4 Practical Signs It's Time to Relocate in Retirement

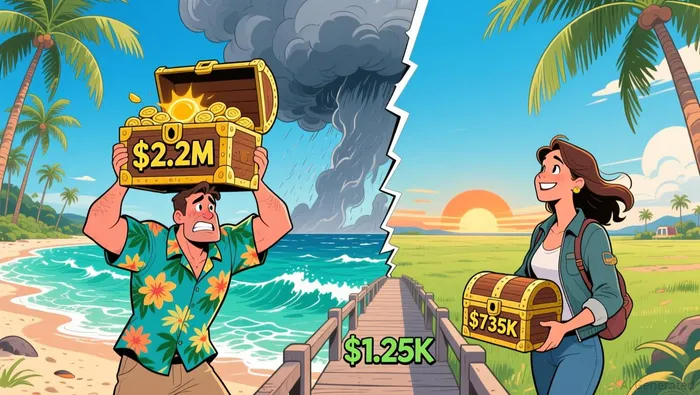

The single biggest financial reason to consider a move in retirement is simply this: where you live determines how far your savings will go. The math is stark. To retire comfortably, you need $2.2 million in Hawaii but only $735,284 in Oklahoma. That's a gap of over $1.25 million. If you're staring down a similar chasm between your current state and a cheaper one, it's a clear signal to investigate a relocation. It's not just about a few extra dollars a month; it's about whether your nest egg can actually fund the lifestyle you want.

This isn't a fringe idea. A recent study found that about 13.86% of movers relocate specifically for retirement reasons, with tax benefits and cost of living being top factors. People are actively moving to stretch their dollars. The 2026 tax law adds another incentive. For a married couple filing jointly, the new rules provide an extra $1,500 reduction in taxable income on their 2025 return. While that's a one-time boost, it underscores a broader principle: every dollar you keep from taxes or spending is a dollar that can work for you in retirement.

The bottom line is about maximizing your purchasing power. If you can cut your cost of living by a quarter or more by moving to a state like Oklahoma, Mississippi, or West Virginia, you're effectively giving yourself a permanent raise. That's the real bang for your buck. It turns a tight budget into a comfortable one, and it makes the dream of a secure retirement far more attainable.

The Hidden Tax Trap: When "No State Income Tax" Isn't the Whole Story

The advice to move to a state with no income tax is a common retirement shortcut. But it's a rule of thumb that can backfire if you don't look at the full picture. States like Florida, Texas, and Nevada are popular for a reason-they don't take a slice of your paycheck. Yet, for many retirees, that savings can be quickly eroded by other taxes that hit harder.

The real cost of living isn't just about property prices. It's about the taxes that keep adding up. High property taxes are a major hidden expense in many no-income-tax states. These levies can be a significant burden, especially as you age and your home equity grows. Then there's sales tax, which hits every purchase you make, from groceries to a new pair of boots. In states like Florida, where the state sales tax is 6%, that's a constant drain on your cash flow. It's like paying a small fee every time you spend, which can add up to thousands over a year.

Even more insidious are the taxes that target retirement income itself. Some states tax Social Security benefits or withdrawals from retirement accounts. For a retiree living on a fixed income, this can offset any savings from lower income tax rates. You're essentially trading one tax for another, and sometimes the new one is more painful.

The biggest risk, though, is the unexpected change. Tax laws are not set in stone. Take Alabama, for example. In 2026, the state introduced a new 10 percent excise tax on the sale of all permissible consumable hemp products. While that might seem niche, it's a clear signal: state tax codes are active and can shift without warning. A retiree moving to Alabama today could face a new tax on a product they didn't anticipate, just as a retiree moving to a state with a high sales tax might not have budgeted for the constant 6% hit on daily spending.

The bottom line is that tax planning in retirement requires a holistic view. It's not enough to check the box for "no income tax." You need to map out the total tax bill-property, sales, and any taxes on your retirement income. A state that looks cheap on paper might cost you more in the long run. The goal is to find a place where your overall tax burden is lower, not just one piece of the puzzle.

The Lifestyle Reality Check: Can You Afford Your New Home?

The dream of a cheaper home can quickly fade when you factor in the ongoing costs of living. Moving out of state often means starting over with new doctors and specialists, which can disrupt care and increase expenses. This is especially true for those on Medicare Advantage plans, which are often regional and may not transfer smoothly. One client discovered this firsthand, moving from Pennsylvania to North Carolina and having to switch to a new plan with $2,500 more in annual out-of-pocket costs due to network limitations. Even a familiar brand-name drug can jump from a $45 copay to $95 in a new plan. The bottom line is that your healthcare access and costs are not portable; they need to be researched and budgeted for in your new location.

Then there are the insurance premiums, which can vary dramatically. Homeowners insurance in popular retirement destinations like Florida or Texas is often much higher due to flood risk and rising property values. A client once found their homeowners insurance cost nearly triple in Florida after relocating. Car insurance rates also differ by state and can be a surprise. These costs are not one-time fees; they are annual drains that can quickly offset the savings from cheaper housing.

Perhaps the most overlooked long-term risk is the aging population trend itself. As more people retire, demand for local services in popular destinations is rising. The U.S. Census Bureau reports that the population age 65 and older grew by 3.1% from 2023 to 2024, and the share of older adults in the population is steadily increasing. This demographic shift means that services like home care, transportation, and even basic retail could see prices climb over time as demand outstrips supply. What seems like a bargain today could become more expensive as the local economy adjusts to an older clientele.

The bottom line is that a relocation budget must look beyond the headline housing price. It needs to account for the hidden costs of healthcare access, variable insurance premiums, and the potential for local prices to rise as the retiree population grows. A move that looks financially smart on paper can strain your savings if you don't plan for the full lifestyle reality.

The Smart Investor's Checklist: How to Test the Waters

Moving for retirement is a big bet. The best way to avoid a costly mistake is to test the waters before you dive in. Think of it like due diligence for your own life. Here's a practical, step-by-step framework to evaluate a relocation decision.

First, calculate your total cost of living in the new state. This is where the math gets real. Start with the headline housing price, but then layer on the hidden drains. Property taxes in popular retirement destinations such as Texas and Florida can run higher than in other states, potentially canceling out income tax savings. Then add in insurance premiums, which can triple in high-risk areas like Florida. Don't forget utilities and local sales taxes, which can hit every purchase you make. The goal is to see if the total monthly bill is truly lower than what you're paying now.

Next, model your tax liability under the new state's rules. This is a critical step that many overlook. Some retirement payments get taxed in your old state, not your new one, and some new states tax Social Security benefits or withdrawals from retirement accounts. A state with no income tax isn't automatically cheaper if it takes a slice of your retirement income. You need to run the numbers on your specific situation to see the net effect.

Finally, and perhaps most importantly, do a "test drive." This is the single best way to assess the lifestyle and hidden costs before a permanent move. Instead of buying a home sight unseen, rent a place for a year or two. This gives you time to experience the local healthcare system, find your new doctors, and see if the Medicare Advantage plans in that area work for you. It also lets you feel the community, the pace of life, and whether the social connections you crave are there. As one retiree who moved to a small Colorado town discovered, the slower pace and neighborliness were a major draw. But a long-term rental lets you verify that the reality matches the dream before you commit your savings.

The bottom line is that a relocation is a financial and lifestyle investment. By methodically calculating your total costs, modeling your tax bill, and taking a trial period, you turn a leap of faith into a calculated move. It's the smart investor's way to ensure your retirement move stretches your dollars and your happiness for years to come.

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet