2025 Market Outlook: Key Investment Themes to Watch for the Year Ahead

As 2024 draws to a close, markets are set to finish another strong year of gains, with the S&P 500 poised to post its second consecutive 20%+ return. This resilience has persisted through a turbulent election season and divisive rhetoric from both political sides, underscoring the strength of the market's momentum.

The Federal Reserve's progress against inflation has finally led to the beginning of a rate-cutting cycle, though fiscal policies under the new administration have raised fresh concerns about potential inflationary pressures on the horizon.

The AI-driven rally remains one of the most dominant forces in the market, with Nvidia continuing its leadership as one of the year's top-performing stocks. As more companies begin to monetize their AI capabilities and leverage these technologies for productivity gains, AI is expected to fuel sustained growth in the coming year. However, valuations remain elevated, with the S&P 500 trading at approximately 22.3 times forward earnings for 2025, suggesting that equities may be extended at current levels.

While some draw comparisons to the market rally following the 2016 election, the economic and market conditions today are significantly different. In 2016, valuations were lower, corporate tax rates had substantial room to fall, and 10-year yields were more than 200 basis points lower than current levels. Additionally, the U.S. fiscal landscape has evolved, with limited capacity for significant deficit expansion given the current state of the balance sheet. This more constrained environment presents unique challenges as we look ahead to the new year.

Against this backdrop, we turn our focus to 2025 and the key themes expected to shape the market's trajectory. Over the coming weeks, we will explore critical drivers, potential headwinds, and areas of opportunity for investors. This multi-part series aims to provide insights on the economic, policy, and sector-specific trends that will impact markets and present opportunities in the year ahead.

Can the S&P Rally 20% for a third Consecutive year?

The past two years have been impressive for the U.S. stock market, with 2023 and 2024 delivering consecutive periods of notable gains across all major indices. In 2023, the S&P 500 surged over 24%, buoyed by economic resilience and easing inflation, while the Dow Jones climbed 16.1%, and the Nasdaq jumped an extraordinary 55.1%, marking its best performance since the late 1990s. Small-cap stocks also performed well, with the Russell 2000 gaining 16.7%. As of late 2024, markets continued this upward momentum, with the S&P 500 up 25.45% year-to-date, the Dow Jones up 16.51%, the Nasdaq up 28.5%, and the Russell 2000 rising by 18.4%. This robust performance has led investors to wonder whether a third consecutive year of gains could be possible in 2025.

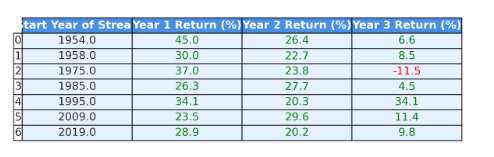

Historically, after two years of 20%+ gains, the S&P 500 has generally posted a positive return in the third year, though these gains are often more modest. On average, the market tends to deliver single-digit returns in the third year following two strong years, reflecting a slower, tempered pace. This pattern suggests that while there's potential for a positive year in 2025, the gains may not match the explosive returns seen in 2023 and 2024. Investors typically begin to take a more cautious approach in the third year, especially as overvaluation concerns and the potential for corrections arise.

Volatility also tends to increase in the third year of a rally cycle. With higher valuations, markets become more vulnerable to fluctuations driven by external factors, such as Federal Reserve policy shifts, economic cycle changes, and shifts in investor sentiment. Historically, in cases like the early 1980s and late 1990s, these third-year gains ranged between 5% and 10%, demonstrating that while gains were achievable, they were often accompanied by greater volatility and intermittent pullbacks.

Looking ahead to 2025, while history indicates the possibility for continued upward movement, the market is likely to encounter additional headwinds and moderate gains. Economic fundamentals, interest rates, and earnings growth expectations will play crucial roles in shaping performance. Investors will need to remain vigilant, as broader market conditions and valuation concerns suggest that while gains may be possible, they're less likely to be as substantial or steady as those seen over the past two years.

