Verizon's Recent Share Price Decline: Strategic Entry or Cautionary Signal for Long-Term Investors?

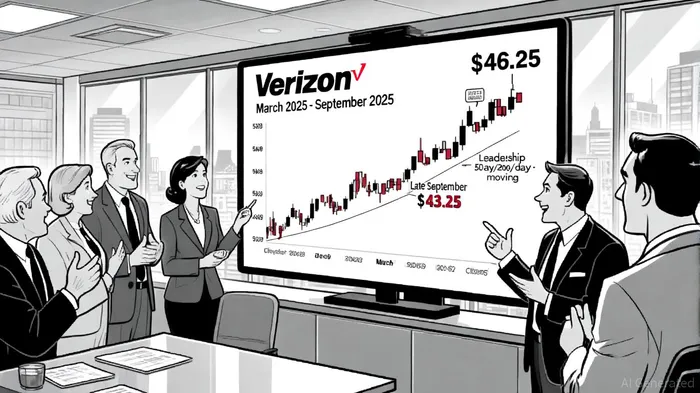

Verizon Communications (VZ) has experienced a notable pullback in its share price over the past month, closing at $43.25 on September 28, 2025, a 0.74% decline from the previous day's close of $43.48, according to historical data. This decline, while modest in the context of the stock's broader volatility, has sparked debate among investors about whether the move reflects a strategic entry point or a cautionary signal. To assess this, we must dissect the interplay of recent leadership changes, financial fundamentals, and competitive dynamics shaping the stock's trajectory.

Leadership Uncertainty and Market Reaction

The most immediate catalyst for the recent selloff was a surprise leadership change in late September, when Dan Schulman, former CEO of PayPal, was appointed to replace Hans Vestberg. The market reacted swiftly, with shares dropping 4.8% on the day of the announcement, as reported in a Yahoo Finance article. While Schulman's appointment brings fresh expertise in digital transformation, investors remain cautious about the implications for Verizon's 5G and fiber expansion strategies. The stock closed at $41.44 on the day of the leadership shift, reflecting a 5.1% single-day decline, according to Benzinga. However, VerizonVZ-- has since reaffirmed its full-year financial guidance, signaling confidence in its operational trajectory despite the transition.

Financial Fundamentals: Mixed Signals

Verizon's Q3 2025 earnings report revealed a mixed bag of results. Revenue of $33.33 billion fell slightly below expectations, driven by a 4.3% decline in wireless equipment sales as customers delay device upgrades, according to Stock-Analysis data. Yet, wireless service revenue grew, and the company added 239,000 postpaid phone subscribers and 389,000 broadband customers, underscoring the strength of its 5G and fixed wireless offerings. Adjusted EBITDA of $12.5 billion and a 43.4% EBITDA margin in the consumer segment highlight operational resilience.

However, net income plummeted to $3.4 billion from $4.9 billion in the prior year, largely due to a $1.7 billion severance charge tied to workforce reductions. This non-recurring expense, while painful, underscores Verizon's commitment to cost discipline-a critical factor in an industry where capital expenditures for 5G infrastructure remain high.

Debt Management and Competitive Positioning

Verizon's deleveraging efforts have been a bright spot. The company's debt-to-equity ratio stood at 1.67 as of Q3 2025, down from 2.67 in mid-2024, according to StockAnalysis. This trend aligns with a broader strategy to reduce financial risk, as evidenced by a declining debt-to-assets ratio (0.38 in Q2 2025 vs. 0.46 in Q1 2021). These metrics suggest a more stable balance sheet, though the pending $20 billion acquisition of Frontier Communications-a deal aimed at expanding fiber broadband reach-could test this progress.

Competitively, Verizon faces intensifying pressure from AT&T and T-Mobile. T-Mobile's partnership with SpaceX to expand satellite-based services, for instance, poses a long-term threat to Verizon's terrestrial network dominance. Yet, Verizon's aggressive 5G and fiber investments, coupled with its robust EBITDA margins, position it to maintain a strong market position.

Valuation: Undervalued or Overcorrected?

Verizon's current valuation appears compelling. Trading at a PE ratio of 10.1x-well below the industry average of 17.0x and the peer group average of 24.4x-data from Macrotrends suggest the stock may be undervalued relative to earnings. Additionally, the price is trading below both its 50-day ($43.65) and 200-day ($43.35) moving averages, indicating potential oversold conditions. However, the 10.7% drop from its 52-week high of $46.49 in March 2025, noted earlier by Benzinga, raises questions about whether the market is overcorrecting for short-term challenges.

Strategic Considerations for Long-Term Investors

For long-term investors, the key question is whether Verizon's recent decline reflects a temporary correction or a deeper structural issue. The leadership transition, while disruptive, does not inherently signal a fundamental shift in the company's business model. Schulman's background in digital payments could accelerate Verizon's pivot toward monetizing 5G through enterprise and AI-driven services-a growth vector highlighted in a TS2 Tech article.

However, risks remain. The pending Frontier acquisition, while strategic, could strain cash flow and delay shareholder returns. Additionally, the telecom sector's low-growth profile and regulatory uncertainties (e.g., spectrum auctions, net neutrality debates) warrant caution.

Conclusion: A Calculated Opportunity

Verizon's recent share price decline offers a nuanced case for investors. The stock's attractive valuation, coupled with strong EBITDA margins and deleveraging progress, suggests a potential entry point for those comfortable with the company's long-term vision. Yet, the leadership transition and competitive pressures necessitate a measured approach. Investors should monitor key metrics-such as post-Frontier integration progress, 5G subscriber growth, and Schulman's strategic priorities-before committing. In a market where patience is rewarded, Verizon's pullback may prove to be a buying opportunity for those with a multi-year horizon.

Comentarios

Aún no hay comentarios