Wintrust Financial's Q3 Earnings: A Blueprint for Long-Term Value in a Challenging Sector

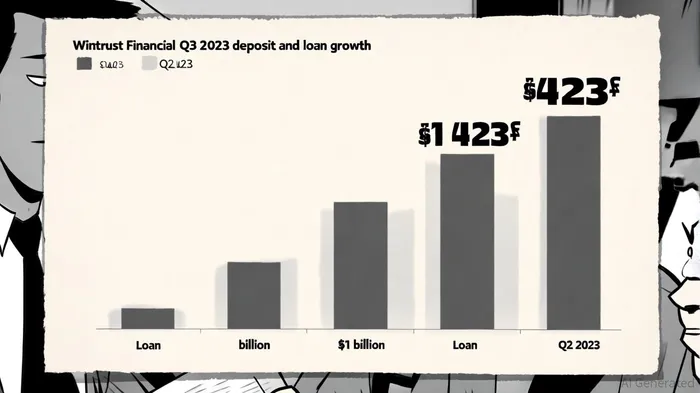

Wintrust Financial Corporation (NASDAQ:WTFC) delivered a standout performance in Q3 2023, reporting record net income of $164.2 million-a 14% increase compared to the same period in 2022, according to MarketBeat's peer data. This growth was fueled by robust deposit and loan expansion, with total deposits rising by $1 billion (9% annualized) and loans increasing by $423 million (4% annualized) after adjusting for a loan sale transaction, per a Wintrust press release. These figures underscore Wintrust's ability to capitalize on its regional banking footprint while navigating a sector marked by rising costs and economic uncertainty.

Profitability and Balance Sheet Strength

Wintrust's net interest margin (NIM) remained stable at 3.62%, a critical achievement in an environment where many regional banks have seen margins compressed due to aggressive deposit rate hikes, according to the Q3 earnings report. The company's disciplined approach-leveraging interest-rate hedges and a loan portfolio that reprices within a year-has insulated it from market volatility, as noted in MarketBeat's peer data. This stability is further reflected in its record net interest income of $462.4 million, driven by a diversified fee business that generated $112.5 million in non-interest income despite a weak mortgage market, as detailed in the WintrustWTFC-- press release.

The company's balance sheet growth is equally compelling. Total assets surged by $1.3 billion during the quarter, supported by a shift away from brokered funding and a focus on organic deposit growth, per the Wintrust press release. Non-interest-bearing deposits stabilized at $10.6 billion in average balances, a testament to Wintrust's customer-centric strategy highlighted in MarketBeat's peer data. Such metrics suggest a sustainable model that prioritizes long-term relationships over short-term liquidity gambles.

Credit Quality and Risk Management

Wintrust's credit quality remains a standout strength. Nonperforming loans stood at just 32 basis points, well below industry averages reported in MarketBeat's peer data. The company's proactive approach to commercial real estate (CRE) risk-highlighted by comprehensive stress testing and disciplined underwriting-has positioned it to weather potential downturns, as noted in a CNN analysis. This is particularly relevant as regional banks face heightened scrutiny over CRE exposure, with many peers increasing provisions for credit losses in Q3.

Competitive Positioning and Valuation

Wintrust's performance outpaces its regional banking peers on multiple metrics. Its return on equity (ROE) of 12.08% exceeds Ameris Bancorp's 9.57%, while its 12-month stock return of 34.14% outperforms the 24.6% growth of Ameris Bancorp, according to MarketBeat's peer data. Analysts have set a consensus price target of $147.31 for Wintrust, implying a 6.23% upside, compared to a potential downside for Ameris Bancorp, per MarketBeat's peer data. This optimism is reflected in institutional ownership, with 93.5% of shares held by large investors, signaling confidence in its long-term trajectory, as shown in MarketBeat's peer data.

Sector Challenges and Wintrust's Resilience

Regional banks broadly face headwinds, including rising deposit costs and the need to bolster credit loss reserves, as covered by CNN. Wintrust, however, has mitigated these pressures through strategic pricing and a focus on high-quality loans. Its ability to maintain stable margins and grow assets in this environment positions it as a rare winner in a sector where peers like PNC have resorted to cost-cutting measures such as workforce reductions, noted in the same CNN coverage.

Outlook and Strategic Momentum

Management's guidance for mid- to high-single-digit loan and deposit growth in Q4, coupled with stable margins and earnings momentum into 2024, reinforces the company's long-term appeal, according to MarketBeat's peer data. With a P/E ratio of 13.12 and a dividend yield of 1.43%, Wintrust offers an attractive valuation relative to its peers, per MarketBeat's peer data. Historical data from 14 earnings-release events between 2022 and 2025 reveals that WTFC's stock exhibited a weak directional bias, with average cumulative returns fluctuating within ±1% over 30-day windows and a win rate hovering around 50%, as shown in the WTFC backtest. These findings suggest that short-term trading around earnings dates lacks reliability, further emphasizing the merits of a long-term buy-and-hold strategy for investors seeking to capitalize on Wintrust's disciplined risk management, asset diversification, and operational efficiency.

Comentarios

Aún no hay comentarios