First Term Presidents and Trump 2016-17 Recap

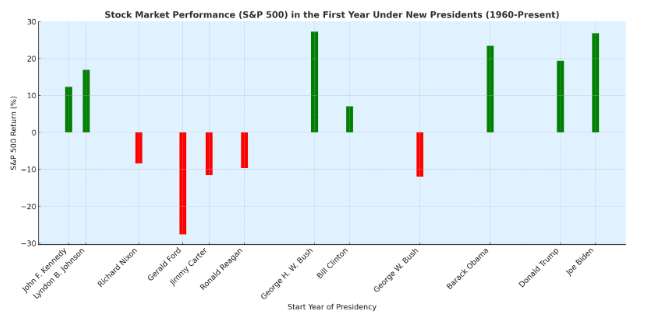

Historically, U.S. stock markets tend to perform positively during the first year of a new presidential administration. The four major indices—the S&P 500, Dow Jones Industrial Average, Nasdaq Composite, and Russell 2000—typically benefit from policy shifts and economic optimism. The S&P 500 has historically averaged returns of 6-10% in the first year, while the Dow Jones, closely following large-cap performance, usually gains around 6-8%. The Nasdaq, often influenced by tech-friendly policies or low-interest rate environments, averages a stronger 10-15% in the first year of an administration. Meanwhile, the Russell 2000, reflecting optimism among small-cap, domestic-oriented stocks, has historically shown average gains of 8-12%.

First-year market performance under a new administration often hinges on pro-growth fiscal policies, such as stimulus initiatives, tax cuts, or regulatory changes. These policies can boost sentiment, especially when they involve sectors heavily affected by governmental decisions, such as energy, industrials, and financials. However, the first year can also bring volatility, with markets reacting to economic uncertainties or policy shifts, as well as any surprises in fiscal or monetary approaches. Broader economic conditions, such as inflation and Federal Reserve policies, also heavily influence market performance in the first year.

The market's response to the start of President Trump's administration in late 2016 and early 2017 exemplified this first-year optimism. From November 2016 through April 2017, the S&P 500 rose roughly 12%, driven by expectations of corporate tax cuts and deregulation. The Dow Jones climbed 14%, led by financial, industrial, and energy stocks in anticipation of relaxed regulations and potential infrastructure investments. The tech-focused Nasdaq surged 16%, reflecting positive sentiment around tech and growth sectors. Meanwhile, the Russell 2000, with its high domestic exposure, gained 17%, as small-cap stocks rallied on the expected economic boost from tax reform and deregulation.

Key policy expectations played a pivotal role in supporting these gains. The Trump administration's plans for corporate tax reform sparked optimism, even though the tax cuts were not officially enacted until December 2017. The anticipated reduction of the corporate tax rate from 35% to around 15-20% created a powerful tailwind for stocks, with investors pricing in the potential impact on corporate earnings. Additionally, Trump's promises to reduce regulatory burdens on sectors like financials and energy led to significant rallies in these areas, as investors anticipated a more business-friendly regulatory environment.

Infrastructure spending promises further supported industrial stocks, although an official infrastructure bill was not immediately passed. Additionally, the administration's pledge to roll back Dodd-Frank regulations fueled gains in financial stocks, with banks expecting fewer regulatory constraints on lending and capital requirements. This policy-driven optimism generated strong momentum for U.S. equities in late 2016 and early 2017, setting a positive tone for Trump's first year in office and underscoring how fiscal policy expectations can impact early market performance in a presidential term.

Conclusion

While the significant rallies of 2023 and 2024 might raise concerns about hitting a market peak, historical patterns suggest that strong consecutive years don't necessarily signal the end of a bull run. In fact, the S&P 500 has shown resilience, often extending gains into a third year, albeit at a more moderate pace. Historically, the third year following two consecutive years of 20%+ gains tends to produce single-digit returns, suggesting that while 2025 could remain positive, gains may be tempered by factors such as higher valuations and cautious investor sentiment. The potential for increased volatility, corrections, and external influences—like Federal Reserve policy and economic cycles—indicates a more complex, albeit positive, outlook.

Moreover, markets have often benefited from optimism during the first year of a new administration. Historically, first-year gains have been fueled by policy expectations around tax cuts, regulatory adjustments, and fiscal stimulus, creating a favorable environment for equities. Trump's initial months in office in 2016-2017 saw a similar pattern, as the market rallied on promises of corporate tax reform, deregulation, and infrastructure investment. However, the current economic landscape is markedly different, and this could temper investor enthusiasm heading into 2025. Elevated valuations, differing fiscal capacities, and the lingering effects of inflationary pressures may make investors more cautious than in previous cycles, setting up a unique environment as we approach the new year.

2025 Key Themes

In the coming weeks, we'll explore a list of key themes that are set to shape the markets in 2025. We'll dive deeper into each situation, analyzing the potential opportunities and challenges for various plays depending on how these themes unfold.

