Verizon's 18% ROE: A Signal of Superior Capital Efficiency or a Fleeting Glimmer in a Competitive Sector?

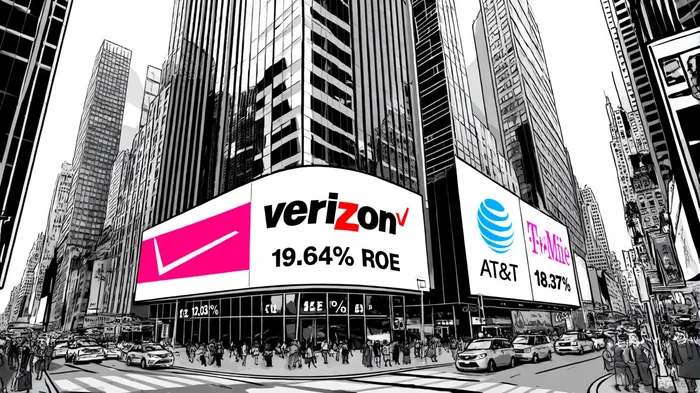

In the fiercely competitive telecom sector, Return on Equity (ROE) has emerged as a critical metric for evaluating capital efficiency and long-term shareholder value creation. Verizon Communications Inc.VZ-- (NYSE:VZ) has recently reported an ROE of 19.64% for Q3 2025, a figure that not only outpaces its peers but also exceeds the industry median of 18.36% and average of 15.35% per GuruFocus. This raises a pivotal question: Does this performance signal a structural advantage in Verizon's capital allocation and operational strategy, or is it a temporary outperformance in a sector grappling with commoditization and margin pressures?

Verizon's ROE Trajectory: A Tale of Resilience

Verizon's ROE has surged from 11% in September 2024 to 19.64% by June 2025, reflecting a dramatic turnaround. This growth contrasts with the telecom industry's marginal decline in Q2 2025, where ROE dipped to 15.35% from 15.44% in Q1 due to deteriorating net income, according to CSIMarket. Verizon's ability to buck this trend underscores its disciplined cost management and strategic focus on high-margin segments. For instance, the company added 339,000 broadband subscribers in Q1 2025 while reaffirming its wireless revenue growth guidance, signaling a pivot toward diversified revenue streams in an article from RCR Wireless.

However, this strength comes with caveats. Verizon's debt-to-equity ratio of 1.71 remains elevated, raising concerns about financial leverage and its impact on long-term flexibility, as highlighted by Stockwire. While high debt can amplify returns in growth phases, it also heightens vulnerability during economic downturns or interest rate hikes-a risk factor that investors must weigh against current ROE figures.

Peer Comparison: T-Mobile's Challenge and AT&T's Stagnation

Verizon's 19.64% ROE in Q3 2025 places it ahead of AT&T's 12.03% and T-Mobile's projected 18.37%, per FinanceCharts. This gap highlights divergent strategic priorities:

- T-Mobile has prioritized aggressive 5G deployment and subscriber acquisition, achieving a 158.5 Mbps average download speed (versus Verizon's 46 Mbps) and 1.3 million postpaid additions in Q1 2025, according to a PhoneArena report. Its ROE trajectory, while strong, reflects a growth-at-all-costs model that may strain margins as competition intensifies.

- AT&T, with a ROE of 12.03%, has focused on fiber expansion and convergence strategies, adding 261,000 fiber subscribers in Q1 2025. However, its balanced approach has yielded modest returns, lagging behind both VerizonVZ-- and T-Mobile, as noted in a FinancialContent article.

Verizon's superior ROE stems from its dual emphasis on customer retention (via loyalty programs like the 3-Year Price Lock) and broadband expansion. Despite losing 289,000 postpaid wireless subscribers in Q1 2025, the company mitigated churn through targeted incentives and capitalized on its fixed wireless access (FWA) offerings, as reported by TalkMarkets. This strategic duality-retaining high-margin customers while diversifying into fiber-has proven more effective than T-Mobile's pure growth or AT&T's cautious approach.

Strategic Drivers: 5G, AI, and Operational Efficiency

The telecom sector's broader push toward AI and operational efficiency is reshaping ROE dynamics. Verizon's 19.64% ROE aligns with its investments in AI-powered network optimization and predictive maintenance, which reduce capital expenditures (CapEx) and improve service reliability, according to Deloitte Insights. By contrast, T-Mobile's reliance on aggressive CapEx for 5G expansion risks diluting returns if demand for premium 5G services plateaus.

Debt management further differentiates Verizon. While all three carriers face a $28 billion free cash flow gap by 2028, per a Bain analysis, Verizon's focus on monetizing legacy assets and streamlining operations has improved its EBITDA margins. AT&T's slower pivot to fiber and T-Mobile's debt-funded expansion, meanwhile, expose them to greater volatility.

Long-Term Value Creation: A Mixed Picture

Verizon's ROE suggests strong capital efficiency, but its long-term value creation hinges on sustaining this performance. The company's high debt load and reliance on loyalty programs to offset churn could erode margins if economic conditions worsen. Conversely, its broadband and FWA growth, coupled with AI-driven cost savings, position it to outperform peers in a sector where total shareholder return (TSR) has historically lagged the S&P 1200 by ~8 percentage points annually, according to a BCG report.

For investors, the key question is whether Verizon's 19.64% ROE reflects a sustainable competitive edge or a temporary boost from cyclical factors. Given the telecom industry's ongoing commoditization and regulatory headwinds, the former scenario is plausible only if Verizon continues to innovate in AI, network efficiency, and customer-centric strategies.

Conclusion

Verizon's ROE of 19.64% is a compelling indicator of superior capital efficiency relative to peers and industry benchmarks. However, this metric must be contextualized within the company's high debt profile and the sector's structural challenges. While T-Mobile's growth-driven model and AT&T's cautious approach offer alternative value propositions, Verizon's balanced focus on retention, diversification, and operational rigor currently positions it as the telecom sector's most effective capital allocator. Investors should monitor its ability to sustain this momentum amid evolving market dynamics.

Comentarios

Aún no hay comentarios