Vertiv's Upcoming Earnings Report and Growth Catalysts: Assessing Margin Resilience and Long-Term Contract Momentum in a High-Service-Automation Sector

The data center and AI infrastructure sector is on fire-and Vertiv (VRTX) is riding the wave with both hands on the wheel. As the company prepares to report Q3 2025 earnings, investors are fixated on two critical questions: Can Vertiv sustain its margin resilience amid lingering supply chain headwinds? And does its $8.5 billion contract backlog signal a durable tailwind for long-term growth? Let's break it down.

Margin Pressures: Temporary Woes or Structural Concerns?

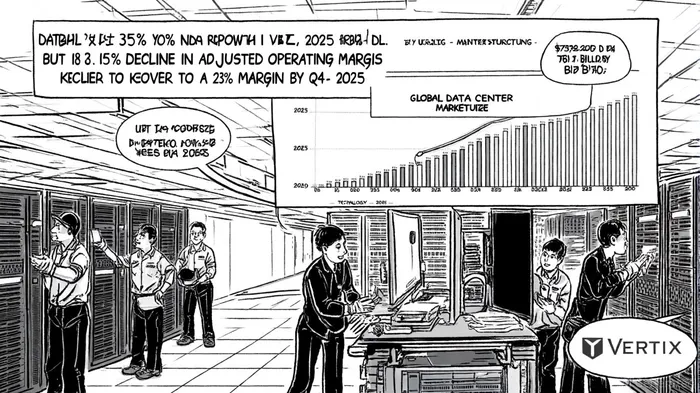

Vertiv's Q2 2025 results revealed a 35% year-over-year surge in net sales to $2.6 billion, driven by insatiable demand for AI-enabled infrastructure, according to Vertiv's press release. Yet, its adjusted operating margin contracted to 18.5%, down 110 basis points from the prior year, due to tariffs, supply chain reconfiguration costs, and operational inefficiencies from rapid scaling, as detailed in the earnings call transcript. While these numbers might raise eyebrows, management has been clear: these are temporary pain points.

According to a fintool analysis, Vertiv expects to resolve these margin drags by year-end, with Q4 2025 operating margins projected to rebound to 23%-a 200-basis-point improvement from Q2. This trajectory aligns with the company's long-term target of 25% by 2029, as noted in an EarningsIQ article. The key here is execution. If Vertiv can normalize its supply chain and absorb the remaining transition costs, its margins should stabilize-and the math suggests there's room to exceed expectations.

Backlog and Guidance: A Recipe for Revenue Visibility

The real story here is the $8.5 billion backlog, a 21% year-over-year increase that reflects a 1.2x book-to-bill ratio, according to a SignalBloom report. This isn't just a number-it's a moat in a sector where demand is outpacing supply. With AI workloads driving hyperscale projects and cloud providers scrambling for capacity, Vertiv's backlog provides a clear line of sight to future cash flows.

Management has already raised full-year 2025 guidance, projecting net sales of $10 billion and adjusted EPS of $3.80, per an EarningsIQ note. For Q3, the company anticipates organic revenue growth of 22%, with mid-30s growth in the Americas and low 20s in APAC, according to the GMI Insights blog. These numbers aren't just optimistic-they're defensible, given the current tailwinds in the data center sector.

Industry Tailwinds: AI Is the New Gravity

The high-service-automation sector is accelerating at a breakneck pace. Global data center market size hit $527.46 billion in 2025 and is projected to grow at a 6.98% CAGR to $739.05 billion by 2030, according to a CBRE report. More importantly, AI-specific data center capacity is expected to expand at a blistering 33% CAGR from 2023 to 2030, per a Converge Digest piece. Vertiv's expertise in power, cooling, and modular solutions positions it as a critical enabler of this transformation.

Consider the Stargate initiative, where OpenAI and Oracle are adding 4.5 gigawatts of US data center capacity-pushing total capacity beyond 5 GW, as noted in the conference transcript. Vertiv's cold-plate and immersion cooling technologies are already being deployed to manage AI racks with power densities of 500–1000kW, per Vertiv's data center trends. Meanwhile, its acquisition of Great Lakes Data Racks & Cabinets and partnerships with NVIDIA underscore its commitment to dominating the white-space segment, as EarningsIQ has documented.

Strategic Moves: Innovation and Resilience

Vertiv isn't just riding the AI wave-it's shaping it. The company's investments in R&D, modular solutions, and regional manufacturing expansion are designed to future-proof its operations. For instance, its hybrid cooling configurations and high-density UPS systems are tailored for AI's unique demands, according to a Gilder Report article. Additionally, its focus on microgrids and small modular reactors addresses the energy consumption challenges of AI workloads, as noted in the earlier EarningsIQ note.

These moves are paying off. In Q1 2025, Vertiv's backlog surged by $1.6 billion, and its net income hit $164 million, according to an earnings-event study. With a 24% YoY sales growth in that quarter, the company is proving that it can scale without sacrificing innovation.

The Bottom Line: Buy, Hold, or Watch?

Vertiv's Q3 earnings report will be a litmus test for its margin resilience and operational execution. While near-term pressures persist, the long-term fundamentals are compelling. The $8.5 billion backlog, coupled with a $10 billion full-year sales target, suggests a company that's not just surviving but thriving in a high-service-automation sector.

For investors, the key is to stay the course. If Vertiv can deliver on its Q4 margin guidance and maintain its leadership in AI infrastructure, this stock could outperform the broader market. But if supply chain issues linger or demand for AI cooling solutions softens, caution is warranted. Either way, Vertiv is a name to watch-and its upcoming earnings report will offer critical clues.

Historical data on VRT's earnings events from 2022 to 2025 reveals a mixed picture for investors relying on a simple buy-and-hold strategy. Over 14 earnings releases, the average 30-day post-earnings excess return was modest at +5.6%, but statistically insignificant (see the earnings-event study referenced above). The win rate fluctuated between 50–65%, offering no clear directional edge, while most of the cumulative move occurred after the second week post-announcement. These findings suggest that while VRT's long-term growth drivers remain intact, short-term volatility around earnings reports has historically been limited and unpredictable. Investors should focus on the company's ability to execute its margin recovery and backlog monetization rather than overreacting to near-term price noise.

```

Comentarios

Aún no hay comentarios