New World Development's Liquidity Crisis: Strategic Asset Sales and Financing Talks as a Catalyst for Value Unlocking

Hong Kong-listed property developer New World Development (00017.HK) has long been a bellwether for the city's real estate sector. However, its recent liquidity crisis has thrust the Cheng family-controlled firm into the spotlight, with strategic asset sales and financing discussions with global heavyweights like Blackstone Inc.BX-- and CapitaLand Group sparking debates about its potential for value unlocking. For investors, the question is whether these moves signal a turning point or a precarious gamble in a sector still reeling from broader market downturns.

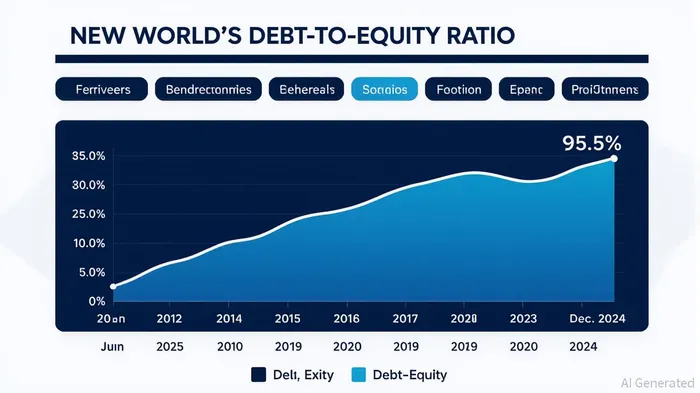

The Debt Overhang and Refinancing Lifeline

New World's debt burden remains staggering, with net debt reaching 95.5% of shareholders' equity as of December 2024. This placed the company on a knife's edge, particularly after it reported its first annual loss in 20 years for the fiscal year ending June 2024. A critical pivot came in June 2025, when the firm secured an $11.2 billion refinancing package from over 50 banks—the largest of its kind in Hong Kong. This deal, backed by prime assets like New World Tower and Victoria Dockside, temporarily averted a crisis and restored some investor confidence.

Yet, refinancing alone is insufficient. The company's attempts to secure a HK$15.6 billion loan led by Deutsche BankDB-- missed a self-imposed deadline, underscoring lingering liquidity challenges. To bridge the gap, New World has aggressively pursued asset sales, including its 11 Skies airport mall and mainland China properties. These divestitures, though potentially dilutive to earnings, are critical for deleveraging and stabilizing cash flows.

Blackstone and CapitaLand: A Strategic Inflection Point?

The most tantalizing development has been the rumored $2.5 billion investment from BlackstoneBX--, potentially in partnership with the Cheng family. While New World has denied formal offers, the mere speculation triggered a 20% single-day surge in its shares and a 2-cent jump in its 4.5% notes due 2030.

A Blackstone-led investment could provide the capital firepower to accelerate asset sales, refinance high-cost debt, and stabilize operations. The firm's expertise in restructuring distressed assets—evidenced in past deals like its $10.3 billion takeover of Hilton Hotels—suggests a strategic fit. However, risks loom. A privatization would reduce transparency, potentially alienating bondholders and institutional investors who rely on public disclosures to assess risk.

CapitaLand's involvement adds another layer. The Singaporean firm's interest in New World's assets, particularly its mainland China properties, hints at a broader trend of cross-border capital seeking undervalued real estate. Yet, CapitaLand's own exposure to Asia's slowing property markets raises questions about its appetite for a large-scale investment.

Risk-Reward Dynamics for Investors

For long-term investors, New World's situation presents a high-risk, high-reward proposition. The company's deleveraging strategy—combining asset sales, refinancing, and potential private equity backing—could reshape its balance sheet from a debt-laden entity to a leaner, more sustainable business. However, execution risks are significant.

- Asset Sales: Selling high-value properties like 11 Skies at a loss could erode shareholder value if not timed correctly. The success of joint ventures, such as Deep Water Pavilia's HK$26 billion sales target, will be critical.

- Financing Execution: Delays in securing the Deutsche Bank loan or Blackstone's investment could reignite liquidity concerns.

- Market Conditions: Hong Kong's property market remains fragile, with demand for luxury assets like Victoria Dockside dependent on global economic stability.

Is This a Buying Opportunity?

The answer hinges on three factors:

- Debt Reduction Progress: If New World can reduce its net debt-to-equity ratio to below 70% within 18 months, the risk profile will improve materially.

- Blackstone's Involvement: A confirmed investment would signal institutional confidence, potentially unlocking a premium for shareholders.

- Asset Sale Efficiency: Successful monetization of non-core assets without sacrificing long-term growth potential will be key.

For resilient investors, the current valuation—trading at a 50% discount to net asset value—offers a compelling entry point. However, patience is essential. The company's recent refinancing and asset sales have bought time, but the path to recovery is far from guaranteed.

Conclusion

New World Development's liquidity crisis is a microcosm of the broader challenges facing Asia's property sector. While strategic asset sales and financing talks with Blackstone and CapitaLand provide a lifeline, the company's success will depend on its ability to execute its deleveraging plan without compromising its core assets. For investors willing to navigate the volatility, this could represent a rare opportunity to capitalize on a restructuring story with significant upside—if the pieces fall into place.

In the end, the market will judge whether New World's gamble pays off. For now, the ball is in the court of the Cheng family, Blackstone, and CapitaLand to turn the tide.

Comentarios

Aún no hay comentarios