3M Q1 Earnings: Strong Margins, Resilient Core, But Tariff Cloud Gathers

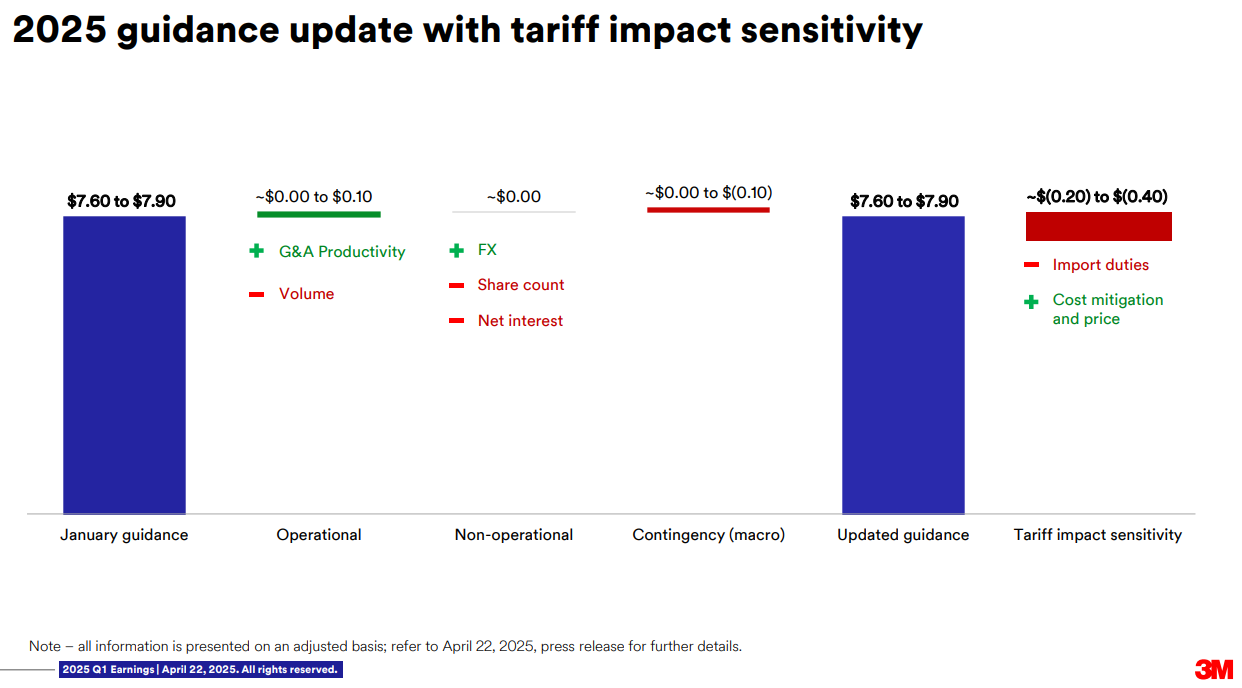

3M delivered a better-than-expected first quarter, with strength in margins and earnings despite modest sales headwinds. The company reported adjusted EPS of $1.88, beating estimates of $1.77, and revenue of $5.8 billion, narrowly topping forecasts despite being down significantly from the prior year’s $7.72 billion. Operating metrics were encouraging, with adjusted operating margins expanding 220 basis points to 23.5% year-over-year. While the quarter showed resilience, the real headline lies in 3M’s tariff warning: the company now expects a $0.20–$0.40 per share drag from new trade levies. This puts the stock at the center of market conversations around protectionism and global supply chain fragility.

Earnings growth was driven by a mix of operational discipline and favorable cost controls. GAAP EPS surged 61% to $2.04, aided by a $0.63 per share gain linked to Solventum’s ownership. Organic sales growth was modest at 1.5% year-over-year, but higher than feared given macro softness. Gains were driven by strong performance in electrical markets, industrial adhesives, and aerospace, partially offset by weakness in automotive and packaging-related categories. Despite top-line softness, 3M’s focus on productivity and lower restructuring costs translated into stronger margins across the board.

