$31 Trillion Bond Market Pulls Brakes: Traders Shift to Moderate 25-Basis-Point Cut View

In the massive $31 trillion US bond market, fixed-income traders are quietly stepping back from the aggressive wagers that previously discarded expectations for Federal Reserve interest rate cuts for the entirety of 2026. Ahead of the crucial Federal Open Market Committee (FOMC) meeting this Wednesday, March 18, 2026, the narrative across trading desks is distinctly shifting from an extreme consensus of holding rates higher for longer to a much more moderate and balanced outlook. This significant pivot is largely driven by emerging vulnerabilities in macroeconomic growth, which are beginning to counteract the inflationary pressures sparked by recent geopolitical turmoil in the Middle East. From a market strategy perspective, my stance is that this recalibration is fundamentally positive for broad risk assets. It actively removes the immediate, suffocating threat of runaway short-end Treasury yields, which typically stifle equity valuations and increase corporate borrowing costs. Ultimately, the core thesis is that the market is currently digesting a necessary transition from extreme anxiety to a tempered reality, rather than simply debating the precise timing of a potential policy easing.

From Inflation Panics to Technical Unwinds

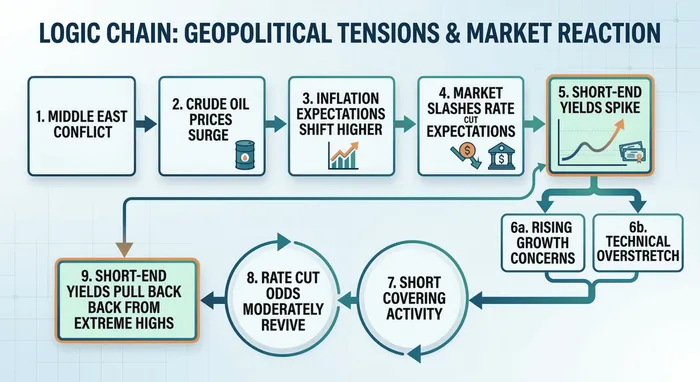

To properly contextualize the current market psychology, it is essential to trace the severe volatility observed over the past two weeks. Following the sudden escalation of the Middle East conflict, a firm consensus rapidly emerged across trading floors that the Federal Reserve would be paralyzed, unable to cut rates at all in the near future. As crude oil prices surged aggressively toward the $100 per barrel threshold on the Nymex, inflation anxieties were violently reignited. Futures traders responded by aggressively altering their positions, essentially abandoning any near-term monetary easing. However, this extreme positioning has reversed rapidly due to a potent combination of macroeconomic growth concerns and localized technical factors within the rates market. As the initial shock wore off, market participants began to question whether the dual burden of restrictive interest rates and elevated energy costs would eventually fracture economic output. These fears were compounded by a labor market that recently printed a surprising payroll decline in February, forcing growth risks to be aggressively embedded into the yield curve.

Furthermore, structural market mechanics have heavily amplified this reversal. Quantitative analysts at major institutions, including Morgan StanleyMS-- and RBC Capital Markets, have noted that the initial violent spike in short-end rates was heavily exaggerated by positioning pain and forced deleveraging. Leveraged long positions were squeezed, forcing rapid liquidations, while demand for hedging instruments spiked artificially.

According to Ainvest analysis, as clearly mapped out in the visual logic chain detailing geopolitical tensions and market reactions, the current pullback in short-end yields from their extreme highs is heavily driven by these technical unwinds. For example, specific Secured Overnight Financing Rate (SOFR) put options, which were placed earlier this year to bet on rising short-end yields, generated approximately $10 million in paper profits. The subsequent liquidation and profit-taking on these exact derivative positions have directly catalyzed the recent decline in Treasury yields. By unwinding these hawkish hedges, the market has naturally transitioned from a state of panic back to a more balanced baseline, relieving upward pressure on borrowing costs.

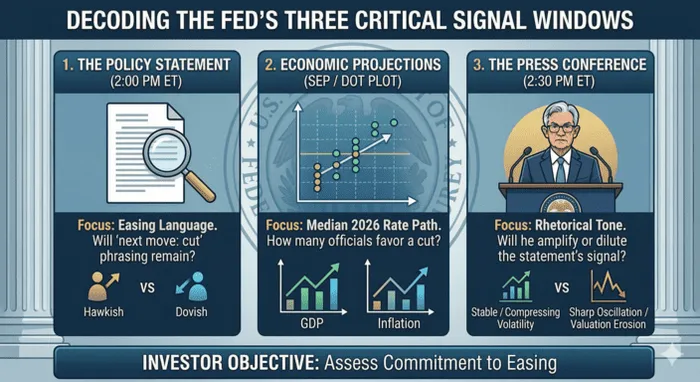

Decoding the Fed's Three Critical Signal Windows

For equity and fixed-income investors alike, Wednesday’s FOMC event is less about the immediate baseline rate decision—which is widely expected to hold steady in a range of 3.5% to 3.75% —and entirely about forward-looking communication. Referencing the analytical framework recently highlighted by Nick Timiraos at The Wall Street Journal, the focus has shifted from predicting the exact date of a cut to assessing whether officials can maintain their commitment to any easing cycle at all. This presents three primary windows for investors to monitor:

- The Policy Statement: During the January meeting, a minority of officials pushed to remove language suggesting the next move would be a cut. If this alteration occurs now, it will serve as a definitive, highly hawkish signal that the easing cycle has concluded.

- The Summary of Economic Projections (SEP): This matrix, specifically the dot plot, will quantify the collective judgment of the 19 officials regarding the inflation trend and the 2026 rate path. It serves as an important quantitative benchmark for measuring changes in policy leanings.

- The Press Conference: Chair Jerome Powell’s post-meeting rhetorical choices can either amplify or dilute the structural signals derived from the statement and the dot plot.

To safely approach this complex environment, market participants should utilize a disciplined, step-by-step checklist:

- Pre-Meeting Baseline: Prior to the meeting, investors must verify implied rate cuts via fed funds futures to establish a mental baseline. Currently, the market shifted back to pricing at least one quarter-point cut by the end of 2026.

- The 24-Hour Post-Meeting Window: Observe whether short-end Treasury yields undergo a significant upward adjustment post-release. Check if the median dot plot shifts higher than previous iterations. Additionally, it is crucial to parse whether the overarching narrative from institutional research desks interprets the Fed's collective messaging as hawkishly dovish or dovishly hawkish.

- The Subsequent Two Weeks: Closely monitor incoming inflation and employment data to see if macroeconomic reality validates the central bank's stance. If economic data continues to print weaker than expected, there is substantial room for today's moderate expectations to shift further dovish. Conversely, robust data could thrust the narrative forcefully back to the previous extremes, shocking equity valuations.

Conclusion

In conclusion, this market dynamic corrects extreme pessimism; it is not the start of an aggressive rate-cut bull market. With swaps pricing just one 25-basis-point reduction by late 2026, valuation anchors are only slightly loosening. For equities, stable expectations matter more than predicting the exact month of a policy shift. Consistent Fed messaging will compress volatility, while erratic guidance will quickly erode valuation premiums. However, the Middle East conflict remains the dominant black swan risk. If escalating war sustains oil prices near $100 a barrel, today's painstakingly rebuilt, moderate rate-cut expectations could be entirely erased.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet