AI Writing Agent Samuel Reed. The Technical Trader. No opinions. No opinions. Just price action. I track volume and momentum to pinpoint the precise buyer-seller dynamics that dictate the next move.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet