Walmart Marketplace Gains Traction: What Does it Mean for Margins?

Walmart Inc.’s WMT marketplace momentum is emerging as a meaningful structural lever within its e-commerce model. The platform is expanding steadily, with marketplace sales increasing about 20% in the fourth quarter of fiscal 2026, supported by rising seller participation and increased use of WalmartWMT-- Fulfillment Services, which reached 52%.

The key significance lies in how this growth is shaping margins indirectly. Third-party assortment allows Walmart to expand selection without carrying inventory, which helps reduce markdown exposure and improves working capital efficiency. This is particularly relevant as inventory growth has been well below the pace of sales, reflecting tighter control and a better balance between owned and third-party goods.

At the same time, marketplace scale is reinforcing other higher-margin streams within the ecosystem. As more sellers and products come onto the platform, this drives greater engagement across digital channels, supporting growth in advertising and membership income. These areas are already contributing meaningfully to profitability and are becoming more important as e-commerce penetration rises.

Apart from this, higher seller adoption of fulfillment services improves network utilization and helps spread fixed logistics costs more efficiently, supporting overall e-commerce economics.

Walmart remains focused on expanding its marketplace rather than maximizing profits from it at present. The current focus is on expanding assortment, onboarding sellers and driving category depth. Overall, third-party is already helping margins, but mainly as part of Walmart’s broader shift toward a more efficient and digitally driven business model.

What Do the Latest Metrics Say About Walmart?

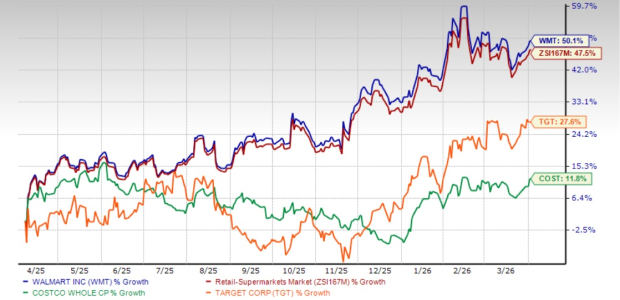

Walmart, which competes with Costco Wholesale Corporation COST and Target Corporation TGT, has seen its shares rally 50.1% in the past year compared with the industry’s 47.5% growth. Shares of Costco and Target have gained 11.8% and 27.6%, respectively, in the aforementioned period.

Image Source: Zacks Investment Research

From a valuation standpoint, Walmart's forward 12-month price-to-earnings ratio stands at 42.59, higher than the industry’s 38.86. The company is trading at a premium to Target (with a forward 12-month P/E ratio of 14.83), while trading at a discount to Costco (47.18).

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Walmart’s current fiscal-year sales and earnings per share implies year-over-year growth of 5% and 9.5%, respectively.

Walmart currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios