Xior Student Housing: A Compelling Case for Re-Rating in Europe's Undervalued PBSA Sector

The European Purpose-Built Student Accommodation (PBSA) sector is undergoing a structural transformation, driven by a perfect storm of demographic tailwinds, institutional capital inflows, and chronic supply shortages. At the heart of this evolution sits Xior Student Housing, a company whose improving fundamentals and sector-leading yields position it as a prime candidate for a re-rating. With a forward P/E ratio of 12.96 and a dividend yield of 6.02%, Xior appears significantly undervalued relative to its peers and the sector's long-term growth trajectory, according to Stockanalysis statistics.

Structural Tailwinds Powering the PBSA Sector

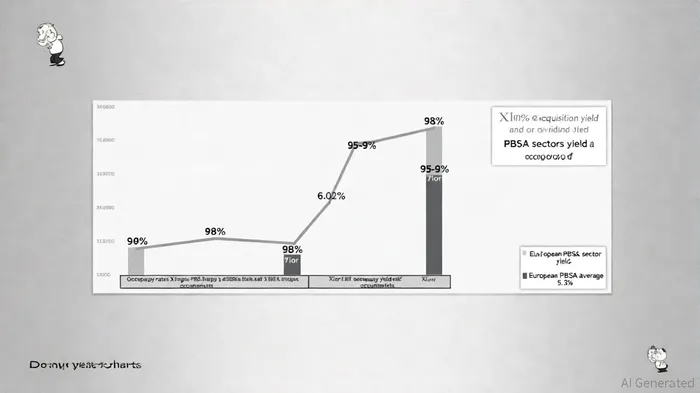

The PBSA sector's resilience stems from its unique alignment with macroeconomic and demographic forces. According to a JLL report, European student housing rents grew by 6.5% in 2023 and 5.4% in 2024, outpacing inflation in 10 of 15 surveyed countries. This trend is underpinned by a persistent undersupply of housing in key cities: provision rates-the ratio of new units to student populations-remain below 20% in Germany, France, and the UK, and as low as 10% in Italy, per Bonard analysis. Meanwhile, international student enrollment is surging, with cities like Warsaw and Amsterdam reporting occupancy rates below 2% vacancy, as noted in a BusinessResearchInsights report.

Institutional investors are taking notice. A Cushman & Wakefield survey found that 75% of European real estate investors plan to increase their PBSA exposure over the next three years, attracted by its stable cash flows and regulatory advantages compared to traditional residential markets. This growing demand for PBSA as a core-plus asset class has pushed average initial yields in prime markets to 5.3%, yet Xior's recent acquisition of 900 units in Poland delivered a gross yield of 10.5%, according to an Investing.com article.

Xior's Fundamentals: A Recipe for Re-Rating

Xior's outperformance is not accidental but the result of disciplined capital allocation and operational excellence. In H1 2025, the company reported 5.36% like-for-like rental growth and maintained a 98% occupancy rate, even as it raised prices, as shown in the Marketscreener presentation. That presentation also highlighted stronger liquidity-sufficient to cover financing needs for 18 months-and a modest reduction in loan-to-value (LTV) ratios to 49.84% from 50.99% in 2024.

The company's capital recycling strategy further enhances its appeal. By divesting non-strategic assets and reinvesting in high-yield markets like Poland and the Netherlands, Xior is compounding value at scale. Its active pipeline of 1,500 units, set to be delivered by 2026, will drive earnings growth in cities with proven demand, such as Amsterdam and Porto (details summarized in the Marketscreener presentation).

Valuation metrics underscore the case for re-rating. While Xior trades at a P/E of 22.3x, its European PBSA peers average 11.6x, per SimplyWallSt valuation. Analysts argue this disconnect is unsustainable: Xior's 6.02% dividend yield and 18.3% projected EPS growth rate are highlighted in Yahoo Finance analysis, and SimplyWallSt's forward-looking model also reflects the company's rare combination of income and growth in a sector where most operators trade at discounts to intrinsic value (see SimplyWallSt's future outlook).

Risks and Catalysts

Xior is not without risks. Rising construction costs and interest rate uncertainty could pressure margins, and regulatory shifts in zoning laws may delay developments. However, these challenges are sector-wide and do not detract from Xior's relative strengths. The company's low leverage, high-yield acquisitions, and sticky occupancy rates provide a buffer against macroeconomic headwinds.

The key catalyst for re-rating lies in the convergence of undervaluation and sector momentum. With the European PBSA market projected to grow at a 10.09% CAGR through 2030 (per the BusinessResearchInsights report cited above), and Xior trading at a 20% discount to estimated fair value (€36.63 vs current €29.05) according to SimplyWallSt valuation, the stock offers asymmetric upside.

Conclusion

Xior Student Housing embodies the intersection of a high-conviction sector and a compelling valuation. Its ability to generate sector-leading yields, coupled with a robust balance sheet and an active growth pipeline, positions it to outperform as institutional capital continues to flock to PBSA. For investors seeking exposure to a structural growth story with immediate income and re-rating potential, Xior offers a rare and well-sourced opportunity.

Comentarios

Aún no hay comentarios