Western Midstream's Attractive 9.6% Yield and Strong Risk-Adjusted Returns

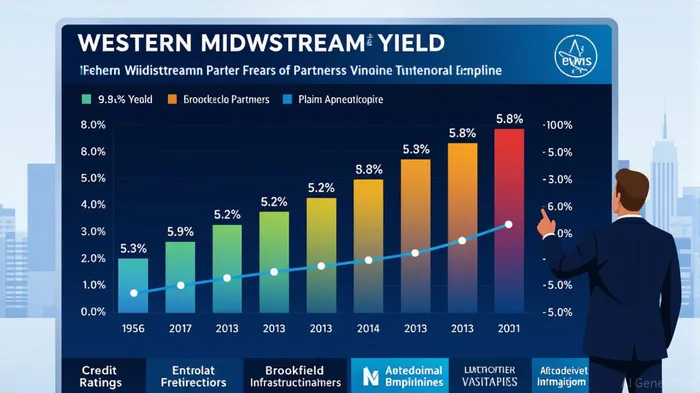

Master Limited Partnerships (MLPs) have long been a cornerstone for income-focused investors, but few offer the compelling combination of yield and risk mitigation seen in Western Midstream (WES). As of September 2025, WES boasts a forward yield of approximately 9.8%, significantly outpacing peers like Enterprise Products PartnersEPD-- (EPD) at 6.9% and Plains All American PipelinePAA-- (PAA) at 5.8% [4]. This high yield is not merely a function of aggressive payout policies but is underpinned by a robust operational and financial profile that positions the company as a standout in the midstream sector.

A High-Yield MLP with Investment-Grade Stability

Western Midstream's appeal lies in its ability to deliver exceptional returns while maintaining a conservative balance sheet. The company's leverage ratio of 3.0x net debt to EBITDA aligns with its BBB- credit rating, a level that ensures access to capital at favorable rates without overexposing the business to refinancing risks [4]. This is particularly notable when compared to peers like PAA, which also maintains a 3.0x leverage ratio but lacks the same level of yield differentiation [1].

The company's fee-based business model further insulates it from commodity price volatility. Over 90% of its cash flows derive from fixed-fee contracts, ensuring predictable earnings even in uncertain markets [2]. Strategic projects like the Pathfinder Pipeline—which enhances water-handling capacity in the Delaware Basin—underscore WES's commitment to growth without sacrificing financial discipline [2]. These factors contribute to a risk-adjusted return profile that rivals, if not exceeds, that of investment-grade MLPs with lower yields.

Yield-to-Risk Comparison with Peers

To evaluate WES's superiority, consider its peers:

- Enterprise Products Partners (EPD), with an S&P rating of A- and a yield of 6.9%, offers greater credit safety but at the cost of significantly lower returns [3]. Its 30-day historical volatility of 0.0854 suggests moderate price stability, yet its yield lags WES by over 300 basis points [5].

- Brookfield Infrastructure Partners (BIP), rated BBB by S&P, provides a 5.2% yield and a beta of 0.81, indicating lower market sensitivity [4]. However, its diversified infrastructure portfolio comes with diluted exposure to high-margin midstream assets.

- Plains All American Pipeline (PAA), with a BBB- rating and 5.8% yield, faces higher volatility (30-day historical volatility of 0.1427) and a beta of 0.81 [6]. While its recent $1.25 billion debt offering aims to fund growth, its yield remains uncompetitive relative to WES [6].

WES's 9.8% yield thus stands out as a rare combination of high returns and manageable risk. Its BBB- rating, while one notch below EPD's A-, is justified by its strong EBITDA growth and disciplined leverage management [4]. Moreover, its business is expanding in key basins like the Delaware and DJ Basins, where long-term demand for midstream services is robust [2].

Historical backtesting of WES's performance around dividend record dates from 2022 to 2025 reveals a modest positive drift, with win rates exceeding 70% after the second week. While cumulative returns over 30 days averaged approximately 4%, the effect remains limited in magnitude and not statistically significant in most sub-windows. This suggests that while WES's yield is attractive, its price performance post-dividend events is relatively muted, aligning with its stable, fee-based business model.

Strategic Growth and Long-Term Resilience

Western Midstream's recent performance reinforces its appeal. In Q1 2025, the company reported record throughput in the Delaware Basin, driving strong financial results and a 4% quarter-over-quarter distribution increase [2]. Analysts, while cautious, maintain a “Hold” rating with a price target of $40.25, implying a 5.8% upside from current levels [7]. This suggests that the market recognizes WES's operational strengths but remains wary of broader sector headwinds—a sentiment that creates an attractive entry point for long-term investors.

Critically, WES's expanding footprint in high-growth basins positions it to capitalize on the energy transition. Its fee-based contracts and infrastructure investments ensure that cash flows remain resilient even as commodity prices fluctuate [4]. This contrasts with peers like CQPCQP-- and PAA, which face greater exposure to cyclical energy markets [1].

Conclusion: A Compelling Case for Income Investors

For income-focused investors, Western MidstreamWES-- represents a rare opportunity: a high-yield MLP with a strong balance sheet, low volatility, and a clear path to sustainable growth. While peers like EPDEPD-- and BIPBIP-- offer greater credit safety, their yields fall short of WES's 9.8%—a premium that is justified by the company's operational performance and strategic execution. As midstream infrastructure becomes increasingly critical to energy supply chains, WES's focus on fee-based contracts and disciplined leverage management ensures it remains a top-tier option for those seeking superior risk-adjusted returns.

Comentarios

Aún no hay comentarios