Vicor (VICR): Navigating Catalysts and Valuation in Niche Power Electronics Markets

Recent Stock Performance and Key Catalysts

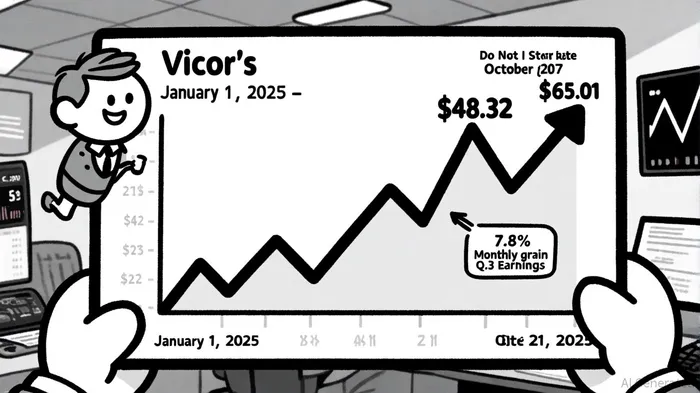

Vicor's stock has surged 4.7% year-to-date, outpacing broader market benchmarks, as noted in a Yahoo Finance article. As of September 8, 2025, shares traded at $50.5950, but recent momentum has propelled the price to $65.01, reflecting a 7.8% gain in the last month alone, according to MarketBeat. This outperformance is partly attributable to the company's strong Q2 2025 results, where revenue reached $141.05 million-well above the estimated $96.43 million-driven by robust demand for its Advanced Products segment, including next-generation Vertical Power Delivery (VPD) solutions (see the DataInsightsMarket profile).

The upcoming Q3 earnings report on October 21, 2025, is a critical catalyst, per the GuruFocus preview. Analysts project revenue of $95.4 million and adjusted EPS of $0.20, building on the prior quarter's 11.9% year-on-year growth noted in the Yahoo Finance piece. While these figures suggest continued momentum, the stock faces mixed analyst sentiment. A consensus "Hold" rating is tempered by bullish price targets, with Wall Street analysts averaging a $43.00 target-a 14.87% downside from the current price, according to MarketBeat. However, short-term indicators hint at a potential 15.58% rise over the next three months, highlighting the stock's volatility in the view of a StockInvest projection.

Valuation Metrics: Overvalued or Undervalued?

Vicor's valuation remains a point of contention. The company's price-to-earnings (P/E) ratio of 34.65 exceeds the market's fair value benchmark of 20x but lags behind the Computer and Technology sector average, as discussed in the Yahoo Finance article. Meanwhile, the price-to-sales (P/S) ratio has climbed from 4.83 in Q2 2025 to 6.87 as of October 20, 2025, reflecting a combination of rising stock prices and relatively stable revenue per share (see the WallStreetNumbers P/S history). Analysts argue that Vicor's current price of $53.65 slightly exceeds its estimated fair value of $52.50, suggesting a modest overvaluation per MarketBeat.

However, this assessment overlooks the transformative impact of Vicor's IP licensing strategy. In Q2 2025, the company secured a $45 million patent litigation settlement, and projections indicate licensing revenue could reach $300 million by 2026, according to a MarketChameleon analysis. This non-recurring income stream has already surpassed quarterly R&D expenditures, which account for 18% of revenue-a stark contrast to competitors' R&D ratios noted on the DataInsightsMarket profile. Such innovation-driven growth could justify a premium valuation, particularly as VicorVICR-- expands into high-growth sectors like AI data centers and electric vehicles (EVs).

Niche Market Position and Competitive Advantages

Vicor's dominance in niche power electronics is underpinned by its proprietary technologies, including Gen 5 VPD and 800V-to-48V bus converters (per the DataInsightsMarket profile). These solutions are critical for AI data centers, where energy efficiency is paramount, and EVs, where high-density power systems enable performance gains. The company's IP portfolio, enforced through aggressive litigation and ITC rulings, has created a moat against competitors. For instance, a 2025 Limited Exclusion Order (LEO) barred infringing products from entering the U.S., compelling OEMs and hyperscalers to license Vicor's technology, as reported in the MarketChameleon analysis.

This strategy has unlocked a $5 billion market opportunity for 800V-to-48V solutions by 2027, according to DataInsightsMarket. While Vicor competes with industry giants like General Electric and Raytheon, its focus on modular, high-density power modules positions it as a preferred supplier for specialized applications (see the IncFact profile). Strategic partnerships and technological advancements further reinforce its competitive edge, ensuring relevance in an industry where innovation cycles are accelerating.

Risks and Opportunities

Despite its strengths, Vicor faces headwinds. The reliance on IP licensing revenue introduces volatility, as settlements and settlements are inherently unpredictable. Additionally, the P/S ratio's upward trajectory raises concerns about overvaluation, particularly if growth in core product sales stagnates. However, the company's diversified revenue streams-combining product sales, licensing, and settlements-mitigate some of these risks.

For investors, the key lies in balancing these factors. Vicor's upcoming earnings report will provide critical insights into whether the company can sustain its momentum. If Q3 results meet or exceed expectations, the stock could see a re-rating, especially if the market begins to value its IP portfolio as a recurring revenue stream rather than a one-off windfall. Conversely, a miss could exacerbate the 14.87% downside highlighted by analysts, per MarketBeat.

Conclusion

Vicor's journey in 2025 exemplifies the dual-edged nature of niche market investing. While its stock price has surged on the back of strong fundamentals and IP-driven growth, valuation concerns and sector-specific risks demand a measured approach. For those willing to navigate the volatility, Vicor offers a unique opportunity to capitalize on the convergence of AI, EVs, and power electronics-a sector poised for long-term expansion. As the Q3 earnings report looms, all eyes will be on whether Vicor can translate its technological prowess into sustained shareholder value.

Comentarios

Aún no hay comentarios