Yield Curve Inversions

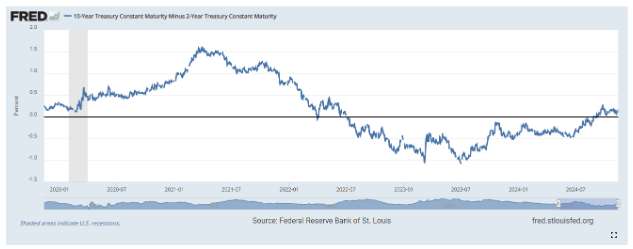

As 2025 begins, the longest yield curve inversion in U.S. history has ended, with the two- and ten-year Treasury spread returning to positive territory. This shift is being driven by bull steepening, as short-term yields fall more sharply than long-term yields amid expectations of imminent Federal Reserve rate cuts. A similar trend is observed in German Bunds, though the steepening there is expected to be more moderate. The Federal Reserve and the European Central Bank are both anticipated to cut rates multiple times through 2025, potentially supporting a gradual economic soft landing. However, while disinversions have historically preceded recessions, analysts see only a 38% recession probability in the U.S., expecting yields to rise slightly over the next year. This environment may favor investments in short- to medium-term maturities, as these are historically well-positioned to benefit from curve normalization and initial rate cuts.

Crypto Surge

Crypto is set to be a major theme in 2025, with Bitcoin fast approaching the once-unthinkable $100,000 mark, driven by growing institutional acceptance and the recent support from the GOP and Trump. The approval of Bitcoin and Ethereum ETFs in the U.S. has shifted investor perception, attracting both institutional and retail inflows, and setting the stage for broader adoption. While the recent rally has softened, the supply-demand dynamics remain favorable, and global monetary easing could act as a catalyst for further gains. As blockchain applications continue to expand in areas like decentralized finance and NFTs, and as regulatory clarity improves, the potential for crypto as a portfolio component is becoming increasingly compelling, though volatility remains a key consideration for investors.

Can AI Growth Continue?

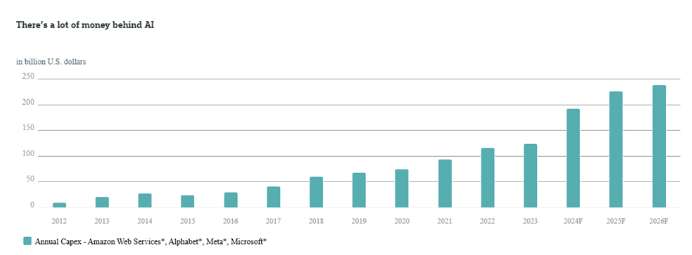

AI is expected to remain a key market driver in 2025, with companies in the Mag7 group, which have high AI exposure, already contributing significantly to the S&P 500's growth and earnings. AI investment is expanding beyond tech giants to other industries, with sectors like pharmaceuticals, consumer goods, and industrials increasingly incorporating AI for operational efficiency and innovation. However, regulatory oversight, data security concerns, and high operational costs could slow the rapid growth of AI. Despite these challenges, the momentum in AI is likely to continue, supported by the substantial financial resources of major companies aiming for leadership in the field. This dynamic environment presents opportunities but requires careful stock selection to navigate the risks inherent in early-stage technology adoption.

Will Commodities Breakout?

The potential for a commodity supercycle is a growing theme, driven by the global energy transition and infrastructure demands that could push commodity prices higher for an extended period. Historically, supercycles are marked by prolonged price increases due to structural shifts in demand and limited supply growth. Current trends, such as the rising need for metals like copper and lithium for renewable energy and electric vehicles, indicate that a similar cycle may be on the horizon. China's decarbonization goals and its leadership in electric vehicle adoption are set to fuel demand, while policy initiatives in the U.S. and Europe focus on securing access to critical resources. For investors, the commodity sector offers diverse opportunities across energy, metals, agriculture, and renewable energy resources, though careful stock and ETF selection is advised to capture potential long-term gains in a dynamic market environment.

Trade Wars 2.0

A potential trade war between the U.S. and China is emerging as a critical theme for 2025, fueled by President-elect Trump's aggressive stance on tariffs and trade restrictions. Trump has hinted at imposing a 60% tariff on Chinese goods, with further measures that could severely disrupt U.S.-China economic relations and global supply chains. This raises concerns about a response from Beijing, including a significant devaluation of the yuan to offset U.S. tariffs and protect Chinese exports, a move that could destabilize financial markets. China faces economic challenges, including a property crisis, youth unemployment, and slowing export demand, and these new trade pressures could exacerbate its vulnerabilities. Additionally, Trump's team of advisors, including policy hawks like Robert Lighthizer, signals a potentially more intense trade conflict that could extend beyond China to impact other Asian economies. The outcome of this escalating tension could influence global markets and economic stability, making it a key theme to watch in the coming year.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO