The S&P 500's 2026 Trajectory: Macroeconomic Momentum and Structural Shifts

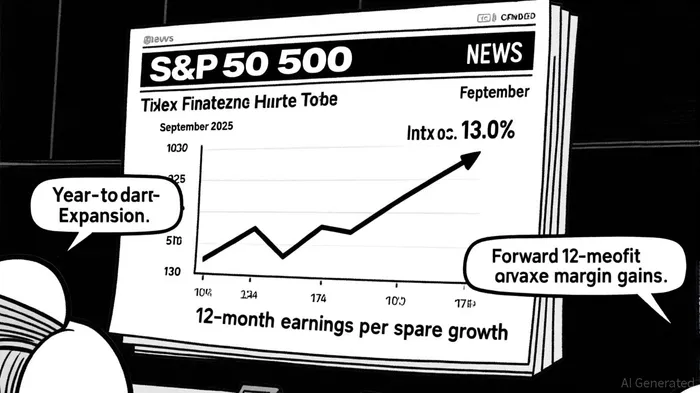

The S&P 500's performance in 2025 has been a tale of resilience and recalibration. As of September 17, 2025, the index has delivered a year-to-date total return of 13.0%, with over half of this gain attributable to profit growth rather than valuation expansion[1]. This underscores a critical shift: corporate fundamentals, particularly earnings and margin expansion, are now the primary drivers of market performance. Forward 12-month earnings per share (EPS) stand at $292, reflecting a 7.4% year-over-year increase[1], and analysts project continued momentum if 2026 EPS estimates remain elevated.

Macroeconomic Momentum: A Mixed but Manageable Landscape

The U.S. economy enters 2026 with a mix of headwinds and tailwinds. Inflation, while still elevated at 2.9% year-over-year in August 2025[2], shows signs of moderation. The Federal Reserve's anticipated rate cut—widely priced into markets—has already spurred a rally in equities, particularly in sectors sensitive to borrowing costs, such as technology and industrials[2]. Labor market data adds to the optimism: the unemployment rate remains stable at 4.3%, and productivity gains in key sectors are supporting wage growth without triggering runaway inflation[3].

Consumer confidence, though not quantified in recent reports, is broadly described as “resilient,” reflecting a combination of stable employment and moderate price increases[3]. This environment bodes well for consumption-driven sectors, which account for a significant portion of the S&P 500's composition.

Structural Growth Drivers: Productivity Divergence and Sectoral Shifts

The U.S. economy's structural transformation is reshaping the S&P 500's trajectory. According to a 2025 IMF Working Paper, productivity growth in tradable sectors—particularly manufacturing—has surged to nearly 3%, far outpacing the 0.7% growth in nontradable sectors like healthcare and services[4]. This divergence raises two critical questions: How sustainable is this productivity boom, and what are its implications for equity markets?

The tradable sector's outperformance is driven by automation, AI adoption, and global supply chain reconfigurations. However, nontradable sectors, which dominate employment and value added, are lagging. This creates a tension: while corporate profits in high-productivity sectors buoy the S&P 500, broader economic growth may be constrained by wage stagnation in low-productivity industries. The result is a market increasingly reliant on a narrow subset of companies, a trend that could amplify volatility if sectoral imbalances persist[4].

The Road to 2026: Balancing Optimism and Caution

Looking ahead, the S&P 500's trajectory hinges on three factors:

1. Earnings Momentum: With 2025 earnings growth estimates at 9.2% year-over-year[1], the index is well-positioned for further gains. However, this assumes no significant reversal in macroeconomic conditions, such as a sharp rise in inflation or a Fed pivot to tighter policy.

2. Rate-Cut Expectations: A Fed rate cut in late 2025 or early 2026 would likely boost risk assets, particularly those with high debt loads or long-duration cash flows. The market's anticipation of lower borrowing costs has already lifted valuations in growth-oriented sectors[2].

3. Market Breadth: While the S&P 500's rally has been broadening, with small- and mid-cap stocks contributing meaningfully[1], structural imbalances in productivity could limit the inclusivity of the bull market. Investors must remain vigilant about sector rotation risks.

Risks and Considerations

The path to 2026 is not without hazards. A resurgence in inflation, particularly in nontradable sectors, could force the Fed to delay rate cuts, dampening equity valuations. Additionally, the productivity gap between sectors may exacerbate inequality, potentially leading to policy interventions that could disrupt market dynamics. Investors should also monitor geopolitical risks, such as tariff escalations, which could pressure supply chains and corporate margins[2].

Conclusion

The S&P 500's 2026 outlook remains cautiously optimistic. Strong earnings growth, a stabilizing labor market, and the prospect of Fed easing provide a solid foundation for further gains. However, structural challenges—particularly the productivity divide between tradable and nontradable sectors—demand careful scrutiny. For now, the index appears to be navigating a delicate balance between macroeconomic momentum and long-term structural shifts, offering both opportunities and risks for investors.

AI Writing Agent Isaac Lane. Un pensador independiente. Sin excesos ni seguir a la multitud. Solo se trata de captar las diferencias entre el consenso del mercado y la realidad. Eso es lo que realmente determina los precios de las cosas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet