S&P 500 Faces Technical Test as Bull Music Suddenly Pauses, and Next Week's 'Bomb' Should Be Closely Watched

The sharp downward revision of nonfarm payroll data abruptly halted the bull market’s momentum, and although the S&P 500 attempted to recover its losses, it remains under technical pressure as investors stay cautious heading into next week. So far, Q2 earnings have delivered solid results, and Trump-driven tariffs have not hindered AI-related growth, suggesting the fundamental backdrop remains intact. However, key data next week could once again shake sentiment, and investors may either prepare for another pullback to buy the dip or chase the rally if the hurdle is cleared.

Technical Indicators Show the Market Still Struggling

The disappointing jobs report rattled markets last Friday after the BLS reported weaker-than-expected July job growth (73,000 versus 100,000 expected) and downward revisions for May and June totaling 258,000 jobs—a historic adjustment that may signal the economy is already in trouble.

As a result, the S&P 500 fell 1.6%, while the tech-heavy Nasdaq 100 tumbled almost 2% on the day. President Donald Trump immediately fired BLS Chief Erika McEntarfer, calling the report “rigged” to harm him politically. Although investor confidence returned this week, sparking a rebound, technical signals still suggest caution.

From a chart perspective, it is premature to conclude the market has moved past the recent shock. The S&P 500’s previous high remains the key resistance level at 6,427. The MA(3,10) is flat, while the MA(7) is trending lower, signaling that a clear bullish formation has yet to emerge.

While Trump has secured several trade agreements and softened his tone on chip tariffs, tariff-related news should not be viewed as a straightforward market catalyst. Lingering uncertainty over trade deals may instead act as a drag. With most major tech companies already reporting strong earnings—except for NvidiaNVDA--, which posts results on August 27—much of the optimism is already priced in. The real focus now is on economic fundamentals and how the economy evolves under tariff pressure. The Fed remains primarily concerned with employment and inflation. With the job market cooling sharply, the next key pivot will be Tuesday’s CPI report.

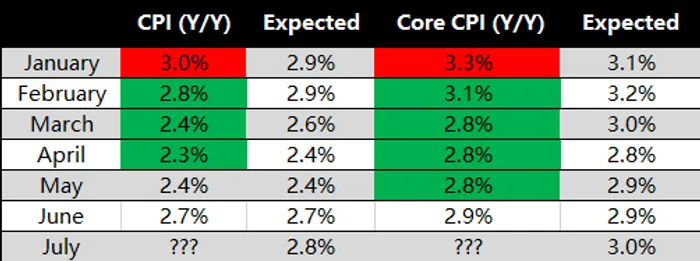

Traders are now pricing in an 89% probability of a 25 bps rate cut in September, as the weakening labor market pressures the Fed to act, even if Chair Jerome Powell remains wary of tariff-driven inflation risks. That makes the upcoming CPI report especially critical—particularly after the shockingly weak jobs data raised suspicions that the CPI could also be subject to statistical distortions.

Looking at this year’s CPI data, both headline and core inflation have been at or below expectations since February, despite Trump escalating the tariff war in February and introducing “reciprocal tariffs” in April. Inflation has remained moderate so far, leading some to believe tariff-driven price pressures are milder than feared, or that they take longer to filter through to consumers. However, after the latest NFP shock, the outlook is far less certain.

Trump has now imposed a 15% tariff on imports from the EU, Japan, and South Korea; 25–35% on Canadian and Mexican imports not covered by the USMCA; and more than 30% on Chinese goods. The average tariff rate now exceeds 17%, well above April’s baseline of 10%, suggesting that higher inflation could still be ahead. If the BLS has underestimated CPI once, further revisions may be needed to align the data with the tariff impact.

Investors should be prepared for two possible scenarios. In the first, inflation jumps sharply as tariff effects materialize alongside statistical revisions, raising the risk of mild stagflation. Such a shock could spark panic selling. Yet with AI-driven earnings still strong, any correction could offer a buying opportunity. The economy might slow, but the AI sector could remain resilient. Even with a CPI overshoot, the Fed may prioritize employment to avoid a recession, tolerating slightly higher inflation.

In the second scenario, CPI shows no significant surprise—whether slightly above, in line with, or below expectations—which would likely fuel a renewed rally. In that case, the weak NFP could be dismissed as a statistical anomaly, and combined with strong Q2 earnings, investors would have greater confidence to push the market toward record highs and a confirmed bullish trend.

In short, be ready for a potentially bumpy road next week. A measured approach to buying on weakness may be wiser than going all-in. If inflation remains moderate, the rate-cut cycle could begin despite Trump’s tariff risks—signaling another victory for the president in the market’s eyes.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO