VICI Properties' Investment Potential Following 2025 Market Correction: Strategic Entry Points and Long-Term Value Creation in the REIT Sector

In the wake of the 2025 market correction, real estate investment trusts (REITs) have faced heightened scrutiny, with investors seeking resilient assets capable of weathering macroeconomic volatility. Among these, VICI Properties (VICI) has emerged as a compelling case study, balancing disciplined capital management with strategic growth initiatives. This analysis evaluates VICI's post-correction performance, focusing on its financial health, occupancy stability, and analyst-driven optimism, while identifying strategic entry points for long-term value creation.

Financial Resilience and Debt Management

VICI Properties has demonstrated robust financial stewardship, particularly in managing its debt profile. As of the latest available data, the company maintains a debt-to-EBITDA ratio of 4.89, a metric that remains within conservative thresholds for REITs, according to StockAnalysis statistics. In Q2 2025, VICIVICI-- executed a $1.3 billion refinancing of its debt through investment-grade senior unsecured notes, extending maturities and reducing refinancing risks, as detailed in VICI's Q2 2025 release. This action, coupled with a Moody's credit rating upgrade to 'Baa3' in 2024, underscores the company's commitment to balance sheet strength (per StockAnalysis statistics).

Revenue growth has also been a key driver of stability. For Q1 2025, VICI reported $984.2 million in revenue, a 3.4% year-over-year increase, despite a $187 million rise in credit loss provisions, according to Benzinga. By Q2 2025, revenue climbed further to $1.0 billion, with a 4.6% year-over-year gain, prompting the company to raise its full-year 2025 adjusted funds from operations (AFFO) guidance to $2.35–$2.37 per share (see the company Q2 release). These figures highlight VICI's ability to generate consistent cash flows, even amid economic headwinds.

Occupancy Stability and Strategic Portfolio Enhancements

A critical factor in VICI's post-correction resilience is its 100% occupancy rate in Q1 2025, a testament to its tenant retention strategy and the inelastic demand for premium real estate assets, according to a MarketsGoneWild article. The company's portfolio, anchored by long-term leases with industry leaders like Caesars and DraftKings, provides a stable rental income stream. Strategic investments further reinforce this stability. For instance, VICI increased its commitment to the One Beverly Hills project by $150 million, bringing total investment to $450 million, and partnered with Red Rock Resorts on the North Fork Mono Casino & Resort, signaling confidence in high-growth markets, as outlined in the Q2 release.

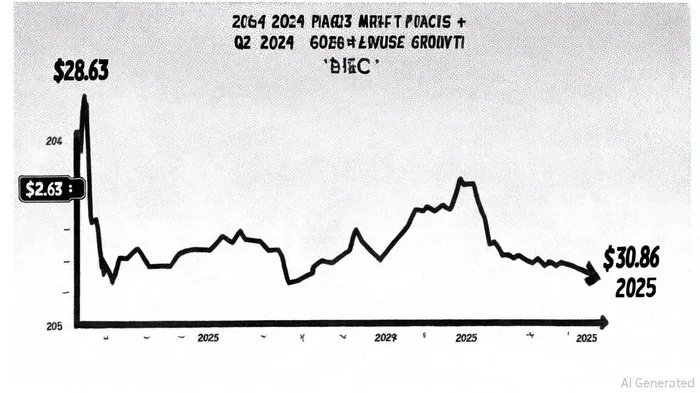

Analyst Sentiment and Stock Price Dynamics

VICI's stock has experienced volatility post-correction, with a low of $28.63 in April 2025 and a recent closing price of $30.86 on October 17, 2025, per Investing.com. While the stock has declined 2.94% over the past 12 months, analyst sentiment remains cautiously optimistic. A "Moderate Buy" consensus from 12 Wall Street analysts reflects this optimism, with 9 buy ratings and 3 holds (reported in the company Q2 release). The average 12-month price target of $35.40 implies a 6.01% upside from the current price, while recent upgrades-such as Scotiabank's $36.00 target and Citigroup's $36.00 target-suggest growing confidence in the company's trajectory, according to Benzinga.

Notably, 97.71% institutional ownership of VICI shares indicates strong backing from professional investors, who likely view the REIT as a defensive play in a fragmented market (per the company Q2 release). This institutional confidence, combined with VICI's 86.39% net margin-well above industry averages-further validates its long-term appeal (Investing.com also highlights the margins).

Strategic Entry Points and Long-Term Value Creation

For investors seeking entry points, VICI's current valuation presents an opportunity. The stock's pullback from its 52-week high of $34.29 to $30.86 offers a discount relative to analyst price targets, particularly given the company's 4.63% revenue growth and $601.3 million AFFO in Q4 2024 (per StockAnalysis statistics). The recent refinancing and credit rating upgrade also reduce downside risks, making the REIT a lower-volatility option in a high-interest-rate environment.

Long-term value creation hinges on VICI's ability to execute its $450 million One Beverly Hills expansion and replicate its success in the North Fork project. These initiatives, paired with a disciplined acquisition strategy, position the company to capitalize on premium real estate demand while maintaining occupancy rates above 95% (as noted in the Q2 release).

Conclusion

VICI Properties' post-2025 market correction performance underscores its role as a resilient REIT with strong fundamentals and strategic agility. While short-term volatility persists, the company's debt management, occupancy stability, and analyst-driven optimism create a compelling case for long-term investors. For those prioritizing strategic entry points, the current valuation-coupled with a "Moderate Buy" consensus and rising price targets-suggests that VICI is well-positioned to deliver value as the market stabilizes.

Comentarios

Aún no hay comentarios