Vireo Growth's Financial Underperformance: Operational and Strategic Misalignment in a Competitive Cannabis Market

Financial Performance: Growth vs. Margins

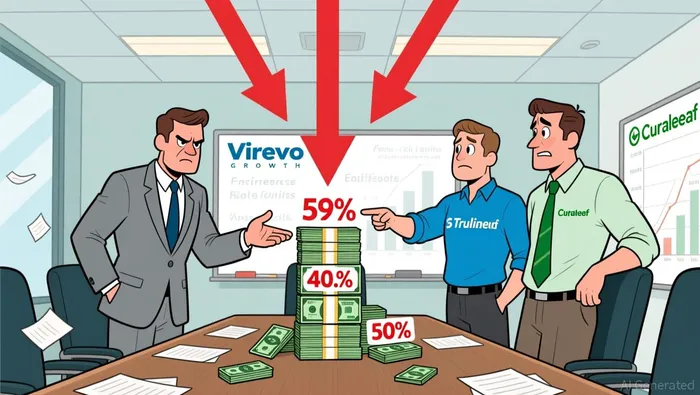

Vireo's Q3 2025 GAAP revenue of $91.7 million was bolstered by M&A activity, but its gross margins tell a different story. The company reported a GAAP gross margin of 40.8% and an adjusted gross margin of 55.4%, according to a StockTitan report. While the adjusted figure reflects non-GAAP adjustments, the GAAP margin lags behind industry peers. For instance, Trulieve Cannabis Corp. (TCNNF) reported a 59% gross margin in Q3 2025, according to a Yahoo Finance roundup, and Curaleaf Holdings (CURLF) improved its margin to 50%, according to the same Yahoo Finance roundup. These figures highlight Vireo's cost management challenges, particularly in production and integration of acquired assets.

Vireo's cost of goods sold (COGS) for Q3 2025 was $12 million, according to a MacroTrends report, but this does not account for the broader operational costs of integrating multiple acquisitions. Competitors like Grown Rogue International (GRUSF) have achieved production costs as low as $348 per unit in Oregon, according to a GuruFocus earnings call, a stark contrast to Vireo's opaque cost structure.

Operational Challenges: Integration and Expansion

Vireo's aggressive M&A strategy has created integration bottlenecks. The company entered a Restructuring Support Agreement with Schwazze, a multi-state operator, to optimize operations, and settled a $10 million dispute with Verano Holdings, according to a StockTitan report. While CEO John Mazarakis emphasized progress in integrating acquisitions by year-end, according to the StockTitan report, the lack of detailed metrics on integration efficiency raises concerns.

In contrast, competitors like Grown Rogue International have leveraged automation and ERP system upgrades to streamline operations, according to a GuruFocus earnings call. Vireo's implementation of a new ERP system is a step in the right direction, but the absence of concrete data on cost savings or productivity gains suggests delays in realizing synergies.

Strategic Misalignment: Market Expansion vs. Cost Discipline

Vireo's expansion into Minnesota's adult-use cannabis market is a strategic move, but it faces stiff competition. Grown Rogue International, for example, has already established a strong presence in the state and reported a 20% year-over-year yield improvement, according to a GuruFocus earnings call. Vireo's reliance on M&A-driven growth, while valid in a fragmented industry, risks overextending resources if integration costs outpace revenue gains.

Meanwhile, companies like Village Farms (VFFCF) have prioritized cost discipline and international expansion, achieving a 750% year-over-year increase in international cannabis sales, according to a Seeking Alpha article. Village Farms' stock surged 378.85% in 2025, according to the same Seeking Alpha article, underscoring the market's preference for disciplined operators. Vireo's stock, however, lacks comparable momentumMMT--, with no clear data on its performance relative to benchmarks, according to a StockTitan report.

Investment Implications

Vireo's Q3 2025 results highlight a critical juncture. While its cash reserves ($117.5 million) and debt refinancing ($10 million annualized interest savings, according to a StockTitan report) provide flexibility, the company must address operational inefficiencies and strategic drift. Investors should monitor:

1. Integration Progress: Has Vireo fully realized ERP and procurement synergies?

2. Margin Expansion: Can the company close the gap with peers on production costs?

3. Market Differentiation: Will Minnesota's adult-use market become a sustainable growth driver, or will it face price wars?

The cannabis sector's volatility, compounded by regulatory uncertainties, according to a Seeking Alpha article, demands a balance between aggressive expansion and operational rigor. Vireo's current trajectory suggests a reliance on M&A to mask underlying inefficiencies-a strategy that may not sustain investor confidence in the long term.

Conclusion

Vireo Growth's Q3 2025 results reflect the dual-edged nature of rapid expansion in the cannabis industry. While revenue growth is robust, the company's operational and strategic misalignment-evident in lagging margins, integration delays, and cost management-poses significant risks. As competitors like Grown Rogue and Village Farms demonstrate disciplined execution, Vireo must pivot toward sustainable efficiency to avoid being left behind in an increasingly competitive landscape.

Comentarios

Aún no hay comentarios