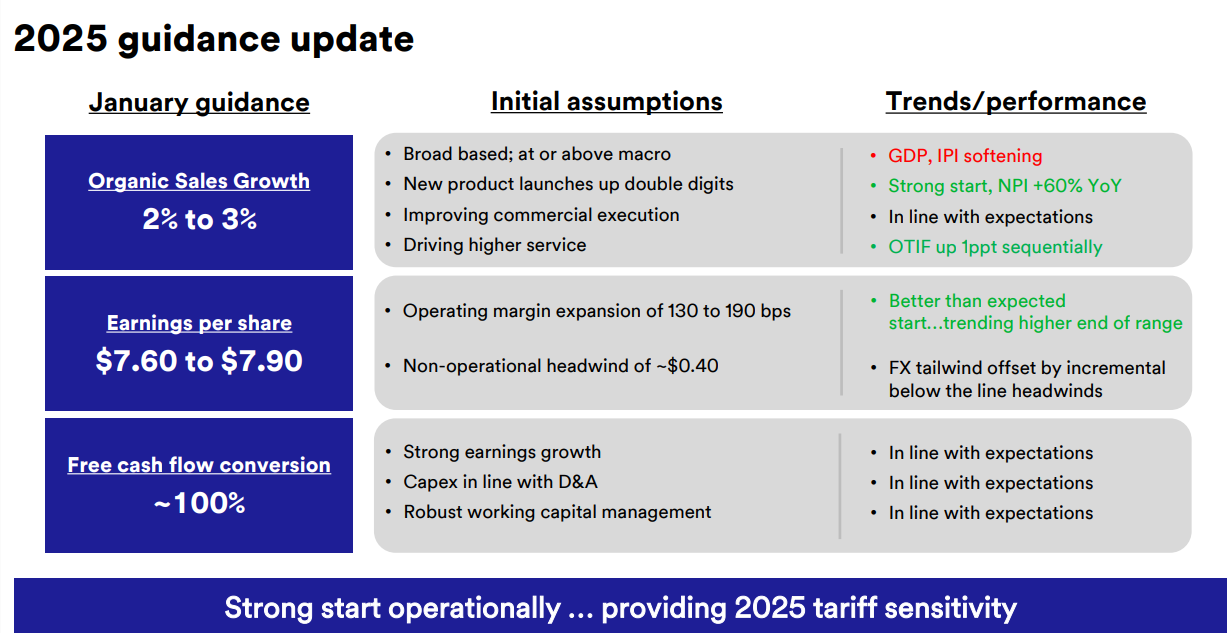

The company maintained its full-year adjusted EPS guidance of $7.60 to $7.90 but added a new wrinkle—an estimated $0.20 to $0.40 per share headwind tied to tariffs. Management highlighted that these costs stem from recently enacted U.S. and international duties on key inputs and components, with the precise impact dependent on future trade policy actions. This makes 3M one of the few multinationals quantifying tariff exposure in real-time, offering investors a critical window into how global industrial supply chains are absorbing the latest round of trade friction.

In practical terms, 3M’s tariff exposure is a byproduct of its vast international manufacturing network. With over 60,000 SKUs produced and sold globally—including high-value industrial, healthcare, and electronics inputs—many of 3M’s operations depend on raw materials and components sourced from China and other tariff-sensitive jurisdictions. That exposure spans both upstream cost pressure and downstream pricing dynamics. As a result, analysts view 3M as a tariff bellwether—akin to an economic pressure gauge for U.S. manufacturing policy. Its visibility into sourcing, logistics, and inventory costs makes its forecasts a de facto proxy for how U.S. industrials will absorb ongoing and potentially escalating trade actions under the Trump administration.

Aside from the tariff concerns, cash flow generation was mixed. Operating cash flow was slightly negative at $(0.1) billion, but adjusted free cash flow came in positive at $0.5 billion. The company returned $1.7 billion to shareholders during the quarter via dividends and buybacks, and it increased its full-year share repurchase target to $2 billion. The board’s $7.5 billion authorization reinforces long-term capital return confidence, even amid near-term headwinds.

In sum, 3M’s Q1 print offered operational reassurance, but it also served as a stark reminder of external risks now returning to the macro conversation. The company beat expectations and reaffirmed its outlook despite signaling that tariffs could shave up to 5% off 2025 EPS. For investors tracking the downstream consequences of trade war escalation, 3M is once again a name to watch—not just for its numbers, but for what it reveals about the industrial economy’s ability to absorb geopolitical shocks.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet