VICI Properties: A Compelling Case for Income Investors in a High-Rate Environment

For income-focused investors navigating the challenges of a high-interest-rate environment, VICI Properties (VICI) emerges as a compelling opportunity. With a robust balance sheet, disciplined capital allocation, and a dividend yield of 5.41%[3], the real estate investment trust (REIT) offers a rare combination of undervaluation and income stability. This analysis explores why VICIVICI-- is well-positioned to deliver long-term value, even as broader market conditions remain uncertain.

Financial Performance: Strong Cash Flow and Dividend Resilience

VICI's Q2 2025 results underscore its operational strength. The company reported $1.001 billion in revenue and $0.60 in AFFO per share, reflecting a 4.9% year-over-year increase[1]. Its dividend of $0.4325 per share is supported by a conservative payout ratio of 72% of AFFO and 74.6% of operating free cash flow (OFCF)[1], leaving ample room for future growth. These metrics highlight a critical advantage: even in a high-rate environment, VICI's triple-net lease model—where tenants cover property expenses—ensures predictable cash flows[1].

The company's liquidity further reinforces its stability. With $2.2 billion undrawn on its revolving credit facility, $621 million in forward sale proceeds, and $233 million in cash, VICI has the flexibility to fund dividends and strategic investments without overleveraging[1]. Notably, 98.1% of its $16.7 billion net debt is fixed-rate, shielding it from rising interest costs[1]. This structural advantage is rare among REITs and positions VICI to outperform peers in a prolonged high-rate climate.

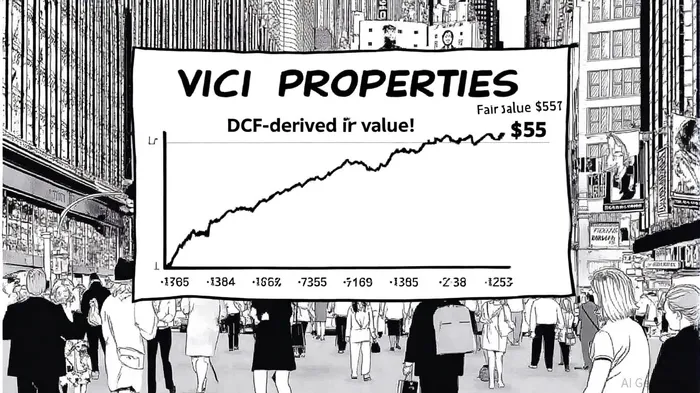

Valuation: A Significant Discount to Intrinsic Value

Despite its strong fundamentals, VICI's stock price has declined to $31.84 as of September 19, 2025, trading at a steep discount to its DCF-derived fair value of $55[1]. This disconnect presents an attractive entry point for long-term investors. A discounted cash flow model, using VICI's updated AFFO guidance of $2.35–$2.37 per share (4.4% growth) and a 10% discount rate, suggests an expected annualized return of approximately 23%[1].

The undervaluation is further supported by historical trends. Over the past month, the stock has traded within a $31.19–$33.54 range, with analysts assigning a 90% probability of remaining within this band over the next three months[3]. However, given the company's upgraded guidance and strategic initiatives—such as a $450 million investment in the One Beverly Hills project and a $510 million financing agreement for the North Fork Mono Casino—the intrinsic value is likely to converge with market price over time[2].

Dividend Sustainability: A Buffer Against Volatility

Income investors prioritize dividend sustainability, and VICI's metrics are reassuring. Its 52.7% payout ratio relative to quarterly earnings and 74.6% payout ratio relative to OFCF[1] provide a buffer against economic downturns. Additionally, the company has no principal repayments due in 2025 and remains in compliance with all debt covenants[1]. These factors, combined with a five-year dividend growth streak, suggest the current yield of 5.41%[3] is unlikely to be cut, even if rates remain elevated.

While one source notes a “low” dividend sustainability score, this appears to reflect macroeconomic uncertainties rather than operational weaknesses. VICI's focus on long-term, triple-net leases and experiential assets (e.g., luxury hotels and casinos) ensures recurring revenue streams that are less sensitive to interest rate fluctuations[3].

Strategic Positioning: Growth Through Discipline

VICI's management has emphasized internally funded growth and disciplined capital deployment[3]. Recent investments, such as the expanded commitment to One Beverly Hills and the North Fork Mono Casino, align with its strategy of acquiring high-margin, experiential assets. These projects not only enhance AFFO but also diversify revenue beyond traditional gaming properties.

The company's debt-to-equity ratio of 0.67x and net debt-to-EBITDA of 4.98x[2] further demonstrate prudent leverage management. By maintaining conservative debt levels and prioritizing fixed-rate financing, VICI minimizes refinancing risks while retaining capacity for strategic acquisitions.

Conclusion: A High-Yield Opportunity with Upside

For income-focused investors, VICI PropertiesVICI-- represents a rare combination of attractive yield, strong cash flow, and undervaluation. Its current stock price of $31.84 offers a compelling entry point, with a DCF model suggesting nearly 70% upside to reach $55[1]. In a high-interest-rate environment, where many REITs struggle with refinancing costs and declining valuations, VICI's fixed-rate debt structure and triple-net lease model provide a competitive edge.

As the company executes on its strategic initiatives and navigates macroeconomic headwinds, the 5.41% dividend yield[3] and disciplined capital allocation make VICI a standout choice for those seeking both income and long-term capital appreciation.

Comentarios

Aún no hay comentarios